Airbnb (ABNB), the sharing economy’s poster-child, filed its IPO prospectus with the SEC. Here we examine the vast transformational opportunity that the company has tapped into and the wide moat it has to defend its profitability, to show just what a sound investment the company is.

The Sharing Economy is Transformational

The world is in the middle of profound technological and demographic changes that have upended our old housing and lodging notions. Standardized accommodation gives way to a demand for more flexible, serviced, home-like, urban, and shared housing.

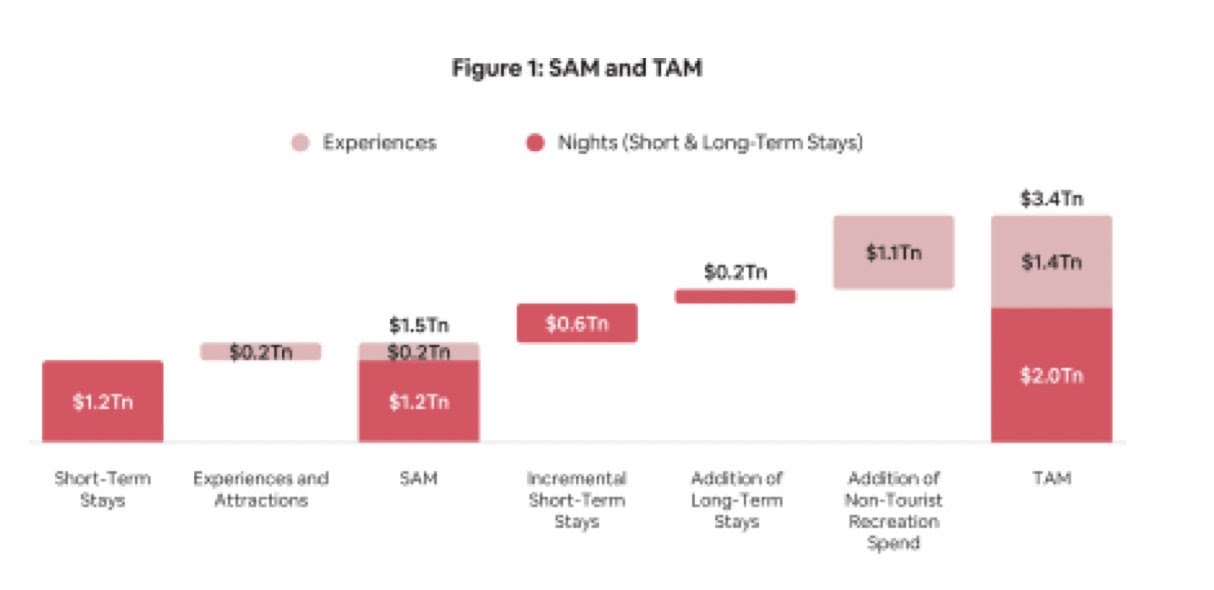

Owners of under-utilized spaces have responded to this change by offering up their property for rentals. ABNB exists to turn these profound changes to profit by offering guests and hosts a matchmaking platform connecting the two sides of this market: hosts and guests. ABNB’s estimated addressable market indicates just how big this addressable market is, as we can see from this chart from its filings:

Companies tend to exaggerate their addressable market size, but I think there are reasons to believe that ABNB’s estimates are conservative. Though Covid-19 has hit its revenues, which have fallen 30% this year, one could argue that the global pandemic has improved ABNB’s long-term prospects.

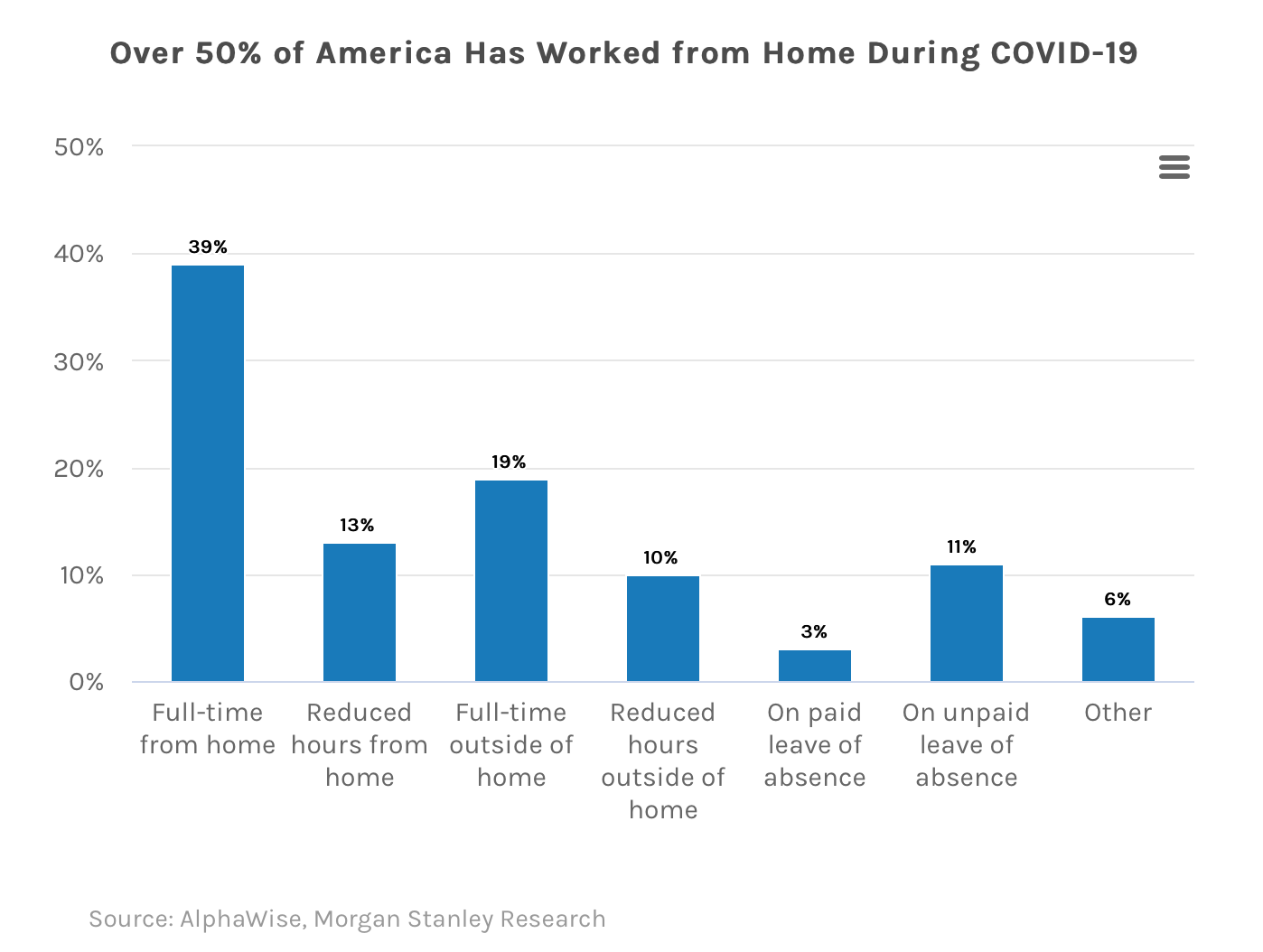

This argument is based on the shift to remote work. Facebook (NASDAQ:FB) CEO Mark Zuckerberg has said he expects 50% of Facebook’s employees to work remotely within the next 5-10 years. He is not the only CEO driving a shift to remote work.

A transition to remote work has apparent effects: it makes location unimportant in terms of volume. HBR and Morgan Stanley have shown that the share of Americans working remotely jumped from 5% pre-Covid to 50% by April 2020. Many workers will return to office work, but many will not. The chart below shows just how dramatically the nature of work has changed:

Remote work also means that the relationship of workers to big cities will change. Per Bloomberg, big cities are so expensive to live in that a person taking a pay cut to move outside a big city can still end up with more money in their pocket. The mere presence of choice will result in more people moving from big cities, enlarging ABNB’s market opportunity. According to old metrics, the company does not have to beat traditional players; ABNB wins by being good at what its users want.

Airbnb’s Moat is Unassailable

A matchmaker, or multi-sided platform, should, in theory, create network effects leading to winner-take-all markets. ABNB’s momentum-driven flywheel is the heart of its business model. Each new user of the platform adds value to the network to present users, which brings in more new users and creates formidable barriers to entry, enhancing the value of the system.

Three things drive ABNB’s value:

- the minimum viable market share,

- customer captivity,

- the degree to which the platform’s user data drives product and pricing optimization.

Minimum viable market share

ABNB’s share of US consumer lodging expenditure in 2019 was 20%, according to data from Second Measure, second only to Marriott. Local density of property inventory is a crucial driver of the business’ financial viability. Product complexity and resultant marketplace liquidity needed to be competitive are very high. Existing rivals and new entrants have to contend that rising local marginal density in listings does not saturate density; they increase the value of the network.

ABNB is mostly a variable-cost business, but fixed-cost requirements are materially essential. Between 2018 and 2019, net property and equipment were approximately $300 million each year, and operating lease right-of-use assets in 2019 were worth about $390 million. Potential rivals will have to recreate this to compete in a market in which market share does not move aggressively, which would lead to a long period of losses while trying to match ABNB. Consequently, direct competitors have tended to be acquired by international travel companies. Homeaway, for example, which has half of ABNB’s listings, was acquired by Expedia (NASDAQ:EXPE), and FlipKey, which has a third of ABNB’s listings, was bought by TripAdvisor (NASDAQ:TRIP).

Customer captivity

Customer captivity is high. In highlighting the possibility that a materially significant share of ABNB’s revenue is from properties dedicated to it, the French Hotel Federation president called ABNB “an underground shadow economy.”

The usual argument is that competitors are a click away, but people are loath to move from platform to platform when seeking guests or hosts. This is an economy where trust is essential. Also, the reviews system keeps people accountable it also creates incentives to stay within the ecosystem to build credit. There is, for example, a difference between one 4-star rating and 1000 5-star ratings. Indeed, one might prefer 1000 4-star ratings to one 5-star rating.

Data

User-generated data enhances the value of this network because it tells ABNB what our travel plans are, what the budget is like, etc., allowing it to continue to improve pricing and products and this nuanced perspective is something money cannot buy; it is a consequence of long relationships with many users.

Conclusion

Networks, such as ABNB, or Geodb, a decentralized peer-to-peer big data-sharing ecosystem are becoming critical to the world we are making. ABNB is at the vanguard of this revolution and is poised to earn increasing market share, defend its economic profits, and help grow the addressable market into something even more significant. The business is a sound investment proposition.