We issued an updated research report on Danaher Corporation (NYSE:DHR) on Nov 18.

The company, with a market capitalization of $102.7 billion, currently carries a Zacks Rank #3 (Hold).

Many tailwinds and headwinds are impacting its performance. Let’s delve deeper.

Factors Favoring Danaher

Solid Product Portfolio: The conglomerate is engaged in designing, manufacturing and marketing of diverse lines of professional, medical, industrial, commercial and consumer products. Solid demand for its products, mainly in developed and high-growth markets, favorably impacted the third-quarter 2019 results.

In the quarters ahead, solid product demand (including DxH 900 analyzer, Esko, X-Rite, ChemTreat and others) will likely bolster Danaher's segmental sales. For the fourth quarter of 2019, the company predicts year-over-year core sales growth of 4.5%.

Shareholder-Friendly Policies: Danaher remains committed to rewarding shareholders handsomely through dividend payments. During the first nine months of 2019, it distributed dividends worth $385 million, up from $321.2 million distributed in the year-ago period.

Notably, the company hiked its quarterly dividend payout by 6% in March 2019.

Inorganic Actions: Danaher has been strengthening the portfolio through acquisitions and divestments. In April 2018, it acquired Integrated DNA Technologies and added Blue Software to its portfolio in July 2018. In January 2019, Danaher enhanced automation capabilities with the acquisition of Labcyte Corporation.

In addition, the company is working toward acquiring General Electric Company's (NYSE:GE) BioPharma business. Danaher anticipates earnings accretion of 45-50 cents per share from the buyout in the first year of the completion of the deal (in the first quarter of 2020). Also, Danaher divested its dental business to an independent publicly-trading company, Envista Holdings Corporation (NVST), in September 2019. The move is expected to work in the best interest of Danaher’s shareholders.

Danaher holds Envista’s 80.6% stake, which it is planning to dispose of.

Factors Working Against Danaher

Share Price Performance and Over-Valued Stock: Market sentiments seem to be working against the stock, as evident from Danaher’s shares’ underperformance compared with the industry. In the past three months, the company’s shares have gained 0.1% compared with the industry’s growth of 12.2%.

Also, its shares currently seem overvalued compared with the industry, using the P/E (TTM) valuation method. The stock’s three-month P/E multiple is 29.84x, higher than the industry’s 21.8x. Also, the stock is currently trading higher than the industry’s three-month multiple of 21.8x. This makes us cautious about the stock.

Costs and Forex Woes: Rising costs and expenses have been dragging Danaher for quite some time now. In the first three quarters of 2019, the company’s costs of sales increased 4.6% year over year, while selling, general and administrative expenses grew 4.4%. Also, research and development expenses expanded 4.4%.

Further, international diversity has exposed the company to geopolitical issues and unfavorable movements in foreign currencies. In the third quarter of 2019, forex woes adversely impacted its sales growth by 1.5%. Debts and stocks issued to fund the acquisition of the BioPharma business are added concerns for Danaher.

Persistence of such issues might be concerning for the company.

Weak Earnings Projections: Danaher has lowered earnings projections for 2019 due to dilution caused by the Envista transaction. It now anticipates adjusted earnings per share of $4.74-$4.77 compared with previously mentioned $4.75-$4.80.

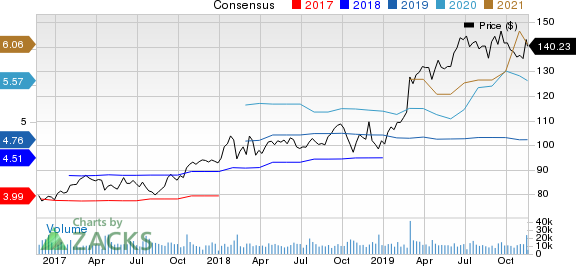

In addition, the Zacks Consensus Estimate for the company has been lowered in the past 30 days. Currently, the consensus estimate for earnings is pegged at $4.76 for 2019 and $5.63 for 2020, reflecting declines of 0.4% and 1.6% from the respective 30-day-ago figures.

Danaher Corporation Price and Consensus

Danaher Corporation price-consensus-chart | Danaher Corporation Quote

Stocks to Consider

Two better-ranked stocks in the industry are Bunzl (LON:BNZL) plc (OTC:BZLFY) and Macquarie Infrastructure Company (NYSE:MIC) . Both companies currently carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

In the past 60 days, earnings estimates for Bunzl improved for the current year, while remained unchanged for Macquarie Infrastructure.

Biggest Tech Breakthrough in a Generation

Be among the early investors in the new type of device that experts say could impact society as much as the discovery of electricity. Current technology will soon be outdated and replaced by these new devices. In the process, it’s expected to create 22 million jobs and generate $12.3 trillion in activity.

A select few stocks could skyrocket the most as rollout accelerates for this new tech. Early investors could see gains similar to buying Microsoft (NASDAQ:MSFT) in the 1990s. Zacks’ just-released special report reveals 8 stocks to watch. The report is only available for a limited time.

See 8 breakthrough stocks now>>

Bunzl PLC (BZLFY): Free Stock Analysis Report

Danaher Corporation (DHR): Free Stock Analysis Report

General Electric Company (GE): Free Stock Analysis Report

Macquarie Infrastructure Company (MIC): Free Stock Analysis Report

Original post

Zacks Investment Research