Most major EU and US indices traded higher yesterday, with the S&P 500 and the NASDAQ hitting fresh record highs. In our view, this means that following last week’s US CPIs, investors have been more comfortable in increasing their risk exposure, even with the Fed decision drawing closer.

The decision will be made public tomorrow, and it would be interesting to see whether there will be any discussion over a potential QE tapering.

S&P 500 And NASDAQ Hit Fresh Records Ahead Of The Fed

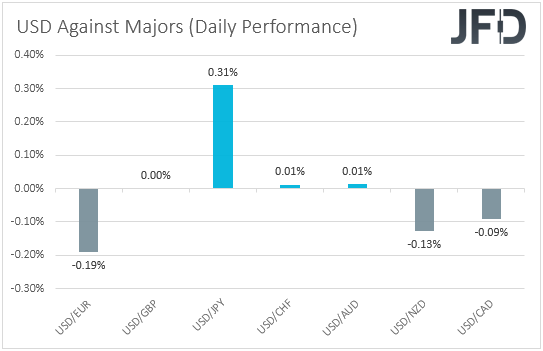

At time of writing, the US dollar was found lower or unchanged against most of the other major currencies this morning. It was higher only versus JPY. The greenback lost some ground against EUR, NZD, and CAD, while it traded unchanged versus GBP, CHF and AUD.

The relative strength of the commodity-linked kiwi and loonie, combined with the weakness in the safe-haven yen, suggests that markets traded in a risk-on fashion yesterday and today in Asia.

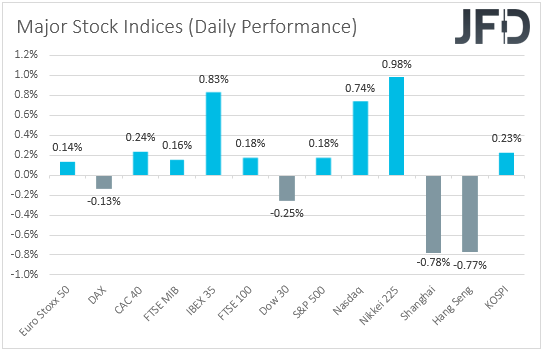

Looking at the performance in the equity world, we see that, yes indeed, most major EU and US indices closed in positive waters, with the S&P 500 and the NASDAQ making record highs.

The only exceptions were Germany’s DAX and Wall Street’s Dow Jones, which slid somewhat. That said, appetite was more on the mixed side today in Asia. Although Japan’s Nikkei 225 and South Korea’s KOSPI traded higher, China’s Shanghai Composite and Hong Kong’s Hang Seng edged south.

In our view, this means that following last week’s inflation data from the US, investors have been more comfortable in increasing their risk exposure, even with the Fed decision drawing closer. Remember that, despite the sharp acceleration in the CPIs, the details of the report revealed that there were hefty contributions to that from short-term increases in airline ticket prices and used cars, which supports the fact that the latest inflation spike may indeed be due to transitory factors.

Having said that though, ahead of the data, several policymakers have expressed their desire to discuss QE tapering at one of their upcoming gatherings. Thus, although we don’t expect officials to rush into taking a decision now, it would be interesting to see whether there will be a discussion around the matter, and if so, whether we will get any hints over a potential desired pace of withdrawal.

A fast pace may suggest that Fed officials do not see the surge in inflation as transitory, as they did in the past, and may hurt equities. At the same time, the US dollar and other safe havens could come under some buying interest.

On the other hand, any discussion suggesting that the time for scaling back monetary policy has not come yet, or anything pointing to a very slow pace of tightening, may encourage market participants to increase their risk exposure a bit more.

Speaking about central banks, today, during the Asian session, the RBA released the minutes from this month’s meeting, where policymakers stood pat and reiterated that, at the July meeting, they will consider further bond purchases. In the minutes, it was revealed that their decision will depend upon the Board’s goals for employment and inflation, as well as the likely effect of deferent options on the overall financial conditions.

With inflation standing at +1.1% yoy, well below the lower end of the Bank’s target range of 2-3%, AUD-traders may have stayed convinced that there are decent chances for policymakers to add to their program, and that’s why they pushed the aussie slightly lower.

In any case, the next focal point may be the employment report for May, due to be released on Thursday. In our view, a stronger-than-expected report may be needed for market participants to discount a smaller probability for a QE extension.

Nikkei 225 Technical Outlook

The Nikkei 225 continued to grind higher, while trading above a short-term tentative upside support line drawn from the low of May 13. Yesterday, the cash index managed to overcome the previous highest point of June, at 29271, and today was trying to make its way towards the highest point of May, at 29686. For now, we will take a positive approach and aim higher, at least in the near term.

If the index continues to rally, it could reach the highest point of May, at 29686, where a temporary hold-up may occur. The price might even retrace back down from there, but if it remains somewhere above the aforementioned upside line, this could interest the bulls again.

If so, they might jump behind the steering wheel and drive Nikkei 225 towards the 29686 obstacle again, a break of which would confirm a forthcoming higher high. Such a move could clear the way towards the area between the 29981 and 30077 levels, marked by the highs of Apr. 12 and 9, respectively.

On the other hand, if the previously discussed upside line breaks and the price falls below the 29100 hurdle, marked by yesterday’s low, that could invite more sellers into the game, as such a move might change the direction of the current short-term trend.

Nikkei 225 may fall to the 28755 obstacle, a break of which could clear the way to the current lowest point of June, at 28555, where the price might stall for a bit. That said, if the bears are still feeling strong, they may drag the index even lower, possibly targeting the 28350 level. That level marks the lows of May 25 and 27.

AUD/USD Technical Outlook

Although AUD/USD was trading below a short-term tentative downside resistance line taken from the high of May 18, at the same time, the rate continued to balance above a short-term upside support line drawn from the low of Apr. 1. This means that the pair could be coiling up. But there seems to be plenty of space for maneuverability in between those lines, so we might even see a move higher again in the near term.

A small decline and a drop below the 0.7688 hurdle, marked by the low of June 11, could send the rate closer to the aforementioned upside line, which if stays intact, may invite the bulls back into the game.

If so, AUD/USD might travel back to the 0.7725 barrier, marked by yesterday’s high, a break of which could clear the path towards the previously discussed downside line, which may provide a hold-up.

Alternatively, if that upside line breaks and we see a rate-drop below the 0.7645 hurdle, marked by the current lowest point of June, that would confirm a forthcoming lower low, possibly setting the stage for further declines, as more sellers might join in.

AUD/USD may then fall to the 0.7622 obstacle, a break of which could open the door for a move to the 0.7585 level, marked by the low of Apr. 13.

As For The Rest Of Today's Events

During the early European morning, we already got the UK employment report for April. The unemployment rate ticked down to 4.7%, as expected, while the employment change revealed that the economy added less-than-forecast jobs in the three months to April.

Average weekly earnings, both including and excluding bonuses, accelerated by more than expected. The pound barely reacted to the report, perhaps as GBP-traders were still waiting for tomorrow’s CPIs for May, and Friday’s retail sales for the month.

Later, from the US, we get the retail sales and PPIs for May, as well as the New York Empire State manufacturing index for June. The headline PPI is expected to have ticked up to +6.3% yoy from +6.2%, while the core rate is forecast to have jumped to +4.8% yoy from +4.1%. Headline sales are anticipated to have fallen 0.8% mom after stagnating in April, but core sales are expected to have rebounded 0.4% mom after sliding 0.8%. The New York index is expected to have declined slightly, to 22.00 from 24.30.

We also have one speaker on today’s agenda and this is BoE Governor Andrew Bailey.