Looking back

It was a very strong week for both equities and credit, depending on what part of the world you were in. The S&P hit new all-time highs, along with a lot of equity markets that are at or close to one-year highs (China, Hong Kong, Thailand, Australia to name a few).

The USD strengthened across almost all major currencies for the week, with the EUR, GBP and JPY seeing the biggest weakness at -0.90%, -0.93% & -1.33% respectively. USDJPY seems poised to break the tight trading range in which the latter cross has resided for much of the year, closing the week at 103.95.The S&P closed at 1988.40, +1.71% on the week. US 10 year Treasuries were slightly wider for the week to close at 2.40%.

The US continues to print very strong macro data, with some notable beats on housing data, manufacturing PMI and inflation coming in-line with consensus. Europe continued to disappoint, albeit both Germany and France came in better than expected on their CPI prints.

In Asia, China had the big miss, while Japan surprised strongly to the upside – indicating that there is evidence of a bounce, post the April sales tax earlier this year. The Nikkei finished nine straight sessions of gains on Thursday, closing Friday above the key 15,500 level for the week.

From a central banks’ perspective, the Federal Open Market Committee minutes were interpreted by many to be slightly hawkish, and the Bank of England was the clear surprise as it was revealed that two of the nine members voted for a 25 basis points hike – the first note of dissension in three years.

On the commodities side, gold and oil were down, with the former breaking down past the key 1,300 level, to close the week down -1.81% at 1281. Crude was correlated with a -1.75% down move to close at 93.65.

Looking ahead

Most of the sentiment and mood going into the new week will have been set by digesting the rhetoric from the central bankers that spoke at Jackson Hole. Draghi's dovish speech (about time), clearly painted out what is really needed in Europe, more fiscal structural policy and the need to avoid moral-hazard - good luck with that given yields are where they are.

Yellen's speech, still left most of the market expecting a summer hike in 2015. What is clear is the structural divergence between the Eurozone and the US is set to accelerate & investors should look for the best way to profit off of this multi-year thematic drift. The EURUSD closed at 1.324 on Friday, I'd be surprised if we are not sub 1.20 a year from now - did someone say DAX exporters or am I thinking out loud again?

With macro data on the light side this week, we could see a shift of focus back into the geopolitical hotspots of the world. A rash of suicide bombing over the weekend in Iraq, escalating violence in Libya, no change in Gaza, Merkel's Saturday visit to Ukraine as well as the Russian convoy finally entering the country, will potentially raise the temperature on geopolitical conflicts. Lets also not forget, the last two weeks have been very risk-on.

The key things I’d be watching are Ukraine, where the army has been gaining ground. Tuesday sees a meeting between Vladimir Putin and Petro Poroshenko. Risk is to the upside if some kind of peace/ceasefire agreement could be reached – albeit one can argue, with the separatists clearly losing ground, why should the Ukrainian forces give ground and possibly allow them time to regroup and re-arm? Putin is looking to save face and have an influence in the region whilst Poroshenko cannot be seen to be weak with Parliamentary elections in October (talk about crap timing, or that excellent timing if you are Putin... I am telling you everything is trade!).

However, the fact that they are having a meeting is positive and with the Russian strategic convoy finally now in Ukraine (seems they drove over on Friday through a rebel controlled border) and the Ukrainian winter approaching, the stakes have never been higher.

Those wanting to play the event betting on a better/more-constructive outcome on Tuesday, would probably find a more compelling risk-reward trade being short the USD and the Ruble which closed on Friday at 36.1073 (ie Ruble strengthening) and to a lesser extent going long RSX which closed on Friday at 24.91 (Russian equity ETF).

You probably loss less or get out flat if its a non-event on the FX trade. For the EURUSD, its more binary, as a positive outcome would be good for EURUSD strength but a neutral-to-negative outcome may not buck the downtrend we've been seeing in this cross - its taken out a lot of people!

US 10-year treasuries are far too tight and offer one of the best risk/reward trades out there as a short. Recall that they shot out to 3.05% in Jan this year (that's +65 basis points from the 2.40% on Friday's close) and net-net, I would argue we are now in a much better place globally, especially so with the US economy than we were at the end of 2013 - yes, Europe has issues, but the EMs, China, Japan and the UK are looking a lot better and should pick up the slack.

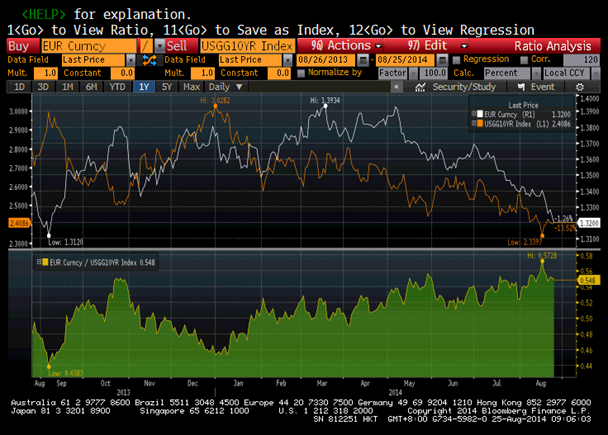

From a trader’s mindset, what’s the worst that can happen on this short? That it might move against you what, 20 basis points - to 2.20%??!! And for that you'd need a very significant shock, or rapid combination of mini-shocks in the market. I think the probability of that happening is low, given the combination of accelerating US growth, current tightness of yields as well as tapering being completed in October. One has to wonder though how much of the EURUSD weakness we've been getting is pushing US treasuries tighter, as the chart below seems to suggest a capital shift.

US 10 year v EURUSD

Europe? That's a whole different kettle of fish – Spanish 10-year treasuries coming in tighter than US government bonds this week – with European yields continuing their tightening trend and I might add, will probably get tighter due to more needed measures by the ECB. Would I go long European credit? Sure, if I was super tactical and trading on a daily basis - would I short them, hell no! There are better risk-reward trades out there than playing with European government bonds. With bunds closing the week at 0.98%, it would not surprise me if we get negative real rates on German 10yr yields over the next 3-6 months - July's CPI came in at +0.80% year-on year, implying +18 basis points of real interest rates over 10 year bonds.

I remain constructive on the S&P going into the end of the year and I feel 2050/2100 by the start of 2015 is not aggressive at all and would put us in the low-to-mid teens in terms of returns for the year. People have been screaming the whole year for a correction in the market and what they are failing to realize is, we've probably just had it! The rule of thumb of a 10% pullback being a correction, does not take into account the dampened volatility & low levels of yields around the world, i.e. perhaps in this kind of market & structural imbalances, -5% is the new -10% for a correction.

For all of you fielding questions from people overarmed with the "bearish necessities" on equities - valuations are too high, earnings cannot keep increasing, rate hikes are coming, inflation is coming (ahem, again! eh?), Europe is falling off a cliff, Europe HAS fallen off a cliff, etc - let me end with a very unappreciated quote from Old Mr. Partridge, taken from that must read book, Reminiscences of a Stock Operator: "Well, you know this is a bull market!"

Lets focus on the big picture. Wishing you all a profitable, rewarding & productive week!

Macro events

Main macro data-points for the week

Monday – Aug 25 (Time Reference: Singapore/Hong Kong Time Zone)

Hong Kong:

- Exports YoY, Jul, 5.3%e, 11.4%p (16:30)

- Imports YoY, Jul, 5.7%e, 7.6%p (16:30)

Singapore:

- CPI YoY, Jul, 1.9%e, 1.8%p (13:00)

Europe:

- IFO Business Climate, Aug, 107e, 108p (16:00)

US:

- Composite PMI Index, Aug P, 60.6p (21:45)

- Services PMI Index, Aug P, 59.1e, 60.8p (21:45)

- New Home Sales, Jul, 425Ke, 406Kp (22:00)

- Dallas Fed Manf., Aug, 13.0e, 12.7p (22:30)

Tuesday – Aug 26

New Zealand:

- Trade Balance, Jul, -475m e, 247m p (06:45)

- Exports, Jul, 3.98bn e, 4.20bn p (06:45)

- Imports, Jul, 4.48bn e, 3.95bn p (06:45)

Singapore:

- IP YoY, Jul, 3.6%e, 0.4%p (13:00)

US:

- Durable Goods Orders, Jul, 7.5%e, 1.7%p (revised) (20:30)

- Consumer Confidence Index, Aug, 89.0e, 90.9p (22:00)

Wednesday – Aug 27

Australia:

- Construction work done, 2Q, -0.5%e, 0.3%p

Thailand:

- Customs Exports YoY, Jul, 3.90%p

- Customs Imports YoY, Jul, -14.03%p

http://goo.gl/JFIlhN (KVP’s macro call on THB strengthening)

Thursday – Aug 28

Hong Kong:

- Retail Sales Value YoY, Jul, -2.5%e, -6.9%p (16:30)

Australia:

- HIA New Home Sales MoM, Jul, 1.2%p (09:00)

- Private Capital Expenditure, 2Q, -0.9%e, -4.2%p (09:30)

Europe:

- Economic Confidence, Aug, 101.6e, 102.2p (17:00)

- M3 Money Supply YoY, Jul, 1.5%e, 1.5%p (16:00)

US:

- 2nd reading, US GDP, 2Q, 3.9%e, 4.0%p [-2.1% in 1Q] (20:30)

- Initial Jobless Claims, Aug 23, 298K p (20:30)

- Continuing Claims, Aug 16, 2500k p (20:30)

- Pending Home Sales MoM, Jul, 0.5%e, -1.1%p (22:00)

Friday – Aug 29

New Zealand:

- Building Permits MoM, Jul, 1.0%e, 3.5%p (06:45)

- ANZ Business Confidence MoM, Aug, 39.7p (09:00)

- Money Supply M3 YoY, Jul, 5.4%p (09:00)

Australia:

- Private Sector Credit YoY, Jul, 5.1%e, 5.1%p (09:30)

Japan:

- Jobless rate, Jul, 3.7%e, 3.7%p (07:30)

- CPI, Jul, 3.4%e, 3.6%p (07:30)

- Retail Sales, Jul, 0.2%e, 0.4%p (07:50)

- IP, Jul P, -0.1%e, 3.1%p (07:50)

Europe:

- Unemployment, Jul, 11.5%e, 11.5%p (17:00)

- CPI, Aug, 0.3%e, 0.4%p (17:00)

- Core CPI, Aug, 0.8%e, 0.8%p (17:00)

US:

- PCE Deflator YoY, Jul, e.1.6%, 1.6%p [Fed preferred metric] (20:30)

- Personal Income, Jul, 0.3%e, 0.4%p (20:30)

- Personal Spending, Jul, 0.2%e, 0.4%p (20:30)

- Michigan Confidence, Aug F, 80.1e, 79.2p (21:55)