Airbnb Inc (NASDAQ:ABNB) market debut was stunning and more than met the goals the company set for itself in its last amendments to its IPO before listing. High as the company’s valuation seemed, which gave an IPO price range of $56 to $60 and valued the company at $34.6 billion, it was well within the cash-making ability of the company to justify that price level. The company is on track to achieve the cash flow expectations implied by the prospectus price.

The last amendments were within the realm of reason but left very little room for error on the part of management and increased the pressure to deliver.

Just to show how far from reality the present valuation has gotten, the IPO indicated price top implied that:

- ABNB would improve its NOPAT margin to 9% over four years, as opposed to the 8% it enjoyed in 2019 and -16% over the trailing twelve-month period.

Improve revenue by 36% CAGR over the next five years, a rise from 30% CAGR.

Fatten its gross booking value from

At the IPO price, the business was already unattractive because the price left no alpha for investors. At present valuations, not only is there no alpha left for investors, but, the assumptions inherent in the price are beyond what is possible within a reasonable set of circumstances, Covid-19 or no Covid-19. Pricing aside, the business model is very good.

ABNB’s economics and business model show a company that has a route to growth with profitability, especially if the company can

- Keep its lower cost structure down in order to improve margins.

Use its dense logistics network to meet booming consumer demand for flexible lodging.

Build competitive advantages for that the business can grow with as little cost as possible.

The company acts as a matchmaker, or multi-sided platform, with an eye toward creating network effects that will drive winner-take-all markets.

The company’s momentum-driven flywheel is the core of its business model. The company is consciously creating a momentum-driven flywheel model that will ensure that the marginal user of ABNB will bring new value to the network and make it more attractive to other users of the product.

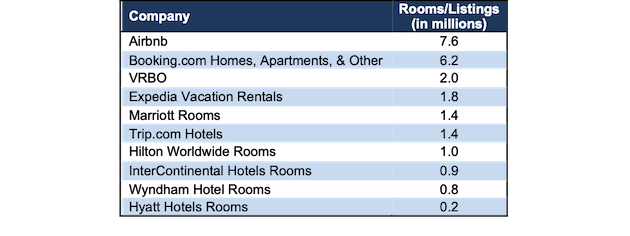

As the chart below by New Constructs indicates, the company has grown to have the largest number of rooms in the accommodation business in the world.

The company’s platform of property owners and room listings is creating network effects that should create economies of scale and allow the company to enter into profitability. The model is designed such that the more marginal users enter the market, the more hosts are attracted to the site in search of guests and this coming to market of suppliers gives hosts a greater number of possibilities and opportunities. This is the network effect through which success breeds success.

ABNB has the largest platform for new listings, alongside a size advantage which even traditional hotel room providers cannot match. The company is very close to achieving economies of scale which will give it pricing power.

Covid-19 has dented the business but this may only be temporary. As the nature of work changes and people pick places to live because of questions of quality of life rather than job opportunities, there will be a greater need for ABNB’s services, in order to help remote workers move from one part of the world to the other. Those who want to make a real estate investment have to realize that the nature of work and travel in this era frees people to live anywhere and so, certain kinds of properties will become less valuable and businesses like ABNB, which are built to take advantage of the changing nature of work and how people choose to live, will thrive.