The signs are unmistakable. China's economic growth rate is slowing. Notwithstanding the anomalous official July PMI number that many viewed with skepticism, economic releases, one after another, point to a slowing economy.

Now China is set to suffer from the Skyscraper Curse, according to Bloomberg:

On July 20, the Broad Group broke ground on Sky City on the outskirts of the south-central city of Changsha. The skyscraper will rise 838 meters (2,749 feet) into the heavens to become the world’s tallest building. If that weren’t feat enough, the project aims to wrap up construction in 90 days and at almost half the cost of Dubai’s Burj Khalifa, which it would top.

As I have pointed out before, the planning and construction of the world's tallest building has been a contrarian sell signal. That point was elaborated on by Bloomberg:

[T]he experiences of Japan, Malaysia, the United Arab Emirates and the U.S. show an uncanny correlation between architectural one-upmanship and economic doom. In the 1920s, for example, New York’s Chrysler and Empire State buildings opened amid the Great Depression. Later, New York’s World Trade Center and Chicago’s Sears Tower presaged fiscal crises and the breakdown of the Bretton Woods system.

Mitigating a downturn

Michael Pettis had been writing about the inherent contradictions and the instability of China's growth path and the inevitable slowdown. In a recent FT article, he wrote that a Chinese slowdown does not necessarily have to be a disaster. The key is to re-balance growth from an export and infrastructure focus to a household focus. If household incomes rise sufficiently, social and political tensions will be contained so that China's political system holds together:

China’s GDP, in other words, does not need to grow at 7 per cent or even 6 per cent a year in order to maintain social stability. This is a myth that should be discarded. What matters for social stability is that ordinary Chinese continue to improve their lives at the rate to which they are accustomed, and that the Chinese economy is restructured in a way that allows it to tackle its credit bubble.

If household income can grow annually at 6-7 per cent, income will double in 10 to 12 years, in line with the target proposed by Premier Li Keqiang in March during the National People’s Congress. What is more, if China can do this while the economy is weaned off its addiction to credit, it will be an extraordinary achievement, even if it implies, as it must, that GDP grows far more slowly that the growth rates to which we have become accustomed.

I would make the analogy to Japan's Lost Decades. Despite over two decades of slow and no growth, social tensions have not risen to the extent that there have been few mass protests and talk of government overthrow.

That's only part of the equation. Despite the lack of a social and political blow-up in Japan, investors in Japan have been decimated since the bubble top of the early 1990's. Andy Xie believes that China will follow a similar path to that of Japan rather than Southeast Asia during the Asian crisis:

China’s property market will adjust similar to what happened in Japan and Taiwan rather than in Hong Kong or Southeast Asia. The former was gradual, and the latter fast.

In 1998, banks in Southeast Asia owed short-term dollar debts to Western banks. When the debts were not rolled over, these countries had to raise real interest rates enormously to contract domestic credit in order to pay off foreign creditors. Surging real interest rates caused their property markets to drop off a cliff.

The Chinese owe the debt to themselves and not foreigners. Therefore the adjustment process can be more gradual rather than catastrophic:

The debts in China’s property bubble are mostly held by local governments and property developers. Total household debt is one-third of GDP, compared to nearly 100 percent when the United States’ bubble burst in 2008 and Japan’s in 1992. On balance, the bursting of the property bubble will boost China’s household demand. The lower property prices will decrease the need for savings.

Financial contagion risk

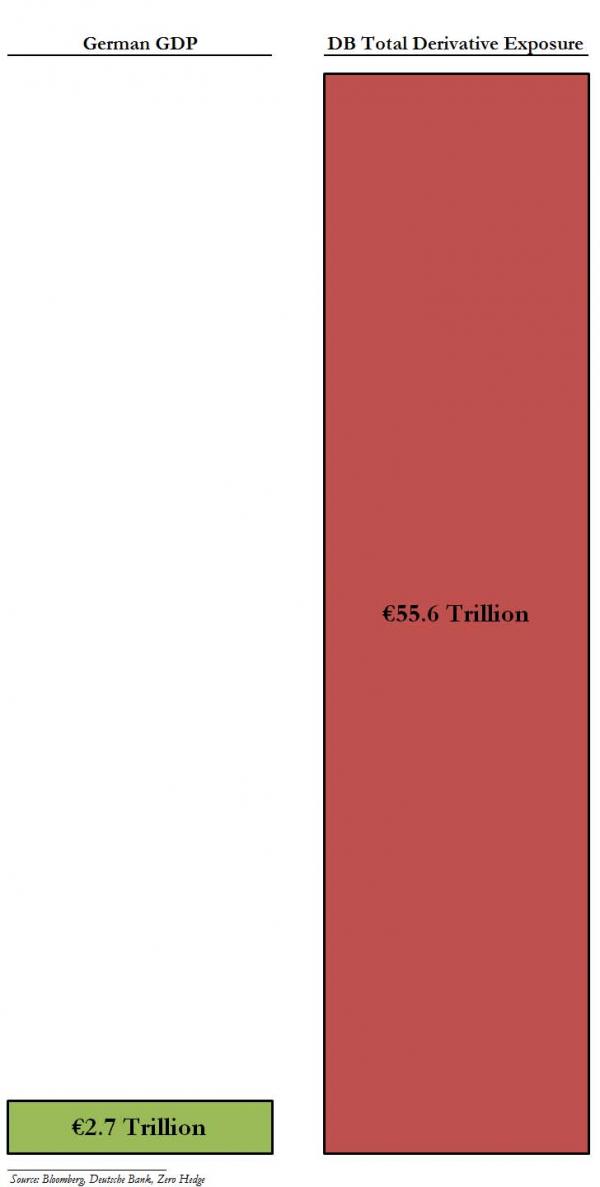

While I respect these points of view, I remain concerned about the risk of financial contagion. Consider this Zero Hedge post about the size of Deutsche's derivative book relative to its own balance sheet. Can anyone truly say that there isn't a bank (e.g. Deutsche, JP Morgan, HSBC, etc.) that doesn't have some outsized derivative exposure to China?

We have seen what happened to the credit markets when the talk of Fed tapering hit the tape. Supposing that China's economy unwound itself in a disorderly way, leaving the formal and shadow banking system with sky-high, non-performing loans. Wouldn't a risk premium on other EM paper surge?

Even if Deutsche, JP Morgan, HSBC, etc. were to be insulated from direct credit risk in China, you can't tell me that these same global banks aren't insulated from rising risk premiums on EM paper like Brazil, Turkey, India or Indonesia?

China slowdown story moving from page 12 to page 1

It is said that investors can make money by identifying an investment story or thesis that moves from page 12 to page 1 of the newspaper. I have been writing about the risks to China for quite some time, but I see that George Friedman of Stratfor has penned an article echoing much of Pettis' thoughts. The article is entitled Recognizing the End of the Chinese Economic Miracle where he discusses the topics of China's unstable growth model and how the leadership can navigate the slowdown by re-focusing growth and the beneficiaries of growth [emphasis added]:

The Chinese are not going to completely collapse economically any more than the Japanese or South Koreans did. What will happen is that China will behave differently than before. With no choices that don't frighten them, the Chinese will focus on containing the social and political fallout, both by trying to target benefits to politically sensitive groups and by using their excellent security apparatus to suppress and deter unrest. The Chinese economic performance will degrade, but crisis will be avoided and political interests protected. Since much of China never benefited from the boom, there is a massive force that has felt marginalized and victimized by coastal elites. That is not a bad foundation for the Communist Party to rely on.

I have followed Stratfor for years and I value their analysis as a barometer of how the Inside the Beltway thinking evolves. Now that even Stratfor is trumpeting the China slowdown thesis and how the leadership can navigate the turmoil, investors can expect that the markets will start to think more about the risks to a China slowdown and price the risk accordingly (recall the page 12 to page 1 analogy).

Canaries in the Chinese coalmine

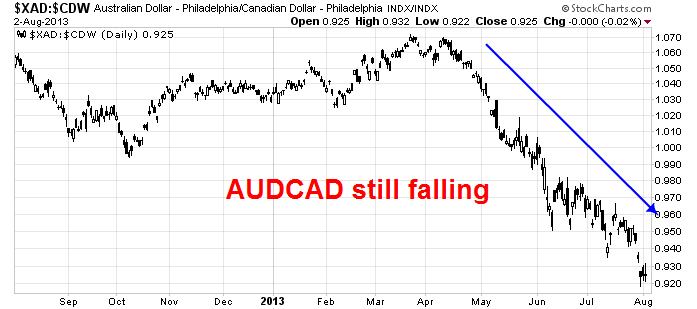

Investors can get on top of this by monitoring critical indicators of Chinese growth and financial fragility. I have been watching the AUD/CAD cross rate, as both Australia and Canada are commodity producing economies but Australian exports are more sensitive to Chinese exports while Canadian exports are more levered to the US. Right now, the AUD/CAD exchange rate isn't looking very healthy:  AUD/CAD" width="697" height="309">

AUD/CAD" width="697" height="309">

Industrial commodity prices, another key indicator, remain in a downtrend. However, there may be some hopeful signs of stabilization, but I would not want to sound the all-clear until this index rallies through the downtrend line.

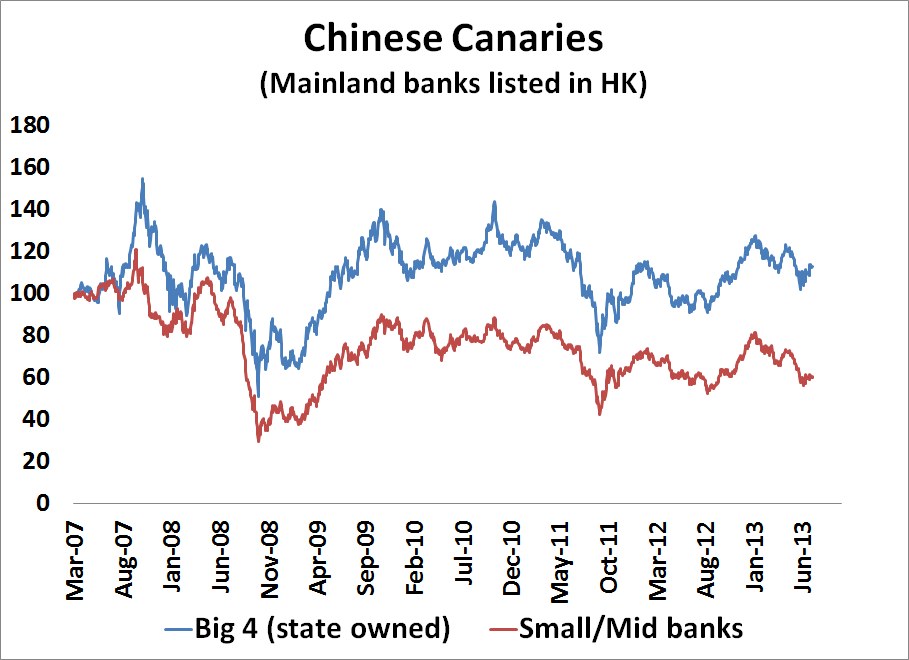

Finally, my Chinese canaries index of Chinese mainland bank stocks listed in Hong Kong as a measure of the degree of perceived stress in China's financial system is indicating elevated stress levels. In particular, the small and mid sized bank stocks (shown in red) are nearing the lows set during the Eurozone crisis of 2011.

Will China crash? If it does, will it take the global financial system down in a repeat of the Lehman Crisis?

I have no idea. The risks have always been there but the Stratfor article suggests that the market spotlight is turning onto this topic and I would expect risk premiums to rise accordingly. Investors can monitor the risks using some of the metrics that I have detailed in order to get a better handle on the situation.

Disclosure: Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. ("Qwest"). This article is prepared by Mr. Hui as an outside business activity. As such, Qwest does not review or approve materials presented herein. The opinions and any recommendations expressed in this blog are those of the author and do not reflect the opinions or recommendations of Qwest.

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or Mr. Hui may hold or control long or short positions in the securities or instruments mentioned.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

China Macro Risk Rising; Will Financial Contagion Follow?

Published 08/05/2013, 02:12 AM

Updated 07/09/2023, 06:31 AM

China Macro Risk Rising; Will Financial Contagion Follow?

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Very thoughtful article. My only doubt is whether the Chinese will be able to contain the social unrest that will follow the drop in GDP growth rate.Though they have been crushing any unrest, if it spreads all over China, it will be very difficult to contain. Secondly, I want to understand the impact of the huge foreign exchange reserves that China holds. Will the foreign exchange reserves have a role in the final analysis?

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.