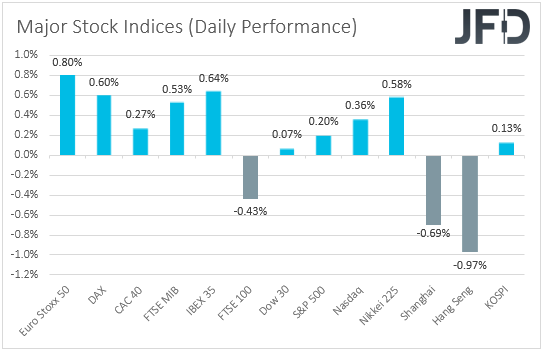

Most major equity indices continued trading north yesterday, perhaps due to investors having second thoughts over the potential economic impact the fast-spreading Delta variant of the coronavirus could have. Investors may have kept increasing their risk exposure also due to a dovish ECB. The Bank kept its policy unchanged, but changed its forward guidance to signal that interest rates are likely to stay at present or lower levels for much longer than previously assumed.

Sentiment Stays Supported, EUR Slides After Dovish ECB

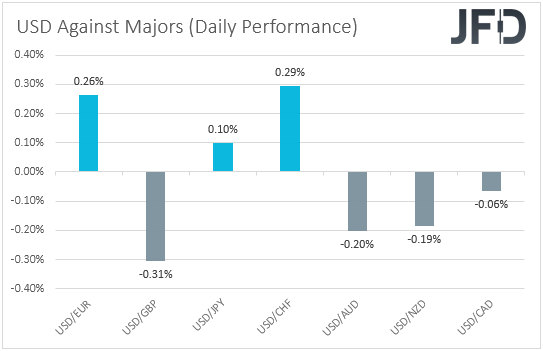

The US dollar traded mixed against the other major currencies on Thursday and during the Asian session Friday. It gained versus CHF, EUR, and JPY in that order, while it underperformed against GBP, AUD, NZD, and CAD.

The weakening of the franc and the yen, combined with the slight strengthening of the risk-linked Aussie, Kiwi and Loonie, suggests that markets continued to trade in a risk-on fashion yesterday. Indeed, turning our gaze to the equity world, we see that major EU indices traded in the green, with the only exception being UK’s FTSE 100, which may have slid due to a strengthening pound. Remember that many companies of the index generate profits in other currencies, so in a strengthening GBP environment, if those profits are converted to pounds, they worth less. Appetite, although relatively softer, remained supported during the US session as well, but deteriorated further today in Asia.

In our view, market participants continued to buy stocks as a result of having second thoughts over the potential economic impact the fast-spreading Delta variant of the coronavirus could have. As we’ve been highlighting the last couple of days, with vaccinations limiting the severity of symptoms of new cases, new measures may not be as restrictive as previously. Investors may have kept increasing their risk exposure also due to the outcome of the ECB monetary policy decision. As was widely expected, the Bank kept all of its settings untouched and changed its forward guidance, saying that it will keep interest rates at present or lower levels until it sees inflation reaching 2% well ahead of the end of its projection horizon, which may also imply a period during which inflation moderately overshoots that objective. This translates into willingness to hold rates low for much longer than the previous guidance suggested.

The euro gained initially, perhaps due to the lack of a more dovish outcome, as what we got was what was expected. However, it pulled back later in the day to be found as the second biggest loser today morning, as investors may have resumed their monetary-policy-divergence bets. With the ECB pledging to stay ultra-loose for longer, while the Fed and the RBNZ have already started discussing the timing of when they should start withdrawing support, we do see the case for EUR/USD and EUR/NZD to drift south in the foreseeable future.

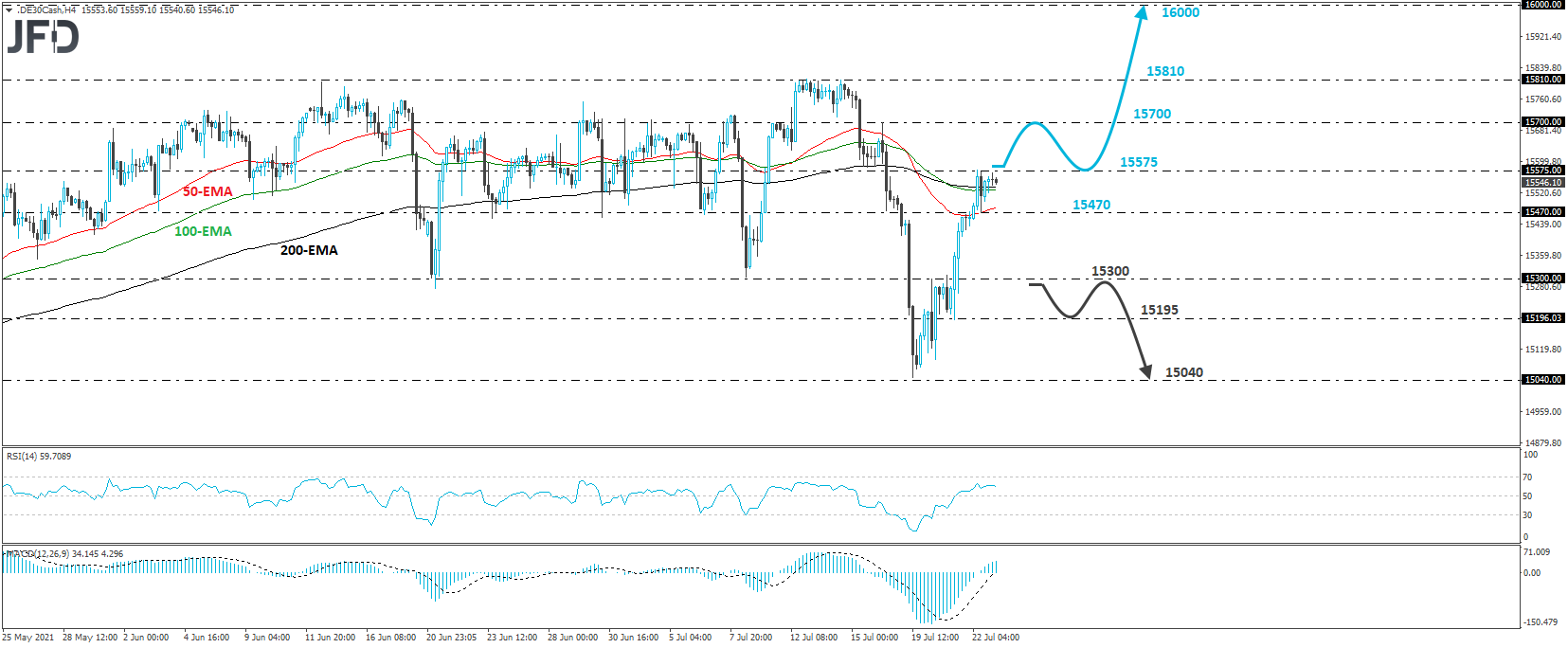

DAX Technical Outlook

The German DAX index continued to recovery yesterday and managed to hit resistance at 15575. That said, with no signs of a reversal back down, we would see decent chances for the recovery to continue for a while more.

A clear break above 15575 would confirm a forthcoming higher high and may pave the way towards the peak of July 16, at 15700. Another break, above 15700, could extend the advance towards the index’s record high of 15810, hit on July 13. If investors are not willing to stop there this time around, the next area to consider as a resistance may be the psychological zone of 16000.

On the downside, we will start examining the case of decent declines upon a break below the 15300 hurdle, marked by Tuesday’s inside swing high. This could initially target the low of the day after, at around 15195, the break of which could extend the fall towards the low of July 19, at 15040.

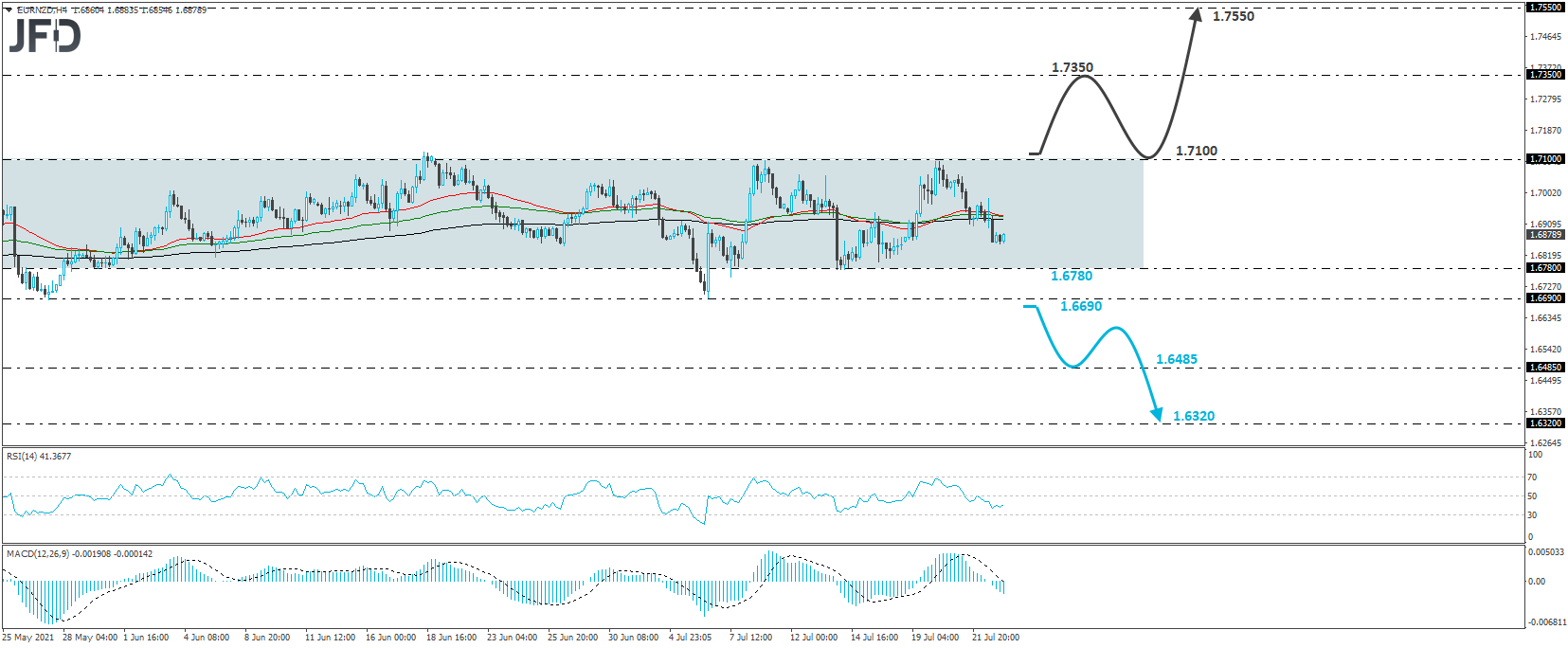

EUR/NZD Technical Outlook

EUR/NZD traded lower yesterday, but stayed within the sideways range, between 1.6780 and 1.7100, that has been containing most of the price action since May 12th. As long as the rate stays within that range, we will adopt a neutral approach, but taking into account the aforementioned fundamentals, we would see more chances for the pair to exit the range to the downside rather than to the upside.

A break below the lower end of the range at 1.6780, or even better, below the low of July 6, at 1.6690, could turn the short-term outlook bearish and perhaps encourage the bears to dive towards the lows of Mar. 17 and 18, at around 1.6485. If that level is also broken, then the slide may get stretched toward the low of Feb. 24, at 1.6320.

Now, in order to turn our gaze to the upside, we would like to see a move above the upper end of the range, which is at 1.7100. Such a move would confirm a forthcoming higher high on both the 4-hour and daily charts and may see scope for advances towards the 1.7350 zone, which provided resistance on Nov. 13, as well as on Dec. 21 and 22.

As For The Rest Of Today's Events

During the early European morning, we already got the UK retail sales for June, with the headline rate rebounding by more than expected, and the core one rebounding by less than anticipated.

Later in the day, we have the preliminary PMIs for July from the Eurozone, the UK, and the US. In the Euro area, the manufacturing index is expected to decline to 62.5 from 63.4, while the services one is forecast to rise to 59.6 from 58.3. This is likely to take the composite index slightly higher, to 60.0 from 59.5. Although this would mean some further recovery in the bloc’s economy, we doubt that it would be enough to lift the euro, especially with the coronavirus Delta variant posing fresh risks to the economy, and the ECB pledged to keep its policy extra-loose for longer. In the UK, all indices are expected to decline somewhat, while the US ones are forecast to come in on the mixed side. The manufacturing one is expected to slide somewhat, while the services one is forecast to have inched fractionally higher.

Canada’s retail sales for May are also due to be released, with both headline and core sales expected to have continued to slide, but at a slower pace than in April.