Realising our potential: Potential output and the monetary policy framework

A speech delivered to the Wellington Chamber of Commerce

On 9 July 2014

By Dr John McDermott, Assistant Governor

Introduction

It has long been recognised that the best contribution that monetary policy can make to strong and sustainable long-run growth is low and stable inflation. This proposition is at the heart of New Zealand’s flexible inflation-targeting framework to maintain price stability while not causing excess volatility to output, interest rates or the exchange rate. When explaining our monetary policy actions we frequently speak about the performance of the economy relative to its potential. Colloquially, the growth in potential output is how fast the economy can expand without generating inflation.

Today I want to speak to you about the concept of potential output itself, rather than the more usual topic of economic growth relative to its potential. Because New Zealand's growth in potential output is not a universal constant, but is subject to frequent changes, it makes sense for the Bank to devote a significant amount of resources to estimating potential output and explaining our thinking behind those estimates.

Our estimates of potential output are regularly reviewed at every release of our Monetary Policy Statement. Our estimates can change for many reasons: data revisions can result in short term changes; capital purchases or labour market participation can result in changes over the medium term; and institutional developments can result in long-run changes. Indeed, the Reserve Bank’s estimate of potential output growth has been revised up over the past six months to a peak of 2.8 percent in 2015, from 2.5 percent previously. Today I will elaborate more on the short and medium term developments affecting potential output and, while not of immediate relevance for New Zealand monetary policy, I will touch on some longer-run issues.

What is potential output?

As noted earlier, potential output is typically considered to be the level of output achievable in an economy given the available factors of production – labour, capital and productivity – that is not associated with accelerating inflationary pressure on consumer prices. Any definition of potential output refers to an unobservable concept.[1]

Potential output could in theory be highly variable. It is undoubtedly highly uncertain and difficult to measure. Because of the difficulty in measuring potential output, we typically assume potential output evolves slowly and relatively smoothly. This assumption allows us to estimate potential output by using averages or trends of GDP data.

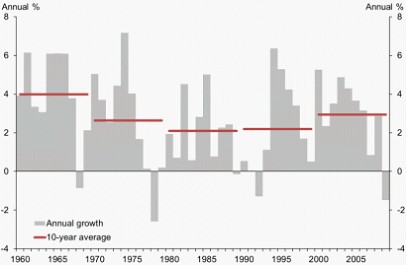

The average rate of output growth over longer periods of time can provide us with a rough gauge of the growth capacity of an economy. Figure 1 shows that observed average growth in New Zealand has varied over the past five decades, ranging from a low of 2.1 percent in the 1980s to almost 4 percent in the 1960s. Over this period there have been significant changes in New Zealand’s economic environment through societal change, government policy, and external conditions.

Figure 1: Average output growth in New Zealand

Source: Statistics New Zealand, RBNZ calculations.

The Reserve Bank focuses on demand pressures and inflation

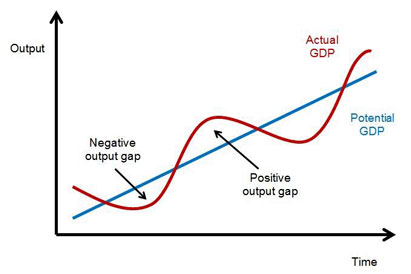

Potential output is a useful concept in framing monetary policy in an inflation-targeting system. The so-called output gap, or, how actual output fluctuates around the path of potential output over the business cycle, describes a key component of inflationary pressures and motivates a monetary policy response. Higher growth in potential output is desirable, but whatever the state of potential output, identifying the fluctuations of actual output around the path of potential output is the focus of monetary policy. Monetary policy settings are mostly about the cyclical fluctuations in the economy.

Figure 2: Stylised view of the output gap and inflation pressures

Source: RBNZ.

If we consider actual and potential output in terms of growth rather than levels, all else equal, inflationary pressure tends to rise when demand in the economy is growing faster than potential output, and tends to moderate when demand is growing slower than potential output. The Reserve Bank will typically respond by increasing interest rates in order to moderate demand pressures in the first case, and by reducing rates to stimulate demand in the second. While this may sound straightforward, policy formulation requires difficult judgements to be made in the face of considerable uncertainties, including judgements as to the size of the output gap and the path of potential output.

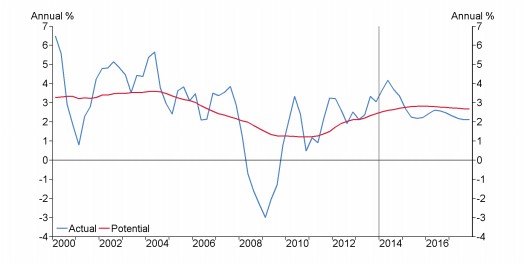

Figure 3: Growth in actual and potential output in New Zealand

Source: Statistics New Zealand, RBNZ estimates.

The notion may be straightforward; measurement is not

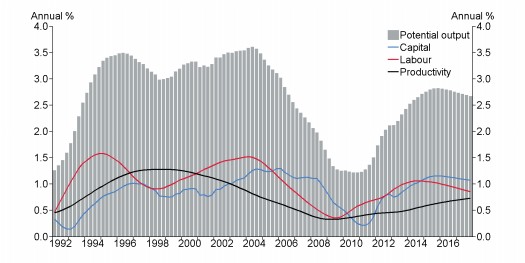

The notion of potential output is straightforward enough. But potential output is unobservable and has to be inferred from the other economic information we have available. Ultimately estimating potential output requires making a judgement about the extent to which particular fluctuations in observed output are cyclical and the extent to which they are changes in the path of potential output. The Reserve Bank expresses growth in potential output as the sum of contributions from estimates of trend growth in capital inputs, labour inputs, and productivity.

Estimating potential output in real time is challenging. Growth in potential output is not constant – its path does not in reality follow a straight line as shown in our stylised figure. Views on the level or growth in potential output, both at present and over history, can and do change. Views can differ from analyst to analyst or model to model, even based on the same data.

The Reserve Bank’s assessment of potential output has changed

The Reserve Bank has recently revised its estimates of potential output growth. The Bank expects growth in potential output in New Zealand to increase over the forecast horizon as labour and capital resources available in the economy increase. Annual growth in potential output is estimated to peak at around 2.8 percent in 2015. This demonstrates a marked improvement in growth prospects from an estimated trough in potential growth of 1.2 percent following the 2008/09 recession.

Figure 4: Components of potential output growth

Source: RBNZ estimates.

Our estimate of potential growth has increased since December, from a peak of 2.5 percent in 2015 to 2.8 percent. The increase in our estimate of potential growth is because:

- Data revisions now reveal that there has been more investment in productive capital than previously thought;

- Strong business confidence suggests that future investment could be stronger than previously thought; and

- The supply of labour is expected to be stronger than previously anticipated, due in part to increased net immigration.

Growth in actual output is expected to have peaked at around 4 percent in the year to June, driven by strong construction spending, increasing net immigration, high export prices, and low interest rates. With the economy growing at a faster rate than potential output, inflationary pressures are expected to increase. In this environment, it is important that inflation expectations remain contained and that interest rates return to a more neutral level.

Structural changes and the economic cycle cause potential growth to fluctuate

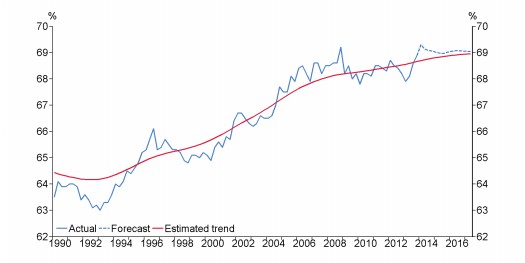

Growth in potential output fluctuates over the medium term as the availability of factors of production is influenced by the state of the economy. Let me explain this further using the example of one of the labour supply components of potential output – the labour force participation rate. Labour force participation captures the share of the total working age population (i.e. the population aged over 15) that are working or are available for work.

Labour force participation has increased over time in New Zealand as female participation in the workforce has increased, and, more recently, as older age cohorts remain in the labour force for longer. Increasing participation increases the supply of labour and increases potential output. Assumed trends amongst labour market cohorts, combined with demographic projections, suggest that a structural upward trend in the participation rate will continue in New Zealand through the remainder of this decade.

Labour force participation is also influenced by the state of the economy. Upswings in activity encourage more people to actively seek work, increasing the participation rate. Conversely, during recessions participation tends to weaken, as people leave the labour force, discouraged by lack of employment opportunities.

Figure 5: Labour force participation rate and estimated trend

(% of working age population)

Source: Statistics New Zealand, RBNZ estimates.

Similarly, growth in capital inputs can be influenced by structural factors in the economy such as population growth or changing technology, but can also move somewhat cyclically with business sentiment, access to finance, and investment intentions.

In an ideal world, we would take full account of these short to medium term influences on potential, but it is difficult to measure and interpret these movements in real time. The Reserve Bank’s use of trends in estimating potential output means these estimates capture the large permanent or persistent changes in input components, such as lasting shifts in participation, but does not capture higher-frequency movements.

‘Fundamental’ factors ultimately affect ‘long term’ prospects

There are a range of more fundamental determinants of growth that matter hugely for economic outcomes over the very long term, but their effect over shorter time horizons is difficult to detect. Typically these factors are more important for explaining differences in growth across countries rather than over time. For these reasons they are less relevant considerations for monetary policy and central banks tend to talk about them much less. To acknowledge their role in the overall growth story, let me briefly offer a couple of examples of these determinants: geography and institutions.

Economic geography can have a significant effect on long term prospects.[2] Proximity and connectedness to regional or global markets exposes domestic businesses to greater competition, aids in the transfer of technology and knowledge, and generates greater efficiencies of scale and scope. New Zealand’s small population and distance from major markets can make it difficult to capture these benefits. Our geographical location may be fixed, but the challenge posed by our isolation can change over time based on patterns of globalisation, political relationships, and technological change.

Our own history evidences the massive impact that innovation and technological advance can play in overcoming geographic isolation. The sailing of the ship Dunedin is one such example. The Dunedin transported the first refrigerated shipment of frozen sheep carcasses from New Zealand to England in 1882, vastly expanding the market for New Zealand’s meat products. In the modern era, further improvements in transport infrastructure and advances in information and communications technology, used effectively, have the ability to dramatically reduce distance to markets.

There is a vast literature on how the quality of institutions in an economy can contribute to growth prospects.[3] For example, for businesses to innovate they must be confident in their ability to generate an adequate return on their investment, and that these returns will not be expropriated. A strong education system supports the formation of ideas and fosters the capability to absorb new technology into business practices to increase productivity performance. A well-functioning legal system that enforces a clear set of property rights provides businesses the ability to capture the returns from their investment for a time. Scaling up production of successful innovations requires access to capital markets.

New Zealand has a relatively strong institutional framework by international comparison. Inflation targeting monetary policy constitutes a key piece of this institutional framework for supporting sustainable growth. Low and stable inflation aids in preserving property rights and keeps incentives clear for savers and investors. The Reserve Bank’s financial stability mandate is also important for supporting the sound and efficient functioning of financial markets. An example of this is the introduction of loan-to-value restrictions on residential mortgages in October 2013, in an effort to stabilise the housing market.

What impact can monetary policy have on potential output?

Recognising these various influences on potential output growth, one might ask what effect monetary policy can have on long term growth. The best contribution that monetary policy can make to sustainable long term growth is low and stable inflation.

There is a short term trade-off between growth and inflation. Unduly easy monetary policy settings can boost economic prosperity for a time, but such a boost is unlikely to be long lasting. Economic consensus, reflecting in part the experience of the 1970s, is that the trade-off between growth and inflation is unsustainable. Over time inflation expectations and nominal wages adjust to monetary expansion such that long-run unemployment and output are largely unchanged, but the rate of inflation is higher.

Indeed, it can be counterproductive to use monetary policy to target higher inflation in pursuit of better output growth over the longer-term. Such attempts risk unanchoring inflation expectations resulting in higher and more variable inflation. High and variable inflation can harm long term growth.[4]

High and variable inflation generates considerable uncertainty for individuals and businesses, hindering their willingness and ability to plan and contract over the long term. Businesses have differing abilities to change their prices in response to inflationary shocks. As some businesses change prices and others do not, it becomes difficult to distinguish a generalised increase in prices from a shift in relative prices when the inflation rate itself is variable.

Unexpected inflation acts as a hidden tax on financial investment for savers, yet reduces the real interest burden of debt for borrowers. This can distort saving and investment incentives and increase the inflation-risk premium embedded in interest rates.

Eventually a reaction sets in against high inflation. Past experiences suggest that reducing inflation materially usually involves a greater slowing in activity than the boost to growth enjoyed as inflation increased. There is evidence to suggest that for advanced economies, the threshold at which inflation becomes negative for long term growth may be as low as 3 percent.[5]

The gains from operating monetary policy to achieve low and stable inflation are difficult to observe and may appear small. Gains from macroprudential policy in moderating credit cycles may be similarly difficult to observe. But, poor policy in either case can cause material damage to long term growth prospects as unsustainable booms unwind.

Conclusion

There is a range of factors that can cause potential output to fluctuate over the short, medium and long terms. Potential output is determined by the economy’s productive base – that is the supply of labour and capital and the efficiency with which these factors are utilised. The quantity and quality of these productive inputs are largely determined by the preferences and choices made by individuals and businesses – how much to work, how much to save, and how much to invest. These preferences can be influenced – for good or for ill – by the policies of central government. Monetary policy cannot persistently affect these preferences. It can however provide a stable backdrop against which individuals and businesses can make decisions about the most efficient allocation of their resources.

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.