Everyone is predicting the demise of Barnes & Noble, Inc. (NYSE:BKS) with good reason. A closer look at the numbers reveals a company in financial distress.

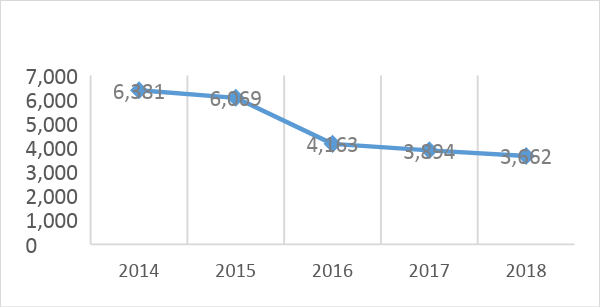

- Sales have decreased $3.2 billion or 46% in the last five years.

- Net profit margin has not cracked 1% and has experienced losses in three of the last five years.

- The current ratio is at 1.05 at the end of the fiscal year 2018.

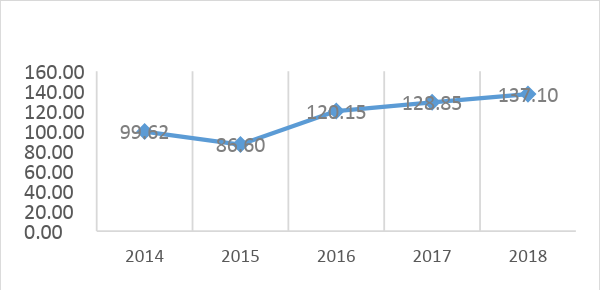

- Inventory days have increased consistently in the last five years from 99.62 days of inventory in 2014 to a whopping 137.1 days of inventory in 2018.

Source: 10K & Quarterly Filings

Yet, those numbers do not begin to tell the story.

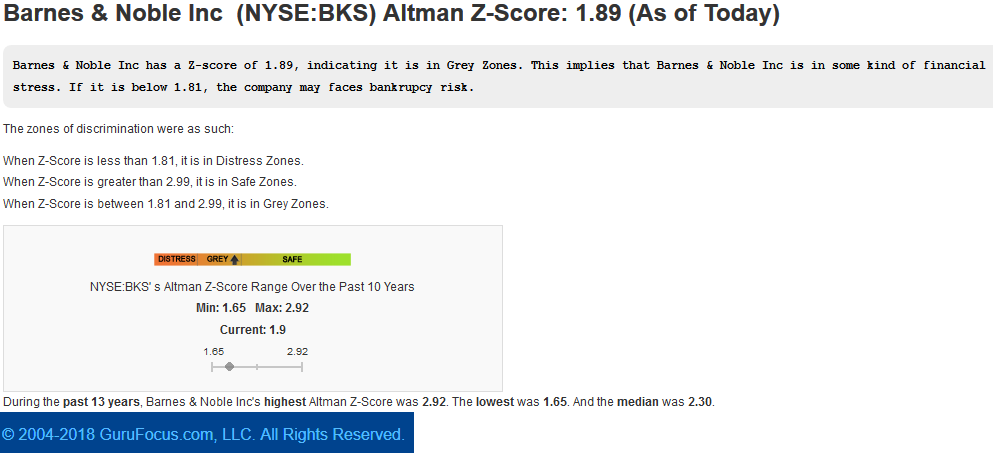

The Altman Z-Score bankruptcy predictor

The Altman Z-score has been successfully used to predict bankruptcy. The median Z-score for a stable business is usually between 1.81 and 2.99. Barnes & Noble’s Z-score is close to reaching distress levels, as it decreased from 2.34 in 2017 to 1.89 in 2018. For comparative purposes, Amazon’s current Z-Score is 7.70. With all these financial indicators trending negatively, Barnes & Noble has shown extraordinary resiliency at avoiding bankruptcy.

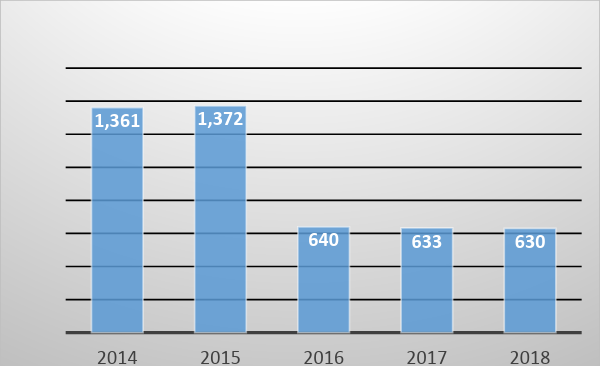

After Amazon (NASDAQ:AMZN) and Kindle disrupted their business, the company has downsized, going from 1361 stores in 2014 to 630 stores in 2018. They also no longer have preferred stock on its balance sheet and spun off the educational business. However, they have kept shareholders happy by maintaining a high-yield dividend, which will soon become in jeopardy if they cannot stop their revenue decline.

Can the company turn this around?

It’s unlikely we’ll see Barnes & Noble disappear in 2018 or 2019. The company's 2018 financials were accompanied by an unqualified opinion from their auditors Ernst & Young LLP. Auditors have unlimited access to the company’s records and employees to determine if the business has any going concern issues. Also, for a company to be classified with going concern issues, there must be another two items present: recurring losses and negative cash flows from operations. If there's a silver lining for Barnes & Noble financial situation, it is that they've been able to maintain an average gross profit margin of 30.66% during the past 5 years. They have also been able to maintain positive cash flows from their operation, netting $37 million in 2018 compared to $147 million in 2017.

Turnarounds don’t happen often, but they do occur. However, it’s unlikely under the current management. It was difficult to listen to the company’s 2018 earnings call. Understandably, management has been working hard to deal with a tough financial situation. They have implemented very difficult cost reduction initiatives with no end in sight. These initiatives include:

- Reduced store base by approximately 135,000 square feet in 2018, closing and downsizing stores, including locations where another store is not available to customers,

- Employee layoffs at the corporate and store level,

- Fewer full-time employees to allow stores to staff up or down.

While these initiatives are taking place, somebody must keep an eye on the company’s future. Barnes & Noble is currently under pressure from their largest competitor Amazon and mom-and-pop bookstores that are offering a superior customer experience.

Stop thinking like a bookstore!

In order to effectively compete, the company needs to adhere to a few principals. First, the company must focus on providing a unique customer experience coupled with superior and original content to be successful in the current marketplace. In today’s world, high service becomes standard.

The company operates in two segments: B&N Retail and NOOK. Management has redesigned stores to reduce their footprint and adapt to consumer demand. However, their strategy has failed to leverage their stores to increase their digital revenues organically. Instead, management has focused on growing their toys & games, café products, and gifts business, which is now 28% of their revenues, compared to 21% back in 2013.

The digital business should have higher margins, but Amazon’s disruption has caused the business to decrease from $780 million or 12% of revenues back in 2013, to $112 million or 3% of revenues in 2018. To be clear, Barnes & Noble has not made any profits from this segment, but that must also change if the company will have a future. Consider retailers across the spectrum from Wal-Mart (NYSE:WMT) to Home Depot (NYSE:HD) who, despite encroachment from Amazon, have found ways to effectively engage with customers online. As such, they must invest heavily in R&D to improve the Nook experience (or a new platform) and take their e-commerce to the next level.

Additionally, the company fails to compete with Amazon.com Inc (NASDAQ:AMZN) with the one asset they have, their stores. Customer experiences provide additional touchpoints to engage with the customer and provide value-added services. Though it’s fallen by the wayside, Barnes & Noble used to be a place for book clubs, author speaking engagements, and more. Consider the size of the education market should they engage those customers. To compete with its much smaller competitors, the company should take a page from Sun Tzu's The Art of War, “To know your enemy you must become your enemy.” Barnes & Noble must offer a superior customer experience and crush their much smaller adversaries with their scale.

Conclusion

Books will never be out of style. The feel and smell of a book in your hands has no equivalent experience. But Barnes & Noble needs management that does not view their business as just a bookstore. Although the company has experienced turnover at the CEO position, and in their current situation, when it is difficult to attract top talent, a fresh new way of looking at their business must be thrown into the mix. The company will be best served to take a page out of Netflix (NASDAQ:NFLX) and invest in content, before becoming the next Borders. Netflix currently generates revenues at approximately three times on their original content spend.