The Aussie fell sharply yesterday, despite the Reserve Bank of Australia (RBA) appearing more hawkish than previously. This was due to the market being hawkish heading into the decision, and thus, anything less than what was priced in was going to be a disappointment.

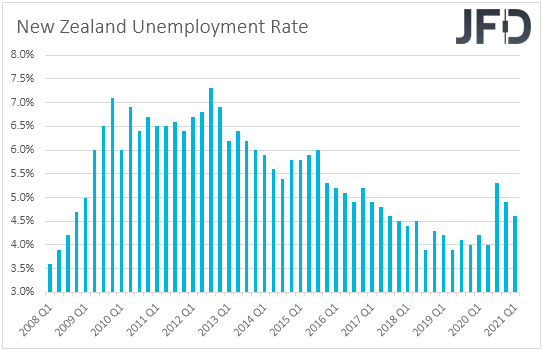

Today, we have New Zealand's employment report for Q3, where decent numbers could add credence to the RBNZ's view for more rate hikes in the months to come.

RBA Fails to Match Market Expectations, NZ Jobs Data on the Agenda

The US dollar traded mixed against the other major currencies on Monday and during the Asian session Tuesday. It lost ground against CHF, JPY, and the EUR while it gained versus AUD and GBP. The greenback was found relatively unchanged against NZD and CAD.

The fact that the prominent gainers were the traditional safe havens yen and franc, combined with the fact that none of the risk-linked currencies managed to record any gains, suggests that markets may have traded in a risk-off environment.

However, looking at the performance in the equity world, we see that this was not the case, at least not during the EU and US sessions. Major EU and US indices were a sea of green, with all three of Wall Street's major averages hitting fresh record highs. However, market sentiment indeed softened during the Asian session today, with only South Korea's KOSPI recording gains.

In our view, market sentiment continues to be relatively supported by signs that the latest supply shortages around the globe may not have affected the economic activity as many may have believed. That said, we expect more cautious trading today and tomorrow, as investors will be biting their nails in anticipation of the FOMC decision.

The financial community broadly expects the committee to announce the beginning of its tapering process, with a pace of $20 billion per month. So, suppose officials indeed decide to proceed with the expected move.

In that case, all the attention may fall on the accompanying statement and Chair Powell's conference for inflation comments and any potential hints on interest rates. According to the Fed funds futures, market participants believe that policymakers will hit the hike button at some point in the middle of next year, so anything pointing to a later timing may come as a disappointment.

Now, speaking about central bank decisions, we already had one today from the RBA. The bank maintained its core policies – rates and QE – unchanged but decided to discontinue the ten bps April 2024 yield target, which was evident after they failed to defend that level last week.

They also abandoned the forward guidance that interest rates are most likely to stay unchanged until 2024 and suggested this could happen in 2023. They said,

“The Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 percent target range. The central forecast is being for underlying inflation to be no higher than 2½ percent at the end of 2023.”

At the press conference following the decision, Governor Lowe confirmed the view, clearly saying that it is now plausible for a rate hike to be appropriate in 2023, but that doesn't make it sure that the central bank will raise interest rates before 2024.

He also added that the latest data and forecasts do not warrant an increase in the cash rate in 2022.

Remember that coming into the meeting, the financial world has been anticipating interest rates to hit 1.25% by the end of next year. So, although the RBA's guidance was more hawkish than previously, it was still well behind expectations.

In our view, that's why the Aussie has fallen sharply after the announcement. Yesterday, we noted that market pricing appeared very aggressive, which put the bar for disappointment very low.

According to the ASX interbank cash rate futures yield curve, market participants still expect some hikes next year, with the December yield now standing at 1.00%. In our view, this suggests that there is ample room for more downside in the Aussie.

Suppose central bank commentary and upcoming data confirm the belief that no hikes are appropriate next year. In that case, those expectations could continue being pushed back, something that could result in more AUD selling.

With the Reserve Bank of New Zealand (RBNZ) being among the most hawkish major central banks, we would expect AUD/NZD to continue underperforming. Remember that the RBNZ has already pushed the hike button and hinted that more hikes might be in the works for the months to come.

So, the two risk-linked currencies will offset any response to developments surrounding the broader market sentiment, and the main driver may be monetary policy divergence.

Tonight, we get New Zealand's employment report for Q3, and decent numbers could strengthen the case for more hikes by the RBNZ soon, thereby increasing the buying interest for the Kiwi.

AUD/USD – Technical Outlook

AUD/USD fell sharply on Monday, following the RBA decision, breaking below the upside support line drawn from the low of Sept. 29. In our view, this has discarded the bullish case, but it has yet to confirm a bearish reversal signal. Therefore, we will stay sidelined for now.

For us, a bearish reversal signal will be an apparent dip below 0.7440, support marked by the high of Oct. 15. This will confirm a forthcoming lower low on the 4-hour chart and may initially pave the way towards the low of Oct. 18, at 0.7380.

If the bears are unwilling to stop there, a lower break could allow extensions towards the low of Oct. 13, at around 0.7330. Below that lies another potential support zone, at about 0.7290, from where the buyers jumped back into the action on Oct. 8 and 11.

Now, to start examining the resumption of the prior uptrend, we would like to see a rebound back above 0.7555. This will confirm a forthcoming higher high on the daily chart and may see scope for extension towards the 0.7600 zone, marked by the high of July 6, the break of which could pave the way towards the inside swing low of June 3, near the 0.7650 area.

AUD/NZD – Technical Outlook

AUD/NZD also tumbled after the RBA policy decision and is now hovering slightly above the 1.0415/24 critical support zone, marked by the lows of Oct. 21 and 19 respectively.

Although the overnight slide suggests that the corrective wave between Oct. 21 and 29 is over, we prefer to wait for a dip below the critical support zone of 1.0415/24 before we get confident in more significant declines.

Such a move will confirm a forthcoming lower low on the 4-hour and daily charts and may pave the way towards the 1.0382 area, marked by the inside swing high of Sept. 10.

A lower break could see scope for extensions towards the key barrier of 1.0355, which provided resistance between Sept. 20 and 23, where another break could set the stage for the low of Sept. 24, at 1.0315.

We will start assessing whether the bulls have gained the upper hand only if we see a break above the high of Oct. 29, at 1.0528. Such a move will confirm a forthcoming higher high and may initially target the 1.0565 barrier, marked by the inside swing low of Oct. 13, the break of which could open the path towards the peak of the day before, at around 1.0612.

As for the Rest of Today's Events

We already got Switzerland's CPI, but as is the case most of the time, the franc barely responded to this report. In a while, we get Eurozone's final manufacturing PMI for October, which is once again expected to confirm its preliminary estimate.

With regards to the energy market, we have the API weekly report on crude oil inventories, for which no forecast is available. As for the speakers, we will get to hear from the ECB Supervisory Board Chair Andrea Enria.