Monday is a slow day for economic updates, but the short list of numbers scheduled for release will tell us a lot. The reports begin with fresh data on business confidence in Italy, followed by the CBI Distributive Trades Survey for Britain, a proxy for the official retail sales updates from the government. Later, we’ll finally see the delayed September numbers on US industrial production.

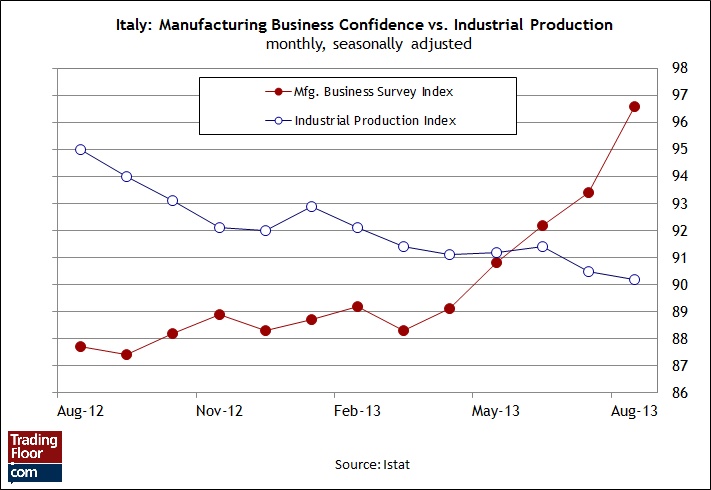

Italy Business Confidence (09:00 GMT) Earlier this month the Bank of Italy was inspired to think positively on the outlook for Europe’s third-largest economy. “The first favourable signs emerge for the Italian economy,” the central bank advised in its October Economic Bulletin. “In recent months, thanks in part to the improvement in the economic cycle in Europe, some positive qualitative signals have emerged for the Italian economy.” Among those signals: last week’s news of a respectable 1 percent increase in industrial sales and a 2.0 percent gain in new industrial orders in August over the previous month. Are these reliable clues that the struggling Italian economy is finally breaking free of its funk?

Today’s update on business confidence will be closely watched for new guidance on the still-precarious view that Italy is on the mend. It’s obvious that the mood in the manufacturing sector is reviving. Istat’s survey of confidence in this corner of the economy jumped to nearly 97 in the September update — the highest in two years. The hard data for industrial production has yet to corroborate the upbeat trend, but that too may be destined to change for the better before the year is out if the revival in expectations among manufacturers rolls on. It doesn’t hurt that there appears to be a positive tailwind blowing through Europe overall. The Bank of Italy’s euro-coin indicator, a monthly estimate of Eurozone GDP, posted its first positive reading in two years last month (pdf). Nonetheless, economists think we’ll see a slight pullback in today’s business confidence number for October. A modest retreat won't mean much in light of this indicator’s sharp gains in recent months. Short of an unexpected tumble of some magnitude, today’s release is likely to offer more support for thinking that Italy might actually be a small but positive force for the Eurozone economy in the months ahead.

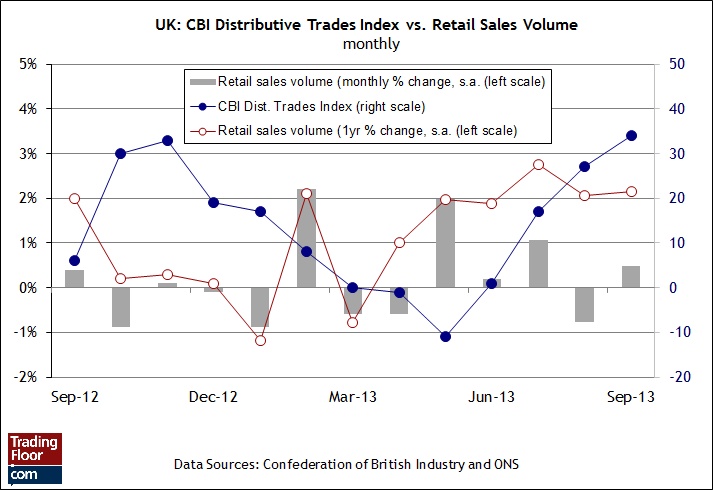

UK CBI Distributive Trades Survey (11:00 GMT) Retail sales have been mixed lately in what has otherwise been a mostly impressive run of positive economic reports for Britain. But while the official numbers on retail sales have yet to mount a convincing run higher, the revival this year in the CBI Distributive Trades Index continues to send a strong signal that consumer spending will strengthen in the months to come.

In the September report from the Confederation of British Industry (CBI), retail sales increased at the fastest pace in more than a year, according to its Distributive Trades Survey. The gain, which surprised analysts, hints at better numbers in upcoming reports from the Office for National Statistics, which is scheduled to publish the October retail sales report on November 14. The case for optimism for consumer spending also draws strength from Friday’s initial estimate of third-quarter GDP, which increased 0.8 percent between July and September — the fastest rate in three years. "What's encouraging about these [GDP] figures is that it's not just services that are growing,” Chancellor of the Exchequer George Osborne told BBC last week. “Construction is growing and manufacturing is growing.” Today’s release from CBI will offer new context for deciding if a similarly cheerful outlook applies to retail sales.

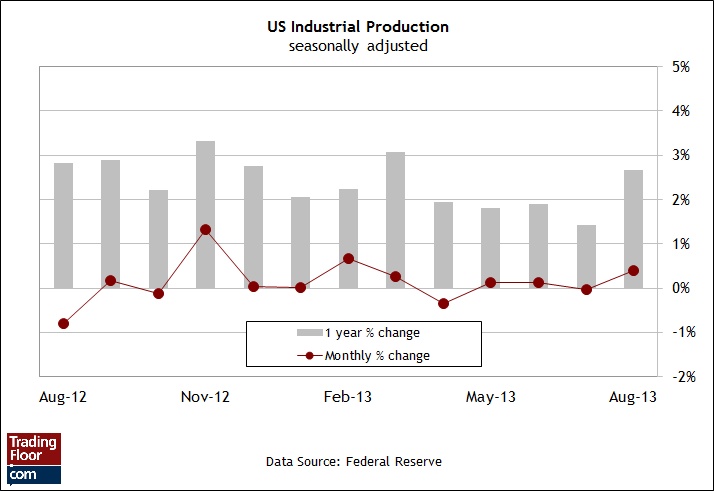

US Industrial Production (13:15 GMT) Today’s delayed industrial production report for September is expected to show a 0.4 percent increase over the previous month, according to the consensus forecast. If so, that would match August’s gain. A pair of 0.4 percent gains would certainly be welcome, offering the best back-to-back monthly comparisons since early 2012. But the weak payrolls report for September raises questions about expectations for last month’s economic profile and beyond. Adding to worries that the crowd may be expecting too much from today’s release is last week’s news that the US Manufacturing Purchasing Managers Index slumped to its lowest level in a year in the flash estimate for October. “The survey showed the first fall in manufacturing output since the height of the global financial crisis back in September 2009,” says Markit’s chief economist (pdf). My econometric modeling also suggests that industrial production’s gain will come in soft relative to the consensus prediction.

Although the monthly comparison will receive most of the attention, keep a close eye on the annual change through September, which is a better guide for gauging the state of the business cycle. In the previous release the year-over-year change posted a substantial improvement with a rise of 2.7 percent through August versus the previous 1.4 percent annual increase. A soft number in the monthly data by itself won’t look as threatening if the annual change manages to remain at or above the 2 percent mark.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Italian Conf., UK Retail Data, US Ind. Prod.

Published 10/28/2013, 03:54 AM

Updated 03/19/2019, 04:00 AM

Italian Conf., UK Retail Data, US Ind. Prod.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.