Tuesday April 26: Five things the markets are talking about.

It tough to get excited about these markets ahead of the FOMC (Wednesday) and BoJ rate (Thursday) announcements this week. Investors prefer to remain non-committed ahead of the meetings, choosing instead to wade to the sidelines and wait for a stronger market signal.

The Federal Open Market Committee (FOMC) starts its two-day conclave later today, but the announcement will not come until Wednesday at 2:00pm EDT. No changes are expected in rates, and fixed income dealers see only a one-in-five chance of a Fed rate hike in June, though the bank has kept the door ajar for a June rise. The event risk is that the market is more likely to have a ‘hawkish’ surprise than a ‘dovish’ one.

1. Pound Squeeze Continues

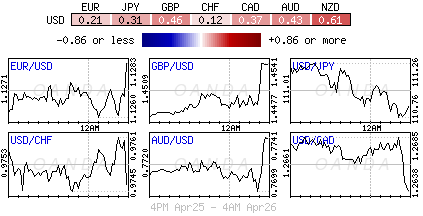

Sterling has rallied this morning to a new ten-week high outright (£1.4572) and a seven-week high against the EUR (€0.7749) as the market assesses whether they have been too hasty in pricing in the prospects of the U.K. exiting the European Union.

The pound’s ‘bears’ have been paring back their Brexit risk-related short positions this week for two reasons. First, U.K. support for remaining in the EU received a lift from last weekend’s comments by U.S. President Barack Obama and second, the odds of Brexit happening continue to drop. The latest ORB poll released this morning indicate that +51% are for staying in the E.U and +43% for leaving (prior poll was +53% and +43%).

The higher sterling climbs the more exposed the currency becomes should the Brexit news flow hit the markets again ahead of the June 23 referendum.

2. Fed’s outlook is hurting the bond flattener trade

The Fed’s patience in raising rates is making some bond dealers nervous, especially those touting the flattening yield curve trade (sell short maturities, the most sensitive to Fed policy changes, and buy longer-term bonds).

The two’s tens spread is currently straddling near its one month highs of +108bps. The up-tick in the premium over the past four-weeks is capturing the broad improvement in risk sentiment and a “cautious” Fed.

Investors are looking for concrete guidance from the Fed, but will they get that with tomorrow’s FOMC’s rate statement? A small percentage of dealers expect the U.S curve to flatten again if Yellen and company happen to shift their stance to a more “balanced” outlook. However, the slower the Fed’s pace, the higher the pressure for investors to lighten up on the flattening yield-curve wagers.

Thus far, the majority see this scenario as less likely at the moment. The 2/10’s flattener has been the dominant FI trade for the last 24-month. Should investors start to worry that the Fed may raise rates more than they currently expect, they may jump back to wager on a flattening yield curve again.

3. Canada’s Poloz Plays New York

Bank of Canada’s Governor, Stephen Poloz, is scheduled to speak at the Canadian-U.S. Securities Summit in New York this morning – the topic, “A New Balance Point: Global Trade, Productivity and Economic Growth.”

Two week’s ago the BoC kept its main interest rate unchanged, but raised its growth forecast for the year on expectations that PM Trudeau’s federal government’s new fiscal measures should have a positive effect on the economy. Note, all G20 economies are watching to see how Canada will “spend and invest” its way to sustainable growth, and not be relying wholly on monetary policy.

Currently, with Poloz expecting the global commodity-price collapse to continue to weigh on growth, as will as slow foreign demand and a recent currency rally (C$1.2640), the market will be interested in what he has to say. Some analysts are expecting the Governor to highlight “the downside risks to growth a little more strenuously” than in his outlook earlier this month. If that is the case, the loonie may struggle.

However, if the governor is a “no show” CAD traders will be looking to Friday’s Canadian GDP print for direction, unless of course Ms. Yellen surprises the market tomorrow.

4. Global equities trade mixed

It’s no surprise that investors are more than happy to keep the bulk of their “powder” dry ahead of the Fed and BoJ rate announcements. Even stocks are gyrating to no particular theme.

Asian equity trading finished their overnight session mixed, as investors remained cautious of monetary policy decisions. Japan’s Nikkei Stock Average ended down -0.5% and Aussies S&P/ASX 200 closed -0.3% lower, while South Korea’s KOSPIadded +0.25%. The outliers were China’s Shanghai Composite Index closing up +0.6% and Hong Kong’s Hang Seng Index gaining +0.5%.

In Europe, local bourses are in the black, mostly on the back of a rebound in crude oil prices contributing to the markets risk-on sentiment and on positive corporate earnings surprises from several companies. So far, North American futures are happy to take its lead from Europe.

5. Crude prices on the rise.

Crude futures are edging higher, mostly on the back of a weaker greenback and on hopes for an easing of the global oil glut situation.

The ‘bears’ would have us believe that gains will be capped by concerns that the battle for market share between Saudi’s and Iran will only intensify further. While the ‘bull’ will argue that the combination of robust demand and weak supply growth will move global oil markets closer into balance by the end of the year.

Despite backing off from last week’s five-month high print, the recent pull back has been limited. Front-month Brent crude futures are trading at $44.75 per barrel, +27 cents on the day, while WTI trades at $42.91 a barrel.

If the market could throw in sustainable global growth there would be a clear winner, however, the demand for market could end up be the outlier.