Wall Street continued to feel the heat of rising yields, but sentiment improved during the Asian session today, perhaps after China cut its mortgage reference rate. In the FX world, the Aussie was the leading gainer due to Australia’s better-than-expected jobs report. At the same time, the Kiwi finished last, maybe due to remarks by New Zealand PM Ardern, who said that restrictions would be tightened if there is community transmission of the Omicron coronavirus strain.

Better Jobs Data Support the Aussie, Kiwi Falls on PM Comments

The US dollar traded mixed against the other major currencies on Wednesday and during the Asian session Thursday. It lost ground versus AUD, EUR, and GBP, while eked out gains against NZD and JPY. The greenback traded nearly unchanged against CHF and CAD.

The weakening of the yen, combined with the strengthening of the Aussie, suggests that markets may have traded in a risk-on fashion yesterday and today in Asia. However, the weakening of the Kiwi points otherwise.

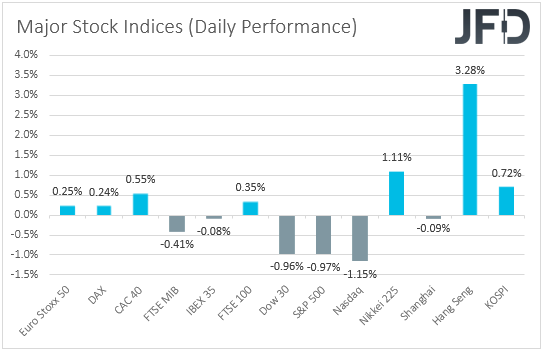

Therefore, to get a clearer picture regarding the broader market sentiment, we prefer to turn our gaze to the equity world. There, we see that European equity indices traded mixed. Still, Wall Street continued to tumble on expectations that the Fed may eventually need to tighten monetary policy faster than previously thought.

That said, market appetite improved during the Asian session today, perhaps after China cut its mortgage reference rate for the first time in nearly two years, a move that followed a surprise cut to the rate for one-year medium-term loans on Monday.

Although the improvement in market sentiment during the Asian session may have been one of the reasons behind the recovery in the Aussie, we believe that the main one was the outcome of the Australian employment report for December.

The unemployment rate declined to 4.2% from 4.6%, beating estimates of a downtick to 4.5%. At the same time, the net change in employment showed that the economy gained fewer jobs than in November, but more than the forecast suggested.

This may have allowed market participants to maintain bets over several rate hikes by the RBA this year, despite the bank signaling that it will not hit the lift-off button in 2022. We believe that the Aussie could stay supported for a while more, at least against currencies the central banks of which are expected to proceed with a more cautious strategy than the one investors anticipate for the RBA.

One example may be the euro and the ECB. Having said all that, though, it is worth mentioning that the survey for the employment report was conducted before the outbreak of the Omicron coronavirus variant. Thus, there is a chance of getting weaker numbers for January. With that in mind, we are reluctant to call for a long-lasting recovery in the Aussie, even against the euro.

In contrast with the Aussie, the Kiwi was the main loser among the majors, despite improved market sentiment during the Asian session and the RBNZ hiking rates twice already. The reason may have been remarks by New Zealand PM Ardern, who said that restrictions would be tightened if there was community transmission of the Omicron coronavirus strain.

In our view, Kiwi traders may have thought that this could slow down future rate hikes by the RBNZ, especially if this bank has done so twice before any other major central bank has even done it for the first time. BoE hiked in December, but this was after the RBNZ’s second increase, which happened in November.

Elsewhere, the Canadian dollar was found nearly unchanged against its US counterpart, but that doesn’t change our view, especially after the acceleration in the Canadian CPIs yesterday. Both the headline and core rates beat estimates, which adds credence to the view that the BoC could also increase interest rates at its upcoming gathering.

We still believe that expectations on that front, combined with rising oil prices, could keep the Loonie supported for a while more.

S&P 500 – Technical View

The S&P 500 cash index traded south yesterday after it hit resistance slightly below the 4616 barrier, near the upside support line drawn from the low of Dec. 3. That said, the slide was stopped near the 4530 barrier, marked by the low of Dec. 20, and then the rate rebounded somewhat. Overall though, as long as the cash index stays below that line, we will consider the short-term outlook to be negative for now.

Even if the rebound continues for a while more, we see decent chances for the bears to jump back into the action from near the aforementioned upside line. This could result in another test near the 4530 zone, the break of which could extend the fall towards the 4493 barrier, marked by the low of Dec. 3. A failure of that zone to provide support could pave the way towards the low of Oct. 18, at 4443.

On the upside, the outlook could become brighter again upon a break above 4670, a zone that stopped the index from moving higher between January 14th and 18th. The S&P will already be above the pre-discussed upside line, and it could initially rise towards the 4745 barrier, marked by the peaks of Jan. 12 and 13, or slightly higher, near the 4258 and 4773 areas.

If none of those levels proves to be an obstacle, then we could see the advance extending towards the 4807 territory, marked by the highs of Dec. 28, 29, and 30.

EUR/AUD – Technical View

EUR/AUD has been in a sliding mode since Jan. 18, when it hit resistance at 1.5870. That said, the slide was stopped near the 1.5690 barrier, marked by the low of Jan. 13, after it hit support slightly below that area. Overall, their price structure does not point to a clear trending structure, but another attempt below 1.5690 may be the catalyst for some further declines.

Such a dip could pave the way towards the 1.5565 territory, which supported Dec. 30 and Jan. 5. That said, if the bears are not willing to stop there, a break lower may carry more bearish implications, perhaps setting the stage for declines towards the low of Nov. 22, at 1.5490, or the low of Nov. 16, at 1.5445.

To start examining the bullish case, we would like to see a clear recovery above the 1.5905 zone, defined as resistance by the highs of Dec. 14 and 20. This will confirm a forthcoming higher high and may see scope for advances towards the high of Dec. 7, at 1.6027. If the bulls are not willing to stop there either, then we could see them climbing towards the 1.6165 territory, near the high of Dec. 3.

Today’s Events

During the European session, we get Eurozone’s final CPIs for December, which is expected to confirm their preliminary estimates, as well as the minutes, from the latest ECB gathering. At that meeting, the ECB announced ending the pandemic emergency purchase program (PEPP) in March.

However, they decided to extend the program’s reinvestment horizon and compensate by doubling the monthly pace of the asset purchase program (APP) for the second quarter. In our view, this revealed a willingness to stay accommodative for a while longer, and we expect the minutes to confirm just that.

That said, we don’t expect a significant tumble by the euro. After all, ECB President Christine Lagarde said several times that they are unlikely to hit the hike button this year, with Chief Economist Philip Lane hinting last week that this may be the case by saying that they don’t see inflation above 2% in the medium term.

Thus, although inflation accelerated to 5% in December, we believe that if the minutes confirm the view of no hikes this year, it will not come as a surprise. From the US, we get the existing home sales for December and the EIA report on crude oil inventories for last week.