The US dollar traded higher yesterday, even though stocks marched north as well. That said, with expectations for more easing by the ECB and the Fed, our own view is that equities are likely to continue gaining, but the US dollar is likely to resume its latest downtrend. Barring any surprising market headlines, the focus will probably now turn to the official US employment data, due to be released tomorrow.

USD GAINS IN TANDEM WITH STOCKS; IS THIS PATTERN TEMPORARY?

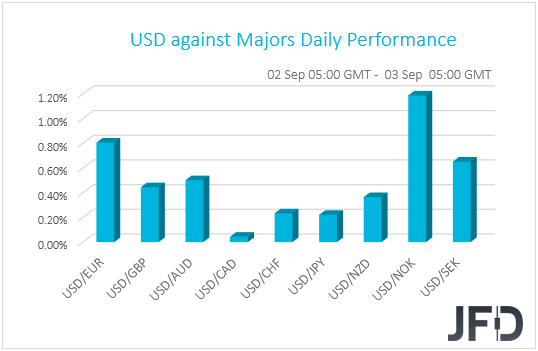

The US dollar traded higher against all but one of the other G10 currencies on Wednesday and during the Asian morning Thursday. It gained the most versus NOK, EUR, and SEK in that order, while it was found virtually unchanged against CAD.

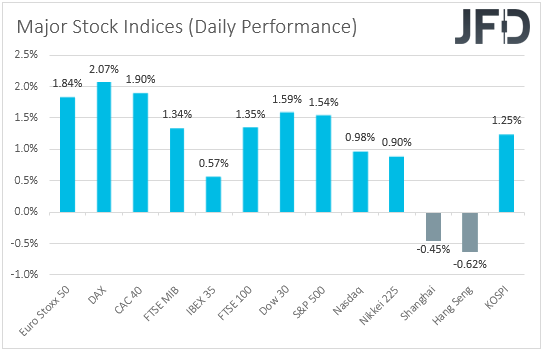

The strengthening of the greenback, and the relatively little gains in the yen and the Swiss franc suggest that the financial community traded in a risk-off fashion yesterday. However, looking at the performance in the equity world, we see that this was not the case. Major EU and US indices were a sea of green, although sentiment softened somewhat during the Asian session today. Japan’s Nikkei 225 and South Korea’s KOSPI were up 0.90% and 1.25%, but China’s Shanghai Composite and Hong Kong’s Hang Seng slid 0.45% and 0.62% respectively.

EU shares rebounded yesterday, with the chemicals sector ending at a record high and tech stocks tracking gains in their US peers, ending at their strongest level since 2001. That said, the strength in Wall Street on Wednesday was mainly owed to defensive utilities, consumer staples, real estate and financials. What may have also helped the rally in the US indices may have been the release of the Beige Book, which showed a modest increase in activity for U.S. businesses and an increase in employment through late August.

Remember that in the last couple of days, we’ve been noting that we would treat the latest setback in equities as a corrective phase before another rebound, and yesterday’s action proves us right. With inflation in the Eurozone entering negative waters, and the ADP employment report in the US showing less than expected job gains, expectations over further stimulus by the ECB and the Fed may have increased. On Tuesday, ECB Chief Economist Philip Lane said that the EUR/USD exchange rate “does matter” for monetary policy, comments that resulted in the rejection in the pair from near the psychological zone of 1.20, while last week, Fed Chief Powell said that he and his colleagues are willing to tolerate above 2% inflation for a while before raising interest rates, which means extra loose policy for longer. On top of that, in the minutes from the latest FOMC gathering it was revealed that additional accommodation could be required.

The question now may be: why the dollar is strengthening during risk-on periods? Has it lost its safe-haven status? Whatever the answer may be, we believe that its recovery may be temporary. We believe that the Fed’s willingness to expand its simulative efforts may eventually bring the currency back under selling interest, while at the same time, it may keep equity markets supported.

Now, barring any surprising headlines that could shake the broader market appetite, we believe that the next big event may be tomorrow’s official US employment data for August. The miss in the ADP report suggests that the NFPs may also miss their own forecast, which is at 1.400mn. This would mean that the labor market is recovering slower than previously anticipated, and may add even more to expectations over additional Fed action. The riddle here is whether the equity markets will retreat or gain after such an outcome. On the one hand, they could retreat on signs of a slower economic recovery, while on the other hand, they could gain on increased speculation for more easing. Our humble view is that the second is more likely. For the dollar is more straight forward and we believe that it may resume its slide. Other safe havens, like the Swiss franc and the yen, may also depreciate, while risk-linked currencies, the likes of the Aussie and the Kiwi, may get benefited.

EURO STOXX 50 – TECHNICAL OUTLOOK

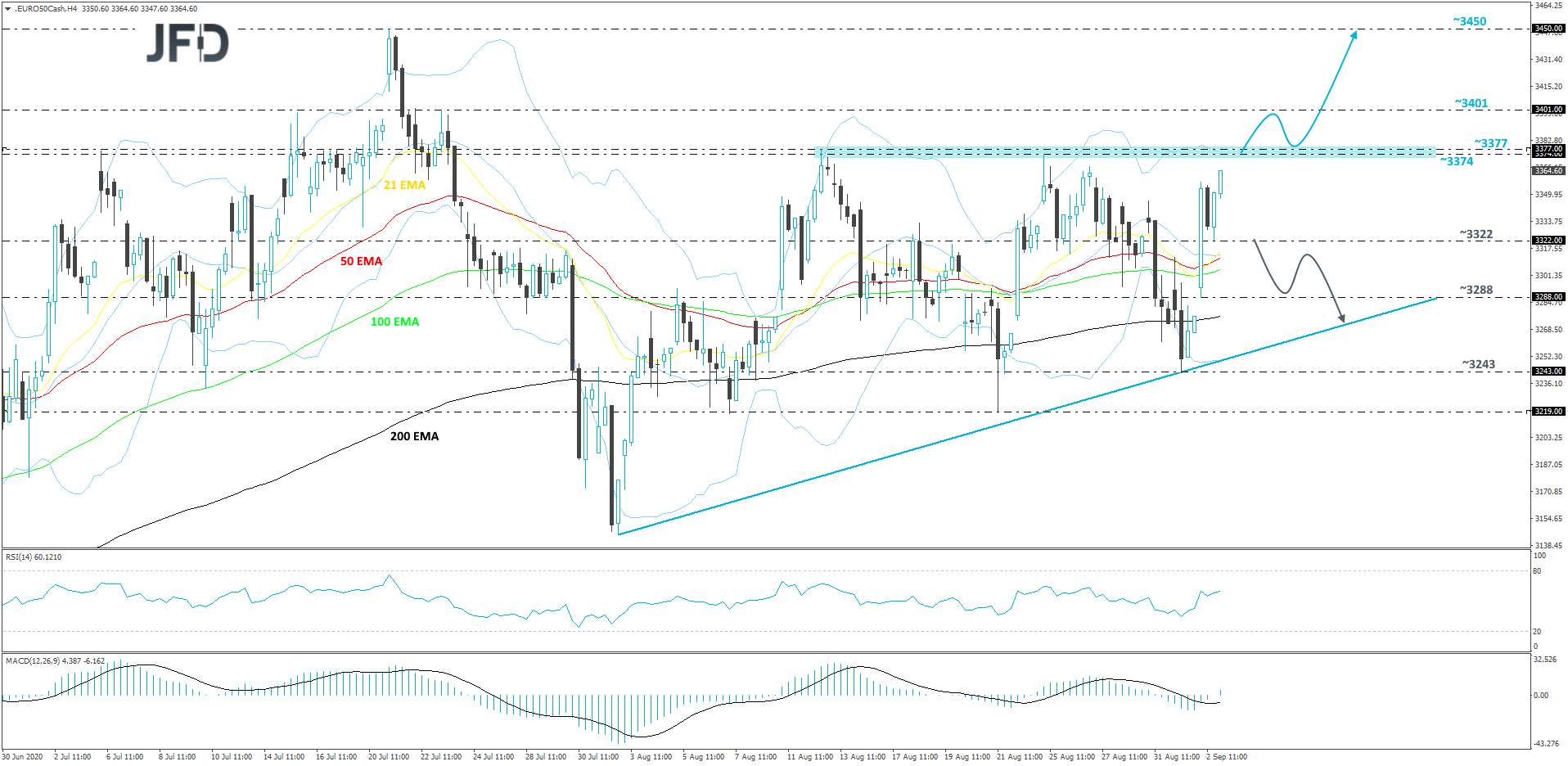

The Euro Stoxx 50 index had a strong move higher yesterday, pushing back closer to its key resistance area between the 3374 and 3377 levels, marked near the highs of August 25th and 12th respectively. In addition to that, the price continues to balance above a short-term upside support line taken from the low of July 31st. Looking at our oscillators, the RSI and the MACD, both indicators are still pointing higher and indicating a rising upside price momentum. However, for us to get a bit more excited about higher areas, we would wait for a push above the 3377 barrier first.

A strong move above the aforementioned 3377 hurdle, would confirm a forthcoming higher high, potentially clearing the path to the 3401 zone, which is marked by the high of July 23rd. The price may stall there for a bit, however, if the buyers are still feeling confident, they might push Euro Stoxx 50 above that resistance zone and aim further north. That’s when we will consider a possible move towards the 3450 level, marked by the highest point of July.

Alternatively, if the index slides back below the 3322 hurdle, marked by yesterday’s intraday swing low, that could invite a few more sellers into the game. Euro Stoxx 50 may then visit yesterday’s low, at 3288, a break of which could open the way towards the aforementioned upside line. If that line stays intact, this whole move lower could be considered as a temporary correction and the bulls may try to take advantage of the lower price again, in order to lift the index higher.

NZD/CHF – TECHNICAL OUTLOOK

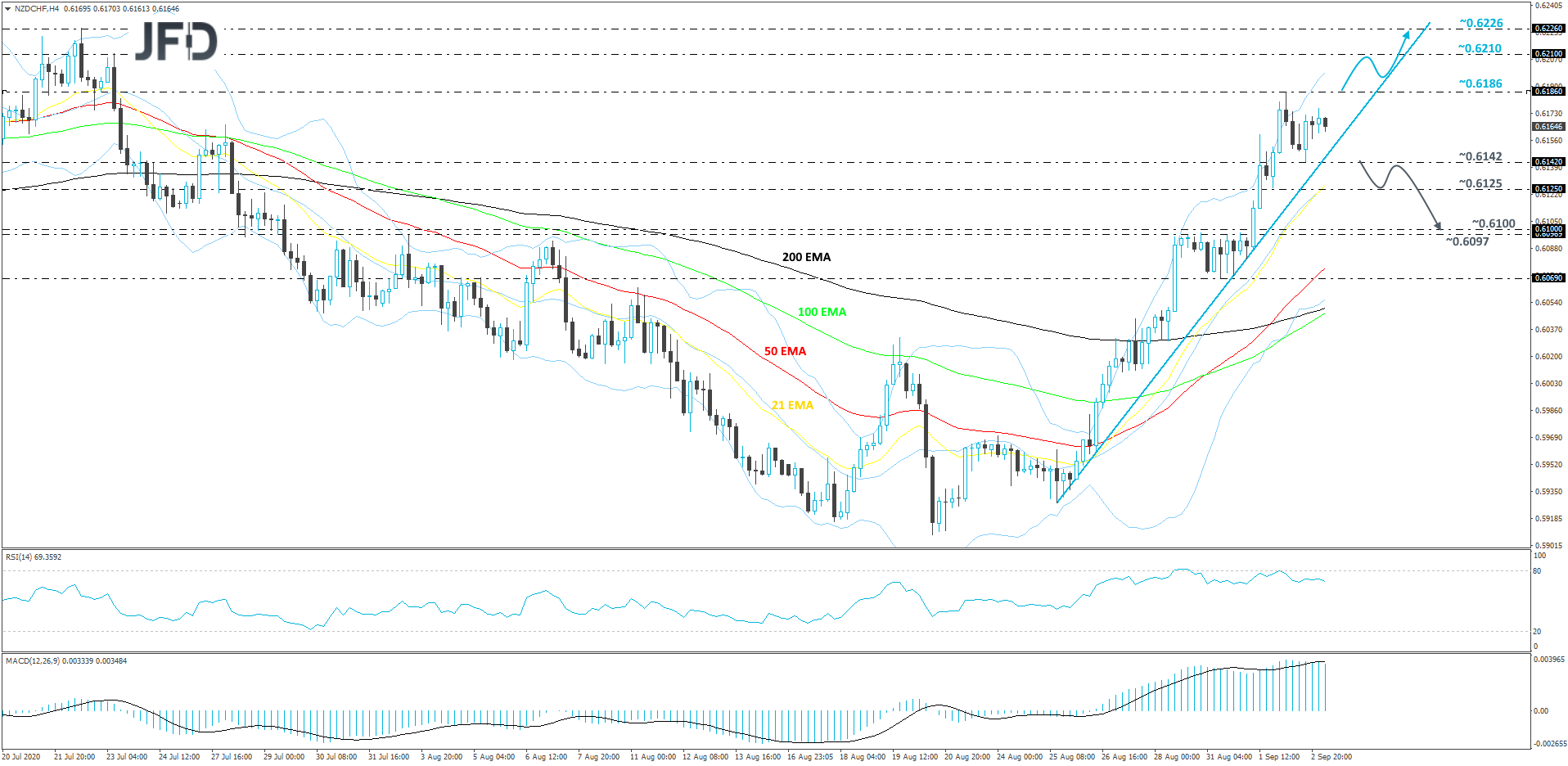

NZD/CHF continues to trade above a steep short-term upside support line drawn from the low of August 25th. Yesterday, the pair got held near the 0.6186 barrier, from where it corrected a bit lower. However, if the rate remains above that upside line, there is a good chance we could see it moving higher again. But in order to get a bit more comfortable with further upside, a break of the 0.6186 barrier would be needed, hence our somewhat bullish approach for now.

If the bulls are able to lift NZD/CHF above that 0.6186 barrier, such a move would confirm a forthcoming higher high and potentially send the rate towards the 0.6210 hurdle, which is the high of July 23rd. The pair might be forced to stall there temporarily. It may even correct slightly lower. That said, if the aforementioned upside line continues to provide support, the bulls might take charge and push the rate up again. If this time the pair is able to overcome the 0.6210 hurdle, the next potential resistance level could be at 0.6226, marked by the high of July 22nd.

On the other hand, if the rate suddenly violates the previously talked about upside line and then slides below yesterday’s low, at 0.6142, that may lead to a change in the short-term trend. If so, NZD/CHF could drift to the 0.6125 obstacle, a break of which might clear the way to the next support area around the 0.6100 or the 0.6097 levels, marked near the highs of August 28th and 31st.

AS FOR TODAY’S EVENTS

During the EU session, we have Switzerland’s CPIs, as well as Eurozone’s and the UK’s final services and composite PMIs, all for August. Switzerland’s CPI is expected to have ticked up to -0.8% yoy from -0.9%, while, as it is always the case, the final PMIs are expected to confirm their preliminary estimates.

We get the final Markit services and composite PMIs for August from the US as well. They are also expected to confirm their initial prints. The ISM non-manufacturing PMI for the month and the nation’s trade balance for July are also due to be released. We get trade data for July from Canada as well.

We also have three speakers on today’s schedule: BoE Governor Andrew Bailey, ECB Executive Board member Isabel Schnabel, and Chicago Fed President Charles Evans.