When I first joined Merrill Lynch, I sat next to a young analyst named Savita Subramanian who was working for Rich Bernstein in strategy research. Though we worked in different groups, I can recall sharing with her everything from Factset data tricks to suggestions about her (then) boyfriend. I have the utmost respect for her as a person and as an analyst.

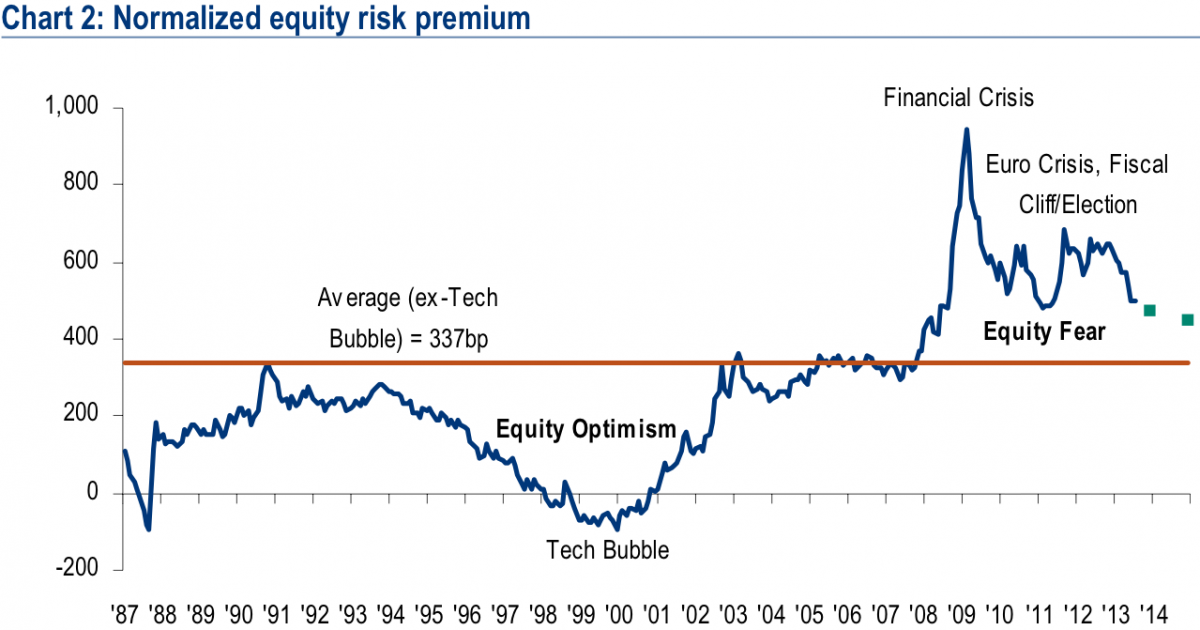

It was with interest that I read (via Business Insider) that Savita Subramanian, who is now BoAML's head of US equity strategy, raised her year-end SPX target to 1750. One of the key inputs is her estimate of the equity risk premium (ERP):

As such, we have lowered our normalized risk premium assumption in our fair value model for the end of 2013 from 600bp to 475bp, which assumes roughly another 25bp of ERP contraction by year-end. We have also raised our normalized real risk-free rate assumption for year-end from 1.0% to 1.5%. Not only have current and future inflation expectations declined since last fall, but long-term interest rates have also begun to rise recently. Meanwhile, our Rates Strategist Priya Misra also recently raised her interest rate forecasts.

Sorry, Savita. I respectfully disagree.

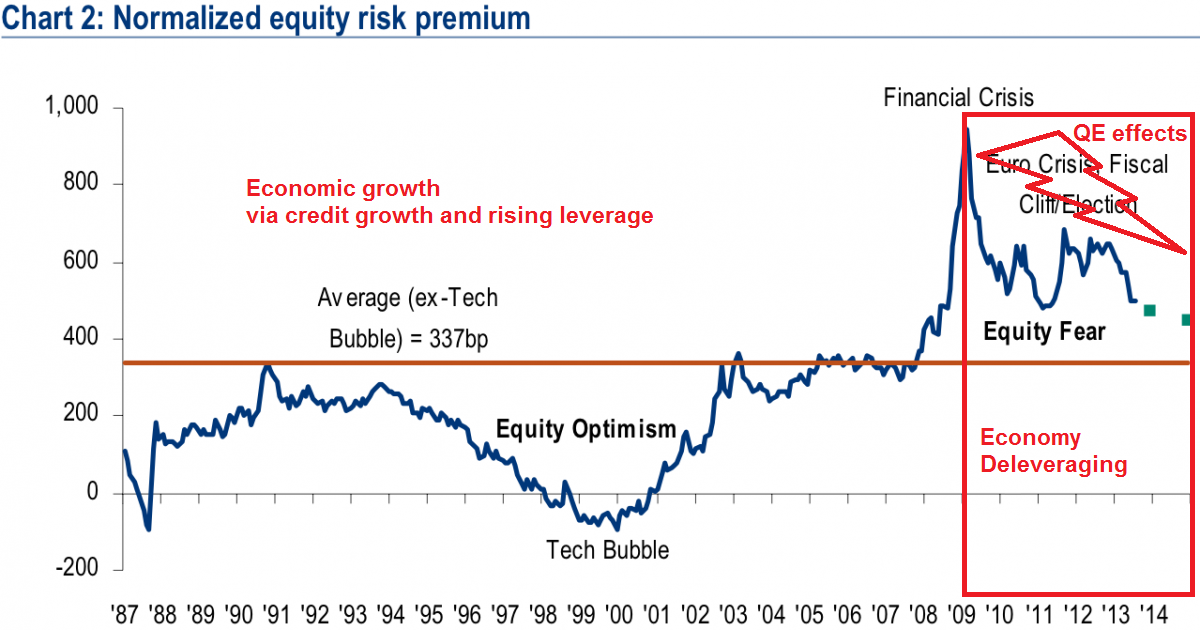

I hate to beat a dead horse here, but I am afraid that much of the Street still doesn't understand the global effects of the deleveraging cycle and subsequent Fed intervention on the perception of risk. Here is the same chart, with my annotations in red:

The first part of the chart, from 1987 to 2009, represents an economic growth phase powered by rising credit growth and rising financial leverage. The latter part, post-Lehman Crisis, is the deleveraging phase of the long cycle. Just read Ray Dalio's explanation of the credit cycle using the Monopoly game analogy and you'll get the idea. If you accept the premise that the two phases of the cycle are different, then you can't apply the norms of an equity risk premium from one phase to another.

Now consider what the Fed did in the wake of the Lehman Crisis (see my previous posts It's the risk premium, stupid! and Regime shifts = Volatility). The Federal Reserve intervened with a series of quantitative easing programs, designed to lower interest rates and lower risk premiums. An artificially lower risk premium forces the market to take more risk, reach for yield, invest, etc. It was thought that such actions would kick start a virtuous cycle of more growth, employment and therefore recovery.

Fast forward to May 22, 2013. The Fed signals that it is thinking of tapering off its QE program. The longer term effect of tapering, regardless of its timing, is to allow risk premiums to find their own natural levels. Since they have been artificially depressed by QE, do you think that they would fall further as postulated by BoAML's analysis?

I recognize that the ERP shot up in the wake of the Lehman Crisis and the various versions of eurozone sovereign debt crisis in the last few years. As fear levels have faded, so should the equity risk premium. Nevertheless, to believe that the ERP will return to pre-crisis levels is to disregard the longer term nature of the deleveraging cycle and the net effects of the Fed's QE programs which depressed risk premiums globally.

Disclosure: Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. ("Qwest"). This article is prepared by Mr. Hui as an outside business activity. As such, Qwest does not review or approve materials presented herein. The opinions and any recommendations expressed in this blog are those of the author and do not reflect the opinions or recommendations of Qwest.

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or Mr. Hui may hold or control long or short positions in the securities or instruments mentioned.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Here's What A Regime Shift Looks Like

Published 07/16/2013, 12:23 AM

Updated 07/09/2023, 06:31 AM

Here's What A Regime Shift Looks Like

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.