The USD is on the rise again, but today is an awkward “half holiday” (closed bond market due to banking holiday) in the US, so we may not get out answer on the status of the USD until mid-week.

Today is one of those banking holidays in the US that means the bond market is closed, but that the equity market is open. But with Friday offering up such an interesting close, the market has been trying to press its case a bit, as EURUSD fell in earnest early in the day and the JPY drifted noticeably back to the strong side as well. But a bounce in risk and a weaker USD towards the early US hours suggests we may have to wait until tomorrow’s action before we get more decisive moves here (a firmer move below 1.0150 in AUDUSD, for example, or a potential follow-up move higher in USDCAD after Friday’s reaction to Canada’s strong jobs report. And in EURUSD, the 1.2950/1.3000 zone is shaping up as a pivot area) In other words, we got the set-up with the Friday close, but we’ve yet to find full confirmation that the top is in here for risk appetite/bottom is in for the USD, though the evidence is leaning that way.

China’s Services PMI and Aussie

The HSBC measure of strength in the Chinese services sector showed a stronger than expected reading, and the Aussie finally started showing a little resilience in today’s European session, though if we look at the rate picture in Australia, there was hardly any reaction, and precious metals sold off again today, even if volatility wasn’t particularly pronounced. An interesting story that has gotten a bit of press lately is the pressure on Australian banks, whose costs are “relentlessly” increasing as depositors are still paid at relatively high rates in Australia. This article from BusinessWeek makes everything sound like smooth sailing, but Australian banks will be hard pressed on funding if risk appetite weakens from here, and it is interesting to note how much the Aussie has weakened of late in broad terms despite nose-bleed levels of complacency. Imagine what the currency would do if actual worry was evident in the standard global measures of risk…. So keep an eye on risk appetite, precious metals and now perhaps Australia bank share prices as well as general confirming indicators on the direction in Aussie from here. I’m actually wondering if it isn’t time for NZD to play a little catchup, particularly on the NZDUSD reversal on Friday and as the sub-0.8200 support areas are in play.

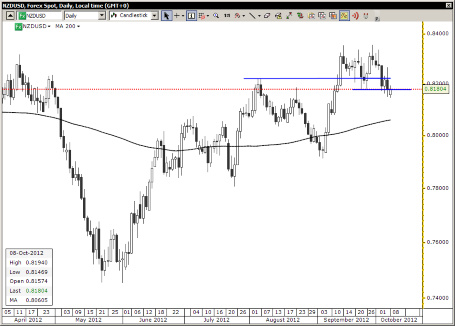

Chart: NZD/USD

This chart has been on a bit of “artificial” support from a wild sell-off in AUDNZD, but Friday’s reversal may finally be seeing the pair tilting fully back into the old range toward 0.8000, provided US equity markets don’t launch yet another rally attempt to new highs for the year. This 0.8150/0.8200 area looks pivotal for the near term outlook for NZDUSD.

NZD/USD" title="NZD/USD" width="455" height="326" />

NZD/USD" title="NZD/USD" width="455" height="326" />

Looking ahead

The Euro resilience may take at least a bit of a pause from here as positioning has been significantly neutralized (the net short is a mere shadow of its former self in the US futures market, for example) and as we face a key series of political EU event risks in coming days with various meetings, including a meeting of EU Finance ministers taking place today and tomorrow, and the EU parliament will be debating EU banking union proposals on Wednesday. This may be the week where the market wakes up to the same problems the EU has been having all along and scratching its head at why the single currency is trading at 1.29 versus the dollar when 1.19 is probably too expensive in the longer run… Look at this post from MISH that discusses the massive support for independence in Italy. And we have EU politicians discussing banking unions and the EU commission’s Barroso talking up the idea of an EU federation? I don’t quite see that yet from where I am sitting. By the way, that being the case, it’s curious to see EURGBP pushing the upper range resistance – looking for some kind of reversal there and in EURCHF before I believe that the Euro downside is going to get more trading focus in the days ahead. Stay tuned.

And stay careful out there.

Economic Data Highlights

Today is one of those banking holidays in the US that means the bond market is closed, but that the equity market is open. But with Friday offering up such an interesting close, the market has been trying to press its case a bit, as EURUSD fell in earnest early in the day and the JPY drifted noticeably back to the strong side as well. But a bounce in risk and a weaker USD towards the early US hours suggests we may have to wait until tomorrow’s action before we get more decisive moves here (a firmer move below 1.0150 in AUDUSD, for example, or a potential follow-up move higher in USDCAD after Friday’s reaction to Canada’s strong jobs report. And in EURUSD, the 1.2950/1.3000 zone is shaping up as a pivot area) In other words, we got the set-up with the Friday close, but we’ve yet to find full confirmation that the top is in here for risk appetite/bottom is in for the USD, though the evidence is leaning that way.

China’s Services PMI and Aussie

The HSBC measure of strength in the Chinese services sector showed a stronger than expected reading, and the Aussie finally started showing a little resilience in today’s European session, though if we look at the rate picture in Australia, there was hardly any reaction, and precious metals sold off again today, even if volatility wasn’t particularly pronounced. An interesting story that has gotten a bit of press lately is the pressure on Australian banks, whose costs are “relentlessly” increasing as depositors are still paid at relatively high rates in Australia. This article from BusinessWeek makes everything sound like smooth sailing, but Australian banks will be hard pressed on funding if risk appetite weakens from here, and it is interesting to note how much the Aussie has weakened of late in broad terms despite nose-bleed levels of complacency. Imagine what the currency would do if actual worry was evident in the standard global measures of risk…. So keep an eye on risk appetite, precious metals and now perhaps Australia bank share prices as well as general confirming indicators on the direction in Aussie from here. I’m actually wondering if it isn’t time for NZD to play a little catchup, particularly on the NZDUSD reversal on Friday and as the sub-0.8200 support areas are in play.

Chart: NZD/USD

This chart has been on a bit of “artificial” support from a wild sell-off in AUDNZD, but Friday’s reversal may finally be seeing the pair tilting fully back into the old range toward 0.8000, provided US equity markets don’t launch yet another rally attempt to new highs for the year. This 0.8150/0.8200 area looks pivotal for the near term outlook for NZDUSD.

NZD/USD" title="NZD/USD" width="455" height="326" />Looking ahead

The Euro resilience may take at least a bit of a pause from here as positioning has been significantly neutralized (the net short is a mere shadow of its former self in the US futures market, for example) and as we face a key series of political EU event risks in coming days with various meetings, including a meeting of EU Finance ministers taking place today and tomorrow, and the EU parliament will be debating EU banking union proposals on Wednesday. This may be the week where the market wakes up to the same problems the EU has been having all along and scratching its head at why the single currency is trading at 1.29 versus the dollar when 1.19 is probably too expensive in the longer run… Look at this post from MISH that discusses the massive support for independence in Italy. And we have EU politicians discussing banking unions and the EU commission’s Barroso talking up the idea of an EU federation? I don’t quite see that yet from where I am sitting. By the way, that being the case, it’s curious to see EURGBP pushing the upper range resistance – looking for some kind of reversal there and in EURCHF before I believe that the Euro downside is going to get more trading focus in the days ahead. Stay tuned.

And stay careful out there.

Economic Data Highlights

- China Sep. HSBC Services PMI out at 54.3 vs. 52.0 in Aug.

- Switzerland Sep. Unemployment Rate fell to 2.9% vs. 3.0% expected and 2.9% in Aug.

- Germany Aug. Trade Balance out at +16.3B

- Switzerland Sep. CPI out at +0.3% MoM and -0.4% YoY as expected

- Euro Zone Oct. Sentix Investor Confidence out at -22.2 vs. -20.9 expected and -23.2 in Sep.

- Germany Aug. Industrial Production fell -0.5% MoM and -1.4% YoY vs. -0.6%/-1.6% expected, respectively and vs. -1.3% YoY in Jul.

- New Zealand Sep. Credit Card Spending (2145)

- New Zealand Sep. QV House Prices (2300)

- UK Sep. BRC Sales Like-for-Like (2301)

- UK Sep. RICS House Price Index (2301)

- Japan Aug. Current Account (2350)

- Australia Sep. NAB Business Conditions/Confidence (0030)

- Australia RBA’s Lowe to Speak (0100)