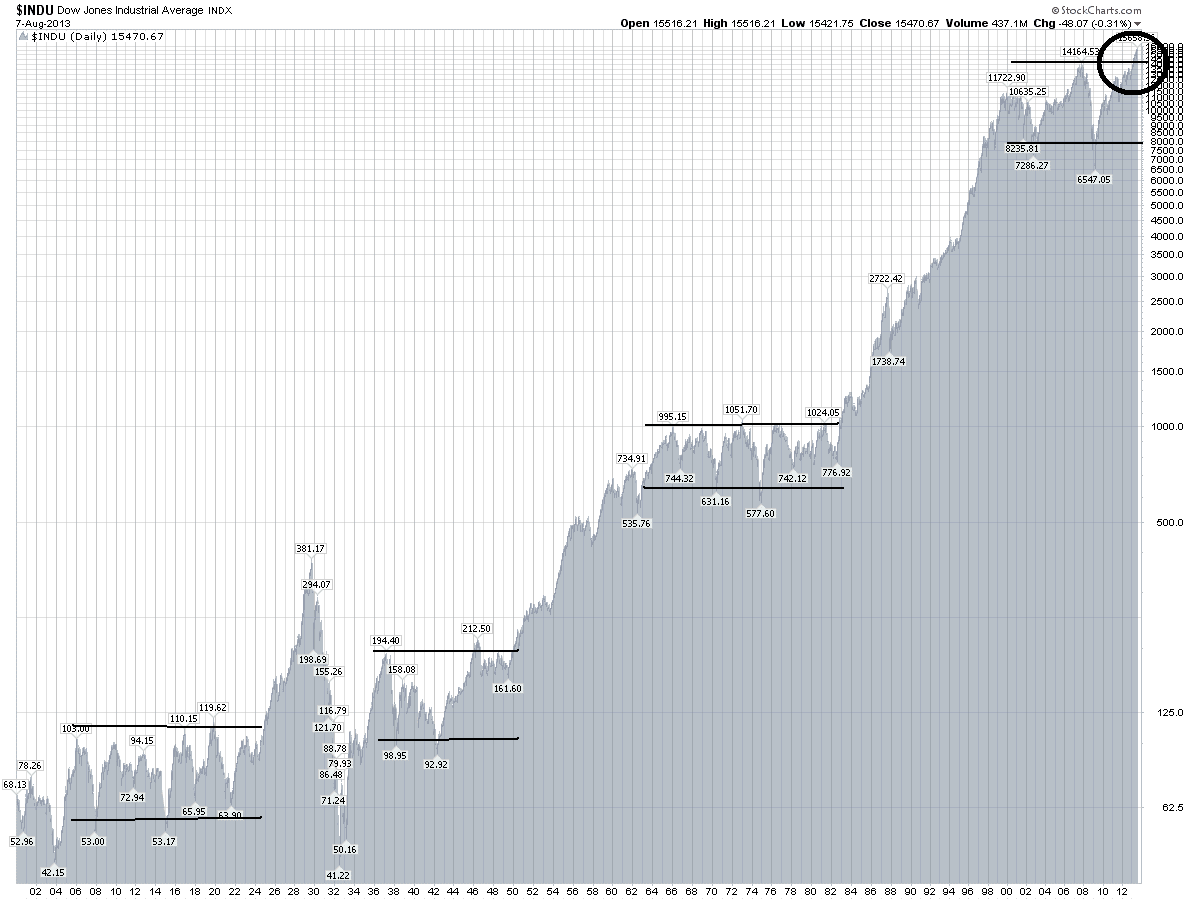

As the chart below shows, the Dow Jones Industrial Average, along with other the major US averages, have decisively made new all-time highs and broken out of their trading ranges. Can we therefore expect the launch of a new secular bull market for stocks?

Dow Jones Industrials Average from 1910

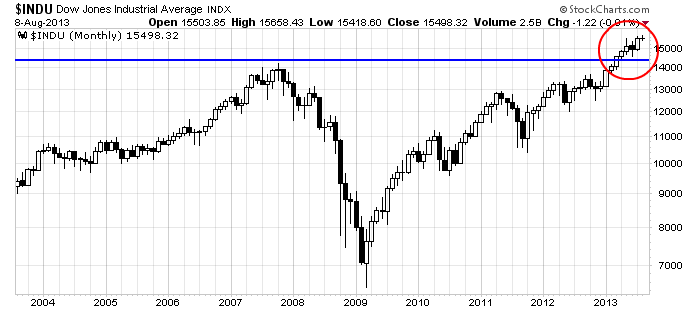

Zooming in, here is the 10-year monthly chart of the Dow. The upside breakout is clear on that chart as well.

Despite the technical evidence, I believe that the odds that this is the start of a secular bull market are low for three reasons. All of these are signals that valuations are elevated, which is what matters in the long-term.

First, private equity firms like Fortress and Blackstone are seeking to sell their equity positions, according to this Bloomberg report:

Private-equity managers from Fortress Investment Group LLC (FIG) to Blackstone Group LP (BX), which made billions by buying low and selling high, say now is the time to exit investments as stocks rally and interest rates start to rise...

“It’s almost biblical: there is a time to reap and there’s a time to sow,” Apollo’s Black said at a conference in April. “We think it’s a fabulous environment to be selling. We’re selling everything that’s not nailed down in our portfolio.”

Black’s New York-based firm, which oversees assets worth $114 billion, generated $14 billion in proceeds from the sale of holdings between the first quarter of 2012 and the first quarter this year.

Where they can't exit their positions, private equity firms appear to be intent on extracting as much value as they can from issuing debt, according to this WSJ report. It seems that this class of investors just can't find good values in the market [emphasis added]:

The industry’s focus on exits has reduced volumes of leveraged buyouts this year, with the number of private-equity deals announced declining 20 percent to 3,047 worldwide from the same period last year, according to data compiled by Bloomberg.

“It’s a difficult environment to find really attractive things when the markets are robust as they are,” Fortress’s Edens said yesterday.

That seems to be the position taken by patient value fund managers, according to this other Bloomberg report [emphasis added]:

The $1.1 billion Weitz Value and $980 million Weitz Partners Value funds each have cash stakes that are close to 30 percent. At the $10.6 billion Yacktman Focused fund, cash has crept up from 14 percent a year ago to 19 percent. The $1.3 billion Westwood Income Opportunity has about 16 percent in cash, more than double what it had at the start of the year. Cash makes up about 28 percent of assets in the $8.9 billion IVA Worldwide Fund, up from 10 percent a year ago, and is 33 percent of the $508 million GoodHaven fund, up from 19 percent a year ago.

Those are some seriously contrarian positions. The average diversified U.S. stock fund has less than 5 percent in cash, according to Morningstar. For funds such as IVA Worldwide that fall into the "world allocation" fund category and invest globally across a wide range of asset classes, the average cash stake is below 15 percent.

There’s no big macroeconomic prediction fueling the move of these value managers into cash. Just some simple investing discipline as managers pare positions in stocks they bought at deeply depressed prices. The Leuthold Group reports that the median price-earnings ratio for large-cap value stocks is 13 percent to 25 percent above its long-term historic norm; large-cap growth stocks trade at an 8 percent to 10 percent discount to their historic norm.

“After taking profits on stocks that have risen close to what we believe is their value, we aren’t finding enough mispriced securities to redeploy that cash into,” says IVA Worldwide co-manager Charles de Vaulx. He'd rather know with certainty that he'll lose a little by holding cash “than stay invested in stocks I don’t think offer enough value and lose a lot.”

In addition, the median appreciation potential of stocks tracked by Value Line is flashing a danger signal:

While not intended to be a market-prediction tool, it has worked nicely as one, especially for investors with a time horizon of a few years. Academic studies have ratified its value in this regard. The market-newsletter tracker Hulbert Financial Digest has ranked it first among market-timing services in forecasting four-year market performance.

Since 1970, the VLMAP, as it is known, has flagged the tremendous buying opportunities at the bear-market lows in 1974, 1982 and 2009, each time suggesting the median return potential was an annualized 25% or more over the next five years. That’s almost exactly how the Standard and Poor’s 500 index has performed in the four-plus years since the March 2009 market low.

Conversely, every time the number has fallen to its current 7% level – which is in the lowest 10% of all readings since 1970 – the broad market has been flat or down over the subsequent half-decade.

The combination of VLMAP, private-equity and value managers represent long-term patient money and modeling techniques. Private equity and value managers are not day-traders or swing traders, but their ticks are in months or quarters. So when patient money tells me that stocks are expensive, I have to sit up and take notice.

To be sure, short and medium term fundamental and technical indicators are still supportive of fresh highs in the major US equity indices. Market breadth remains positive and Street consensus forward earnings continue to grow, according to Ed Yardeni, and this is bullish for equities.

Regardless, long-term investors who put money to work in the stock market today are likely to be disappointed if they were to come back and examine their positions in three to five years.

Disclosure: Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. ("Qwest"). This article is prepared by Mr. Hui as an outside business activity. As such, Qwest does not review or approve materials presented herein. The opinions and any recommendations expressed in this blog are those of the author and do not reflect the opinions or recommendations of Qwest.

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or Mr. Hui may hold or control long or short positions in the securities or instruments mentioned.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

A New Secular Bull? Don't Count On It!

Published 08/11/2013, 01:21 AM

Updated 07/09/2023, 06:31 AM

A New Secular Bull? Don't Count On It!

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.