US markets are closed for Labor Day, but Europe is open for business with the final revisions to August´s manufacturing-related Purchase Manager´s Index data to appear today. This comes ahead of a week that features no fewer than five central bank meetings, starting with tonight’s Reserve Bank of Australia meeting. This week in currency USD It’s all about the data. The Federal Reserve has been doing everything in its power to offload responsibility for policy onto incoming data, and the usual, important first-week-of-the-month data is scheduled to arrive this week. This includes the two Institute for Supply Management data sets (manufacturing tomorrow and non-manufacturing on Thursday) followed by Friday´s US employment report. Any big surprises from the data are likely to have a larger impact than we saw over the summer as the end-of-Quantitative Easing "moment of truth" draws nearer. Looking forward, we have a Federal Open Market Committee meeting the week after next that will include the Fed´s latest forecasts on policy and data.

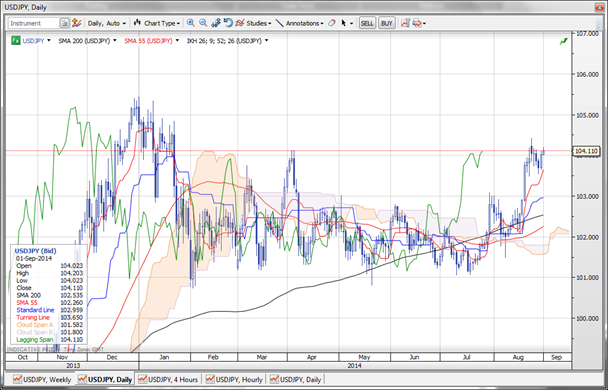

We are generally looking for further USD strength, though to really impress we need to see that strength spreading to the smaller G10 currencies and Emerging Markets — whatever it takes for the market to pull expectations of interest rate hikes further forward, and to steepen them as well. EUR The euro forecast is all about the European Central Bank and the degree to which we get further indications of the magnitude and nature of the Asset-Backed Securities programme. The Euro is pricing in a good deal of ECB easing, so it will take a lot for Draghi to impress the market this Thursday. Increasingly, the euro should be seen as a carry trade currency, and could even rally sharply in negative correlation with risk appetite if global markets are nervous this week, particularly if US data disappoints. GBP The market is holding its breath on the Scottish referendum as the press makes a fuss about poll reliability. After heavy selling of late, this week´s data will be important here, including the Purchasing Manager´s Index data for manufacturing (today) and services (Wednesday). The Bank of England meeting on Thursday should be a non-event, given that rate hike expectations lie out in December and beyond. CHF The Swiss National Bank needs to innovate soon or we will be talking about a testing of the 1.2000 EURCHF floor. More CHF focus to come at the September 18 SNB meeting. JPY The data is clearly less satisfactory here, so how will the Bank of Japan play it later this week? BoJ governor Haruhiko Kuroda will soon have to drop the “everything is going according to plan” line as we move closer to the next round of possible policy moves. In general, the question of to what degree the JPY continues to track the direction of risk appetite remains important, with strong sell-offs in risky assets likely to support in the very near term. The yen will trade weakly on strong US data releases if these result in the markets anticipating a forward move in the Fed´s first rate hike. Clear bearish signs on JPY? Sentiment will likely prove bearish if risk appetite remains robust and Fed policy expectations pick up strongly. On the bull side? The yen could rise if faced with weak risk appetite amid weak US data that results in Fed policy expectations shifting to later in 2015. Anything in between is a bit confusing, though a stable interest rate picture means the focus would mainly be on the direction of risk appetite. Chart: USDJPY This week should tell us whether USDJPY can achieve liftoff through last week's highs and towards a test of the 105.00-plus area from earlier this year. The bull's case is strengthened on stronger US data that moves the Fed's anticipated first rate move forward, though the direction of risk appetite will also play an important role. The Bank of Japan meets on Thursday.  AUD

AUD

The Australian dollar has been very stable and strong lately, with dominant themes including NZD weakness and extremely low global rates amid strong risk appetite. The Reserve Bank of Australia meeting is scheduled for tonight and will certainly have a bearing, especially if RBA governor Glenn Stevens doesn’t maintain his neutral current stance (though it´s hard to see what would change that for now). The currency may be susceptible to weakness if we see strong US data this week and interest rate anticipation ticking higher. CAD A bit of temporary support from the Mergers and Acquisitions front last week, and we are now looking for the 1.0800-plus slippage area to hold USDCAD back from further selling. With a Bank of Canada meeting on Wednesday and an employment report scheduled for release on Friday, expect Bank of Canada governor Stephen Poloz to avoid making dramatic gestures on Wednesday in an attempt to evade potential CAD gains. NZD We are expecting recent NZD weakness to extend as the air continues to come out of Reserve Bank of New Zealand expectations. No key data is scheduled to be released this week. SEK Sweden´s Riksbank is set to meet on Thursday, and risks are generally tilted to the downside for SEK, particularly after this morning’s weak Manufacturing PMI. Watching the 9.13/15 area in EURSEK as the key support area. NOK The upside potential is mostly realized for now. Could be especially vulnerable to EUR firming if Draghi under-delivers on Thursday. Economic Data

- Australia Aug. AiG Performance of Manufacturing Index out at 47.3 vs. 50.7 in July.

- China Aug. Manufacturing PMI out at 51.1 vs. 51.2 expected and 51.7 in July.

- China Aug. HSBC Manufacturing PMI revised down to 50.2 from 50.3 original estimate

- Sweden Aug. Manufacturing PMI out at 51.0 vs. 54.8 expected and 55.1 in July

Upcoming Economic Calendar Highlights (all times GMT)

- Euro Zone Aug. Final Markit Manufacturing PMI (0800)

- UK Jul. Mortgage Approvals (0830)

- UK Aug. Markit Manufacturing PMI (0830)

- Australia Jul. Building Approvals (0130)

- Australia RBA Cash Target (0430)