Moody's Investors Service, a rating arm of Moody's Corporation (NYSE:C) , upgraded the ratings outlook of Citigroup Inc. (NYSE:C) and its subsidiaries to ‘positive’ from ‘stable’. However, the firm affirmed all the ratings.

The Wall Street biggie’s senior debt rating has been maintained at Baa1. Additionally, long-term deposit rating, issuer and senior debt ratings for its subsidiary — Citibank N.A. — has been retained at A1, short-term deposit rating at Prime-1, and baseline credit assessment at baa2, with counterparty risk assessment of A1(cr)/P-1(cr).

Reason for the Upgrade in Outlook

The completion of Citigroup’s restructuring to focus on core operations, resulting in strong asset risk profile and stability in earnings, along with strengthened capital market operations, propelled Moody’s for the upgrade. Per the rating firm, the company’s streamlining efforts have concentrated its geographic footprint and helped Citigroup in making its business more durable and increased focus on institutional client and consumer customer base.

Why are the Ratings Affirmed?

Per Moody's, Citigroup faces tremendous competition in various key businesses, including retail banking and credit cards in the U.S., as well as capital markets worldwide. The bank is striving hard to improve returns for its shareholders.

Among others, management aims to return capital over earnings, along with the capital released by DTA utilization, only after recording Common Equity Tier One ratio at 11.5%, down from the current ratio of 13%. The company believes this would help drive profitability and achieve its target of return on tangible common equity of 11% by 2020.

Additionally, Citigroup has been putting in efforts to improvise profits in its lines of business, including the credit card and retail bank unit in the United States, as well as the CitiBanamex franchise in Mexico. All these objectives aim at recording return on assets ("ROA") in the range of 90-110 basis points.

However, affirming ratings, Moody's views intense competition to act as headwind in accomplishing such targets. Notably, on the cost front, Citigroup has reduced costs since 2014, reporting drop in the cost income ratio to 57% in the first nine months of 2017, from 71% recorded in 2014.

Overall, according to Moody's, Citigroup is well placed among competitors with its strategic streamlining efforts and the unique global consumer strategy, which targets high-profile clients worldwide, resulting in steady earnings and huge deposits base.

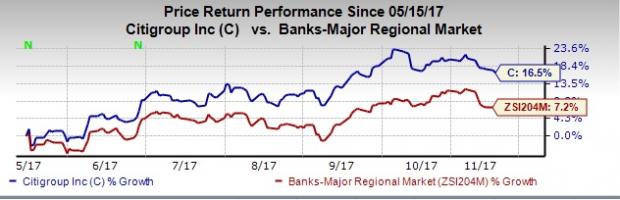

Citigroup currently carries a Zacks Rank #3 (Hold). The company’s stock has outperformed 7.2% growth registered by the industry, over the past six months, gaining 16.5%.

Stocks to Consider

Enterprise Financial Services Corporation (NYSE:C) has been witnessing upward estimate revisions for the last 30 days. Additionally, the stock jumped more than 14% over the past year. It currently carries a Zacks Rank of 2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

First Financial Bancorp (NYSE:C) has been witnessing upward estimate revisions for the last 30 days. Also, the company’s shares have risen nearly 5.6% over the past year. It holds a Zacks Rank of 2, at present.

The Hottest Tech Mega-Trend of All

Last year, it generated $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce "the world's first trillionaires," but that should still leave plenty of money for regular investors who make the right trades early.

See Zacks' 3 Best Stocks to Play This Trend >>

Citigroup Inc. (C): Free Stock Analysis Report

Moody's Corporation (MCO): Free Stock Analysis Report

First Financial Bancorp. (FFBC): Free Stock Analysis Report

Enterprise Financial Services Corporation (EFSC): Free Stock Analysis Report

Original post