We have an exciting week ahead, with two central bank decisions on the agenda: the Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ). While we expect The RBA to take no action, the RBNZ is expected to lift rates for the first time since the coronavirus pandemic.

Today, ahead of those decisions, the OPEC+ group meets to decide on oil output, while on Friday, we get the US employment report for September. Elsewhere, Chinese and South Korean Markets stay closed due to holidays, while no major indicators are scheduled on the calendar for the rest of the day.

Therefore, at first glance, it appears to be a quiet day for the markets. But, we have a meeting between OPEC and its allies to debate if they are to boost oil production or not.

In July, the OPEC+ group agreed to increase production by 400,000 barrels per day every month at least until April 2022, in a process to phase out 5.8 million barrel per day of existing cuts.

Lately, oil prices soared to a three-year high, driven by supply disruptions and recovering demand from the coronavirus pandemic, as well as due to gas supply shortages.

Last week, four sources told Reuters that the group was considering adding more, but there were no details on how much more or when any supply increases could occur.

Therefore, with that in mind, although October’s volumes are already decided, any decision pointing to more increases in the next few months may result in a decent downside correction in oil prices.

On the other hand, maintaining the existing deal and providing no clues as to whether a decision to increase output could be looming at one of the upcoming meetings could add further fuel to the fuel’s latest uptrend.

On Tuesday, during the Asian session, the RBA meets to decide interest rates. In September, the bank planned to taper purchases from AUD 5 billion to AUD 4 billion per week during the last meeting.

Still, it delayed the date for a new review from November 2021 to February 2022 due to a delay in the economic recovery and increased uncertainty associated with the outbreak of the Delta variant.

As for interest rates, officials stuck to their guns that they are likely to keep them at present levels until 2024.

So, taking the prior decision into account, we don’t expect any policy changes this week. However, with daily COVID infections staying near records and keeping in mind the economic slowdown in China, we will be keen to find out if the statement turns out to be more dovish than expected.

Any fresh concerns over the nation’s economic recovery could raise speculation that at some point soon, the bank may delay the timing of its subsequent tapering, thereby adding pressure to the Australian dollar..

With increasing expectations of a November tapering move by the Fed, the Aussie could resume its recent downtrend against its US counterpart.

Elsewhere in Asia, Chinese markets will stay closed until Thursday in celebration of National Day.

From New Zealand, we get the NZIER business confidence index for Q3, while from Japan, we have the Tokyo CPIs for September. Australia’s trade balance for August is also coming out.

Later in the day, we have the final composite and services PMIs from the Eurozone, the UK, and the US, but as it is always the case, they are expected to confirm their preliminary estimates.

The ISM non-manufacturing index for the month is also due. It is expected to have declined to 60.0 from 61.7. From Canada, we have the nation’s trade balance for August.

On Wednesday, the attention will shift to the RBNZ. During the previous meeting, the bank delayed raising interest rates when the financial community was more than confident of a hike.

Policymakers changed their minds after the nation entered a lockdown due to new coronavirus cases. However, they signaled that they still expect to push the hike button before year-end.

Market participants are betting that such a move could occur during this meeting but only anticipate a 25bps rate increase. Any expectations over a double hike may have diminished recently as covid infections have spiked again, suggesting that a full economic reopening is still away.

Therefore, with a quarter-point hike fully priced in, we don’t expect any Kiwi reaction on that. We believe that any move is likely to be triggered by the language in the accompanying statement.

Anything suggesting a more cautious hike path could push the Kiwi lower. For the currency to strengthen, we need to see optimistic remarks pointing to faster hikes, a case we see as unlikely for now.

Therefore, we would consider the risks surrounding the Kiwi’s reaction to the meeting as tilted to the downside with all that in mind.

Later in the day, we have Eurozone’s retail sales for August and the US ADP report for September. Eurozone’s retail sales are expected to have rebounded 0.8% mom after sliding 2.3%, while in the US, the ADP report is expected to show that the private sector has gained 430,000 jobs, less than August’s 374,000.

Although the ADP is far from a reliable predictor of the NFPs, it is the only primary gauge for the official statistic. Thus, it could raise speculation that the NFPs could also come in slightly better than in August.

Thursday is a quiet day regarding economic releases and data, with the only event worth mentioning being the minutes from the latest European Central Bank (ECB) monetary policy meeting.

At that meeting, the bank announced a “moderately lower pace” of PEPP purchases for the next quarter, but President Lagarde made it clear that this was not a tapering move and that when PEPP is over, they have all other tools available.

This may hint that when PEPP is over, conditional upon the economic outlook, they could compensate by buying more through other schemes, like the Asset Purchase Program (APP). So, with that in mind, we will scan the minutes to see whether this is the case.

Clearer hints that the bank stands ready to offset the end of the PEPP by buying more through other programs could encourage more euro selling.

Finally, on Friday, the main item on the agenda may be the official US employment report for September. Nonfarm payrolls are expected to increase to 470,000 from 243,000. The unemployment rate is expected to tick down to 5.1% from 5.2%.

Average hourly earnings are forecast to slow to +0.4% mom from +0.6%. Barring any deviations to the prior monthly prints, this is anticipated to take the YoY rate up to +4.6% from +4.3%.

Overall, all this points to a more decent report than the one we got for August. This, combined with Powell’s recent remarks that inflation remains elevated for longer than they have estimated, may encourage market participants to add to bets over a November tapering by the Fed and the timing of the first interest rate hike.

Something like that could translate into further strength in the US dollar and a deeper correction in equities. The opposite could be true if we get a disappointing set of numbers.

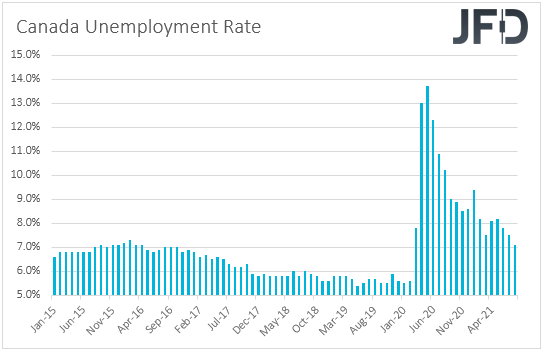

At the same time, with the US employment report, we also get jobs data for September from Canada. The unemployment rate is expected to slide to 6.9% from 7.1%. The net change in employment is forecast to show an uptick of 60,000 jobs during the month, after adding 90,000 in the prior month.

At its prior gathering, the Bank of Canada (BoC) kept its policy untouched and maintained the guidance that the economic slack would be absorbed sometime in H2, 2022, which means this is when they expect to start raising interest rates.

Following the economic contraction in Q2, many participants may have been expecting the bank to announce a delay in its tapering plans. However, that was not the case. Even Governor Tiff Macklem said that he and his colleagues are moving closer to a time when continuing to add stimulus through QE won’t be necessary.

Therefore, another round of decent employment numbers could add to the October tapering case and could somewhat support the Loonie. However, the currency could also be well affected by today’s decision on oil output by OPEC its allies.