Friday November 17: Five things the markets are talking about

The mighty U.S dollar begins the last trading session on the back foot against most of its major peers as a probe into Russian influence on the 2016 U.S election is said to have deepened.

Note: Special Counsel Robert Mueller is said to have served Trump’s election campaign a subpoena in mid-October – this suggests that his ongoing criminal investigation is aggressively pursuing links between campaign officials and Russia.

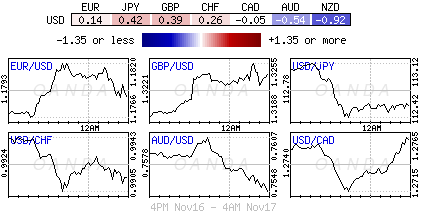

Elsewhere, global equities have produced some mixed results overnight as the EUR (€1.1796) strengthened.

This morning’s Canadian CPI data (08:30 am EDT) will be crucial since BoC governor Poloz defended the central bank’s upbeat inflation projections in his last speech. The market is pricing in odds of +40% that the BoC hikes in January.

1. Stocks mixed results

In Japan, the Nikkei share average rose to a one-week high overnight, helped by gains in most sectors. The Nikkei ended +0.2%, it’s highest closing since Nov. 10. However, it fell -1.3% for the week, snapping a nine-week winning streak. The broader Topix gained +0.1%.

Down-under, Aussie shares rose modestly, trimming the week’s slide as the country’s big banks provided support. The S&P/ASX 200 rose +0.2%, resulting in a -1.2% weekly drop for the index.

In Hong Kong, stocks followed regional indices higher, with sentiment aided by strong Wall Street earnings and a step forward on U.S tax reform. The Hang Seng index rose +0.6%, while the China Enterprises Index gained +0.7%. For the week, the Hang Seng gained +0.7%, while HSCE lost -1.2%.

In China, stocks have their worst week in three-months amid worries on the domestic economy. The blue-chip Shanghai Shenzhen CSI 300 index rose +0.4% for the day, while the Shanghai Composite Index closed down -0.5%. For the week, the CSI300 was up +0.2% and the SSEC lost -1.5%.

In Europe, stocks have opened largely flat and moved lower as the session progresses. There is attention on the Italian banking sector again as banks are having difficulty raising capital. Elsewhere, energy stocks are supported by crude oil prices.

U.S stocks are set to open in the ‘red’ (-0.2%).

Indices: Stoxx50 -0.2% at 3,554, FTSE -0.2% at 7,370, DAX -0.1% at 13,031, CAC 40 -0.2% at 5,325, IBEX 35 -0.4% at 10,043, FTSE MIB -0.6% at 22,073, SMI -0.2% at 9,130, S&P 500 Futures -0.2%

2. Oil set for first weekly fall in six on oversupply, gold higher

Oil prices have rallied overnight, but remained en route for their first week of losses in six, as concerns grew over Russia’s support for an extension of the crude output cuts.

Brent crude oil is up +50c at +$61.86 a barrel, while U.S light crude is at +$55.90 a barrel, up +76c.

Note: Prices are set to fall between -2 and -4% for the week as a whole.

An agreement by the OPEC and other producers such as Russia to limit oil production has propped up prices in recent months, with the deal expected to be extended at the group’s next meeting on Nov. 30.

However, Russian support for a formalized extension of production cuts at the next OPEC meeting appears questionable, even if only to defer the decision to Q1 next year.

Gold prices rally as the ‘mighty’ dollar weakens on report Trump’s election campaign has been subpoenaed. Spot gold is up +0.2% at +$1,281.51 per ounce. It is up about +0.5% for the week and is poised to post a second straight weekly gain.

3. Yields curves continue to flatten

U.S bonds continue to ‘flash’ some uncomfortable warning signs about the U.S economy, as the gap between longer-term and shorter-term yields narrows even further. The U.S benchmark spread (2/30) is back below +70 bps.

Note: The past seven U.S recessions came following ‘inversions’ curve, so the longer the current flattening goes, the more nervous the market becomes.

From here, sovereign yields are expected to range trade for the remainder of this year now that the Fed’s rate increase for December is almost fully priced in, and while the ECB has set its course for most of 2018.

The yield on 10-year Treasuries has fallen -1 bps to +2.36%, while in Germany, the 10-year Bund yield has gained +1 bps to +0.39%, the biggest gain in a week. In the U.K, the 10-year Gilt yield has climbed +2 bps to +1.324%.

4. Dollar under pressure

The USD is trading softer against its Tier 1 currency pairs, mostly on the back of reports that special counsel Robert Mueller has issued a subpoena to President Trump’s election campaign back in mid-Oct in relation to documents on Russia.

Note: This is the first time that Mueller has officially requested information from the campaign.

The EUR/USD higher by +0.2% at €1.1795, while USD/JPY is off by -0.4% at ¥112.55.

In EM pairs, the Turkish lira again trades under pressure after Turkey’s President Erdogan again criticized the central bank. The market is pricing in the risk that the CBRT may do something wrong only because its been pressured into further easing. EUR/TRY is trading atop of €4.59 area, higher by +0.9%.

Down-under, both the Aussie (A$0.7544, down -0.4%) and Kiwi (NZ$0.6785, down -0.85%) pairs are again underperforming, pressured by China’s growing theme that domestic credit and growth were slowing down and would negatively impact Australia and New Zealand’s economy.

5. Draghi’s comments

With little data out during the Euro session, the market focused on ECB’s Draghi comments from a banking conference in Frankfurt. His comments were in-line with recent October policy statement.

He noted that the Euro region was in the midst of economic recovery with increasing confidence that the robust momentum would continue going forward. He did not see inflation moving steadily away from the very low levels of recent years.

He again reiterated the council’s view that they were not at a point where the recovery or inflation could be self-sustained without the current accommodative monetary policy. Extension of QE had anchored rate expectations.