This week appears to be relatively light compared to the previous ones, with the main events on the economic agenda being the US CPIs for July, the UK GDP for Q2, and Australia’s employment report for July.

The US CPIs are forecast to have slowed somewhat, but we don’t expect them to alter expectations around the Fed’s plans. The UK GDP is forecast to rebound and confirm the BoE’s hawkish shift, while Australia’s labor market is expected to stay weak, adding credence to RBA’s dovish stance.

Monday appears to be a relatively light day in terms of economic releases and events scheduled on the financial agenda. That said, it is worth mentioning that today, gold opened with a huge downside gap, breaking below the key support of 1750, and hitting a low of around 1683.

On Friday, the precious metal fell below the important 1790 zone, which had been acting as a floor since July 6, in response to the better-than-expected US employment data for July. Today, the metal opened much lower, perhaps as the break of the 1750 barrier could have triggered massive stop loss orders. In any case, the metal recovered a decent portion of its opening losses during the Asian trading.

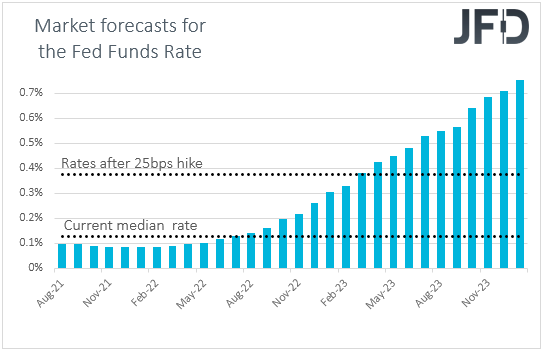

Speaking about the US jobs data, the better-than-expected report may have increased speculation of an earlier tapering by the Fed, and perhaps somewhat earlier interest-rate hikes. Indeed, according to the yields of the Fed funds futures, market participants have now brought slightly forth the timing of when they expect the Fed to start raising interest rates, from April 2023 to March 2023.

Combined with the last week’s hawkish remarks by Fed Vice Chair Clarida and several other policymakers, which came in contrast to Chief Powell’s relatively dovish tone, the strong employment report may keep the US dollar supported for a while more. However, much may depend on the US CPIs for July, due to be released on Wednesday.

On Tuesday, during the Asian session, Australia’s NAB business confidence index for July is coming out, but no forecast is available. In any case, with the RBA extending its bond purchases beyond September, although at a slower pace, and more importantly, noting that interest rates are likely to stay at present levels at least until 2024, we doubt that even a positive surprise would alter market expectations around this Bank.

We stick to our guns that among the commodity-linked currencies, the Aussie is the one that is likely to perform the poorest. We see AUD/NZD as the best pair to continue exploiting Aussie weakness, and this is due to a hawkish RBNZ, which is expected to push the hike button as early as this month.

Later in the day, the German ZEW survey for August is due to be released. The current conditions index is expected to have risen to 30.0 from 21.9, while the economic sentiment one is forecast to have slid to 57.0 from 63.3. Although the current conditions index is suggesting that the economic recovery in Eurozone’s growth engine continues despite fears over the Delta variant of the coronavirus, the economic sentiment reveals cautiousness for the future. Therefore, we don’t expect the euro to receive any support if this is the case.

With the ECB signaling through its new guidance that it is now willing to keep interest rates low for much longer than the previous guidance suggested, and with expectations around an earlier Fed action growing recently, we believe that the path of least resistance for EUR/USD remains to the downside.

On Wednesday, during the European session, we get Germany’s final CPIs for July, but as it is always the case, they are expected to confirm their preliminary estimates.

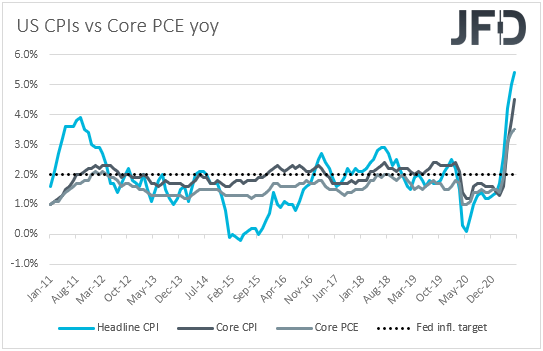

Later in the day, the US CPIs for July are scheduled to be released. Both the headline and core rates are forecast to have slid to +5.3% yoy and +4.3% yoy, from 5.4% and 4.5% respectively. Nonetheless, we don’t believe that such a small decline will be enough to alter expectations with regards to the Fed’s future course of action and thereby halt the dollar’s rally.

Inflation would still be well above the Fed’s objective of 2%, and with underlying pressures still elevated, many market participants could stay convinced that this is unlikely to prove to be transitory, and that some action may be needed soon.

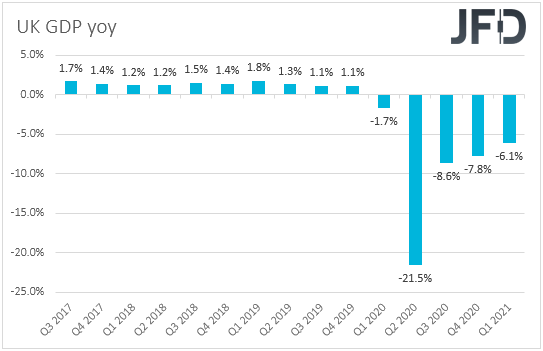

On Thursday, the main event is likely to be UK’s preliminary GDP for Q2, with the forecast pointing to a rebound of +4.8% qoq from -1.6%, something that could take the yoy rate up to +22.1% from -6.1%. Industrial production for June is also coming out and expectations are for a slowdown to +0.3% mom from 0.8% mom.

At last week’s gathering, the BoE lowered the threshold of when they will start reducing their stock of bonds. Specifically, they said that they will do so when the policy rate hits +0.50%, by not reinvesting the proceeds of maturing debt. The previous guidance was for the Bank to not start unwinding its bond purchases until interest rates were near +1.5%.

For some participants this could mean that QE tapering may start earlier than previously anticipated, and a strong GDP print could add credence to that view.

The British pound is likely to receive some support, but we prefer to avoid exploiting any gains against currencies the central banks of which are also expected to start normalizing their policies soon. For example, we would see decent chances for an uptrend continuation in GBP/AUD.

As for the rest of Thursday’s data, during the Asian trading, Australia’s Wage Price index for Q2 is anticipated to have ticked down to +1.4% yoy from +1.5%, while later in the day, we get the US PPIs for July. The headline rate is expected to have ticked up to +7.4% yoy from +7.3%, while the core one is forecast to have held steady at +5.6% yoy.

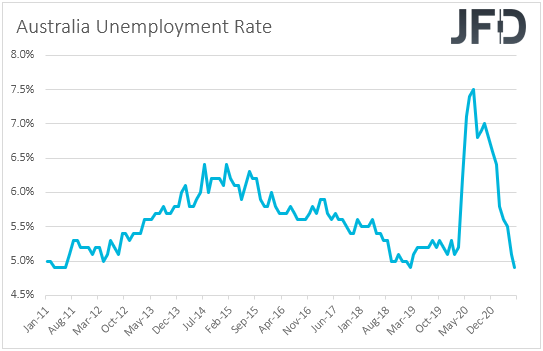

Finally, on Friday, Asian time, we have Australia’s employment report for July. The unemployment rate is expected to have ticked up to 5.0% from 4.9%, while the net change in employment is forecast to show that the economy has added 30.0k jobs, slightly more than June’s 29.1k.

Although higher than June, this would still be a weak number, which combined with an uptick in the unemployment rate, and the slowdown in wages on Thursday, is likely to keep the Aussie under selling interest.

Later in the day, the only indicator worth mentioning is the preliminary UoM consumer sentiment index for August, which is expected to have held steady at 81.2.