When we sell covered calls or cash-secured puts we understand the factors that go into the premiums we receive:

- The option’s exercise price

- The current price of the underlying

- The risk-free interest rate over the life of the option

- Dividends, when applicable

- The amount of time remaining until expiration

- The volatility of the underlying

It is also important to understand the relationship between call and put options and the underlying securities. The value of a call option, at one strike price, implies a certain fair value for the corresponding put, and vice versa. This relates to the arbitrage opportunity that results if there is discrepancy between the value of calls and puts with the same strikes and expirations. Arbitrageurs (the “big boys”, not us) would step in to make profitable, risk-free trades until the departure from put-call parity is eliminated. Understanding these relationships and the reasons behind them will make us all better investors.

European and American style options

Put-call parity relationships generally apply to European style options but can also apply to American style options (the type we use when selling calls and puts) by adjusting for dividends and interest rate:

- If the dividend increases, the puts expiring after the ex-dividend date will rise in value, while the calls will decrease by a similar amount. This is because a dividend distribution results in a decline of share value by the dividend amount on the ex-dividend date

- Rising interest rates increase call values and decrease put values

Synthetic positions and arbitrage opportunities

Every basic position with a stock or option has a synthetic equivalent. Arbitrageurs look to find a divergence between a position and its synthetic equivalent, buy one and sell the other for a risk-free profit. Acting on any such discrepancies quickly eliminates any such differences. Let’s look at a hypothetical example for a call option. Now we sell call options but let’s view this example through the eyes of the call buyer. The maximum loss is the price of the call option while the maximum gain is infinite. Next, let’s look at its synthetic equivalent:

Buy call = buy stock + buy put (one of the six put/call parity rules)

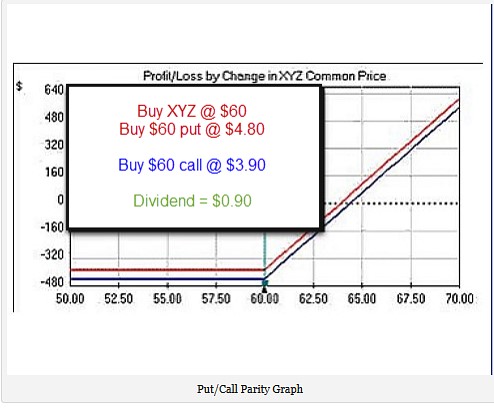

If we purchased a $60.00 call for a stock trading at $60.00 for $3.90, our maximum loss is $3.90, our breakeven is $63.90 (any price below $63.90 at expiration represents a loss for the call buyer) and our maximum gain is infinite. Our synthetic equivalent of buying one hundred shares of stock and one $60.00 put for $3.90 would create the same risk/reward profile. Should the value of either option price diverge, there would be an arbitrage opportunity that Wall Street insiders would jump all over…buy the cheaper option and sell the more expensive one.

What if is there is a dividend ex-date prior to expiration and the dividend amount is $0.90? The share owner would collect the dividend, not the call buyer. This would seem to create an arbitrage opportunity. Here is a risk/reward profile chart depicting this scenario:

Put/Call Parity Graph

The long stock/long put combination would seem to be a better choice because of the upcoming dividend distribution but the laws of put-call parity will make the necessary adjustments decreasing the value of the call option and/or increasing the value of the put option, thereby aligning the two positions and eliminating any arbitrage opportunities. In this scenario, although the share buyer pays more for the put, the dividend distribution will make both positions equal ($4.80 – $0.90 = $3.90).

Discussion

Put-call parity is one of the cornerstones for option pricing. It helps us understand why the price of one option will not move very far without the price of the corresponding options changing as well. If parity is violated, an opportunity for arbitrage exists. These are not a practical source of profits for average retail investors, but understanding synthetic relationships will help us understand options while providing us with even more educational tools.

Market tone

US markets had rose on positive US economic data until the Federal Reserve’s decision Thursday to leave interest rates unchanged due to concerns about global weakness. That led to a selloff in stocks and a rally in Treasuries. This week’s reports:

- The Fed acted as some predicted by leaving interest rates as is for now although Fed officials see the central bank raising rates before the end of the year

- Fed Chair Janet Yellen cited low inflation, “recent global economic and financial developments” and “heightened uncertainties abroad” as deterrents to a September rate rise

- The US Consumer Price Index fell 0.1% in August. Over the past 12 months, the CPI has increased just 0.2%

- Building permits rose 3.5% in August to an annualized rate of 1.17 million, above expectations

- Permits for single-family homes rose to 699,000, the highest since January 2008

- Housing starts fell 3% in August, slightly more than expected, after the expiration of an affordable housing tax credit boosted multifamily home construction in June and July

- Retail sales rose 0.2% in August after July’s gain was revised upward to 0.7%

- Weekly US jobless claims fell to 264,000

- Initial jobless claims decreased 11,000 to 264,000 for the week ending September 12th, the lowest reading in two months

- Continuing claims dropped 26,000 to 2.24 million for the week ending September 5th

For the week, the S&P 500 declined by 0.15% for a year to date return of (-) 4.90%.

Summary

IBD: Uptrend under pressure

GMI: 2/6- Sell signal since market close of August 24, 2015

BCI: The US economy continues to outperform the other major global economies. Since the globalization of the world finances has impacted our stock markets as much as individual corporate events, we must have a broader view of how we should manage our investments. I understand that many of our members are reluctant to actively participate in the stock market at this time and we must all follow our own personal risk tolerances. I did not sell options during the September contracts but plan on entering the October contracts extremely conservatively using in-the-money calls and deep out-of-the-money puts. My monthly goals for these positions is being lowered from 2 – 4% to 1 – 3%. I plan of filling half my positions early next week and the remaining positions mid-to-late week.