As much as things change, they still remain the same, at least when it comes to the euro and European politics. One must become an eternal optimist these days to appreciate the economic strides in the region, which are more like baby steps that beg great leaps of faith. The word crisis has fallen to the wayside after several years of overuse, for the situation never completely heals. As one crisis, like Greece, is dealt with, another waits in the wings to produce another round of uncertainty.

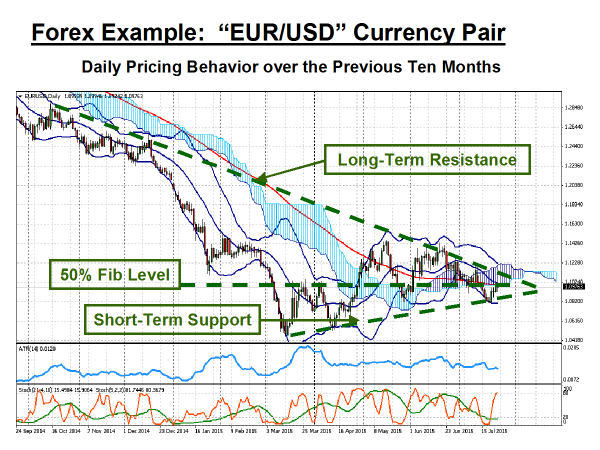

For example, no one is popping the champagne corks just yet over the latest Greek deal. The euro managed a slight bump when Greece moved to the back burner, but there has not been any meaningful news that would engender a robust run up in valuation. Short covering is only a temporary event. As a result, the “EUR/USD” is range bound in an all too familiar symmetrical triangle pattern as depicted below:

The euro has settled into a tight range after its long descent, but the boundaries are on angles this time around that are converging with each passing week. A very similar pattern developed on a weekly basis just prior to its fall from grace in mid-2014. Is history repeating itself? Breakouts from this type of triangle tend to follow the trend that preceded the ranging behavior. Will the euro break for more southerly territory?

From a fundamental perspective, the symmetrical triangle signals that a key decision point is not too far away that will impact the market. Unless you have been asleep in a cave for months, then you would know that this key event is the timing of the Fed’s first interest rate hike. A recent survey of economists delivered an 80% vote for September, as the month when a meager 25-basis point hike will finally become a reality. If there is any stalling, we would expect the triangle to broaden and point to a new date a few months hence, the proverbial kicking the can down the road scenario.

Divergence in central bank policy, however, is still the name of the game for this currency pair. The euro currently sits at the convergence of its 100-Day EMA, the lower boundary of the Kumo Cloud, and a key 50% Fibonacci level, but the prevailing bet at this juncture is that it will fall from this plateau, since analysts believe that the market has only factored in half of the expected rate increase. How far might it fall? Previous support positions will be tested, but the rule for this type of pattern would suggest that a fall to parity with the greenback might not be enough.

If divergence were the one an only thing to worry about, then we could end the story right here and move on to other topics, but such is not the case. The affairs in Greece have only heightened fears of contagion and emboldened many political groups that oppose the euro. The economy of the region is also dependent to a large degree on trade with other parts of the world, especially the United States, China, and Russia. Stock markets may be peaking, another sign of tough days to come. The prognosis is not positive: The patchwork quilt that is europe is beginning to fray at the edges.

What political situation in europe is cause for concern going forward?

As one analyst succinctly stated in a recent article, “The Euro Zone experiment is under fire. The weaknesses of the currency union were exposed in the wake of the financial crisis. And although policy makers have had the years since to devise practical and effective solutions to the many flaws plaguing the Euro Zone, they dithered under the delusion that the measured steps and patchwork solutions to the crises that presented themselves along the way were sufficient to tie the Union over until a sustainable growth trajectory finally returned.”

The problem, of course, is that “a sustainable growth trajectory” never materialized. Debt to GDP ratios ballooned, and quantitative easing programs did little to increase investment in small to medium-sized businesses or lead to acceptable inflation levels. An expanded money supply did lead to a weaker euro, but trade outside the region has been constrained by tepid economic conditions that exist elsewhere. Many of the member states, including the weaker ones, have made some economic progress, but the data is falling well short of what is needed to meet necessary debt liquidation goals.

The employment picture has only gradually improved, and the lack of jobs, especially at more youthful levels, is creating waves of nationalism and anti-austerity movements that can only gain more momentum over time. Spain, Italy, and France will be the next ones in the news, as eyes shift away from tiny Greece to more material pockets of malaise. If the current infrastructure has major problems dealing with the smallest of its members, then how will it fare when it confronts a larger issue? This uncertainty is plaguing the market, and, although foreign exchange reserve managers have saved the euro in the past, it is highly unlikely that this support will rush to its rescue once again.

Will China and other emerging market economies put pressure on the euro?

Worry over China’s ongoing attempt at a soft economic landing continues to grip the headlines, most notably its recent stock market collapse on the Shanghai Composite Index. While most analysts view the current pullback as expected, others point to the historical record for insights. The first insight is that, although the index fell 30%, previous falls have averaged much higher. There may be more room to fall before declaring a full-fledged collapse. The second insight suggests that a collapse in equity values tends to be followed by a similar collapse in industrial output growth in the following year. China is struggling to maintain7% GDP growth for this year. Many project 6.5% growth in 2016, but that figure could be optimistic by as much as 50% or more.

Emerging market economies have also been under fire over the past year due primarily to the U.S. dollar’s major strengthening move and the fall in commodity prices in general and, more specifically, in oil prices, as well. Currency pairings with the USD have been hit hard, but indicators suggest that an oversold condition presently exists. As a result, impacted nations have had to raise interest rates, restrict capital movements, impose import controls, or implement other measures to protect their currencies during the turmoil. This scenario is playing out in many countries, including India, Brazil, Indonesia, Malaysia, the Philippines, Turkey, and South Africa.

Weaker demand for imports will have a direct impact on the euro, too, but the list of consequences does not stop there. In the case of China, Bloomberg has reported that the Bank of China is tapping into its forex reserves to defend the yuan: “After unloading dollars to bolster the Yuan, the central bank may find its reserves out of balance. That may lead it to replenish holdings of the U.S. currency and dump some euros, according to Credit Suisse (SIX:CSGN) Group AG. After the dollar, the euro is the most widely used reserve currency for central banks, International Monetary Fund data show.”

Are stock markets peaking and primed for a great fall?

The “Brilliant Chart of the Week” award goes to the following S&P 500 Index depiction:

A major decline in global stock values would create a sudden capital flow to safe havens, typically U.S. Treasuries and precious metals. The euro would also suffer, but, despite the plethora of articles predicting a significant collapse, many experts claim there is still more play in the current Bull market. In fact, the above chart appeared this week that speculates that a major secular bull market is due to hit in the foreseeable future, if the past is any indication of what may come (Do you believe the past repeats itself?).

The chart purports that there have been two individual “10+ years of a range bound market” before a major long-term market upsurge. In each instance, the surge began after a market low was hit roughly mid-cycle. Fast-forward to the present day, and you can see a profound similarity on all counts, or “déjà vu” all over again. In fact, a major move to the topside has already begun, if you buy into this line of reasoning.

Is now the time to bring out the champagne? What, you are not convinced? Yes, it is time for caution because we are in uncharted waters. Never before have central banks moved in unison across the globe to set interest rates artificially at near-zero levels for so long a period of time. Even central bankers are worried these days about a possible catastrophic unwinding of $3 to $5 trillion in carry-trade positions. A decade ago, a prudent investor might put 5% of his portfolio in foreign securities. Today, that figure has grown to 25% or more, in order to chase after higher returns, regardless of high risk and low liquidity concerns. If and when the “bubble” explodes, it will not be a pretty sight.

Concluding Remarks

In the present environment, the euro could easily rise to 1.11 before meeting heavy resistance. Will a collapsing stock market signal the march to parity with the greenback? As per one analyst, “With no U.S. recession in sight, europe appearing set to move past Greece, and China acting to avoid a hard landing, it's difficult to envision a global recession at this juncture. There exists the possibly for a pullback of 5% or more. If so, it should be viewed as an opportunity, not a concern.”

Uncertainty will persist, however, until the Fed acts on interest rates. Until then, expect more choppiness, as volatility creates its own form of opportunity for the trading community. At the end of the day, the inability of Euro Zone officials to act aggressively to solve major fiscal problems will continue to be its Achilles Heel, and, as confidence wanes in the euro experiment, the euro can head in only one direction, and that one direction is not due north.

Risk Statement: Trading Foreign Exchange on margin carries a high level of risk and may not be suitable for all investors. The possibility exists that you could lose more than your initial deposit. The high degree of leverage can work against you as well as for you.