American Airlines Group (NASDAQ:AAL)) recently completed another major step towards completing its 2013 merger with US Airways. The Federal Aviation Administration has granted the airliners a certificate to operate as one airline. The merger makes American Airlines Group the world’s largest airline. And with this development, we are closer to the time when we can start seeing the full benefit of this merger. In here, we’ll attempt to dig into some events that have occurred since the merger to see why investors just have to be optimistic about the future of this airliner.

Perhaps the biggest benefit so far is that the merger has helped American Airlines improve its profitability. Before the merger in 2013, American’s gross margin was moving closely to the gross margin of Southwest Airlines Company (NYSE:LUV) below the 50 percent market. However, since the merger American’s gross margin has skyrocketed, now standing at 66.31 percent, compared to Southwest’s 58.73 percent.

It is worthy to mention that Southwest has also been growing its profitability due to its merger with AirTran in 2012. However, with the huge stature of US Airways, American seems to be coming out on top as the Airline industry continues its consolidation.

One of the reasons American is coming out on top in the new consolidated airline industry is that the company chose to merge with one of the biggest competitors possible within the industry. You’d understand better when you consider that AirTran reported a revenue of $2.6 billion for 2010 compared to US Airways’ $11.9 billion. In fact, since Southwest reported a revenue of just $12.1 billion in 2010, the merger is more like American Airlines merging with an airline with a stature similar to that of Southwest.

As a result, American has been able to cut the costs of competing with another “Southwest” in form of the merger with US Airways. As a result, we can expect that, once the merger is complete, American will be more profitable.

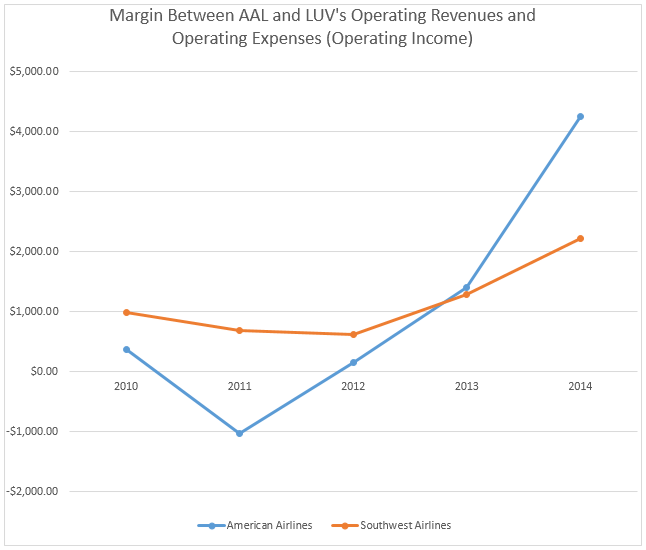

My point that American has been able to cut the cost of competing with a major competitor in US Airways through the merger is also obvious in the spread between the company’s operating revenues and operating expenses – or operating income. I have taken the time to plot a chart of it, in comparison to that of Southwest below.

Data gotten from each company’s 2014 Form 10-K

As the chart shows, prior to the merger, Southwest was able to keep a larger share of its operating revenues as operating income. However, since the merger in 2013, American has improved on this front by a wide margin. By implication, American has been increasing its operating revenues faster than its operating expenses. Again, this is partly attributable to the fact that American now has more time to render quality services than thinking about how to silence competitors – something that will always weigh on operating expenses.

It is important to note that the merger has adversely affected American’s business to some extent. For instance, the merger has brought confusion about airfare, with an interviewed customer complaining that he got different prices for the exact same trip after his US Airways account was merged to American. There are certainly many other customers with similar complaints, and this would have gone to some extent to reduce the company’s traffic. However, once all these kinks have been worked out, as the merger is completed, we can expect more travelers to be confident in American again.

Moreover, the completion of the merger will also help the company ramp up its marketing effort. American’s marketing efforts would be inherently limited right now to afford confusions, since the two companies are probably still working out their policies. However, once the two companies are fully one – standing for the same things and having the same policies – we can expect innovative marketing to begin, which should position the company to take greater advantage of the burgeoning air travel demand.

In addition, I believe American would see more traveler-to-traveler recommendation, as it is also improving its inflight entertainment with improved inflight music and several interesting games. It offers games like chess, casino, just like William Hill’s online casino without the betting. In fact, travelers can see what’s available for each month on its entertainment website. All of this would only help bring out the full benefit of the merger.

Another added value that should help the company on the long-term is that also helps secure its customers by partnering with Allianz (XETRA:ALVG) Global Assistance to offer tailor-made competitive insurance packages for its traveler, which includes but not limited to auto insurance.

By way of bringing it together, the latest single operating certificate development, should remind investors of the benefits that the merger of two of the largest airlines offers. And with a forward PE of 5.52, compared to Southwest’s 11.60, American looks cheap at current levels and now may be a good time to buy shares of American Airlines.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Why It Is A Good Time To Buy Shares Of American Airlines

Published 04/10/2015, 08:46 AM

Updated 07/09/2023, 06:31 AM

Why It Is A Good Time To Buy Shares Of American Airlines

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.