Income investors had a little scare in May and June. Bond prices took a tumble and dragged down assets that have come to be viewed as bond substitutes -- including popular dividend-paying stocks, MLPs and REITs.

Now that the dust has settled and the income markets have regained some semblance of normalcy, let’s take a step back and review the case for income stocks. With the Fed’s quantitative easing eventually coming to an end and with bond yields likely to rise in the years ahead, does it still make sense to look to the stock market for income? Or might investors be better off buying and rolling over a bond ladder to meet their income needs?

A Look At The Numbers

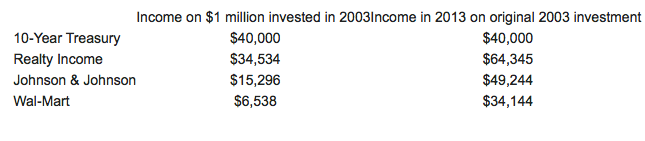

Consider the options you had as an investor ten years ago. In 2003, the 10-year Treasury yielded 3.97%. We’ll be generous and say 4% to keep the math simple. A million-dollar portfolio invested in Treasuries would have paid out an income of $40,000 in the year you bought it…and ten years later, it still would have paid you $40,000 per year on your original purchase price. (Math purists will point out that the yield to maturity calculation is a little more complicated than that, but it’s close enough for our purposes here. We’ll assume you bought the bonds at par and that capital gains are a moot point.)

Over the ten year life of the investment, you would have received $40,000 per year. Of course, $40,000 went a lot further in 2003 than it does in 2013, but we’ll get to that a little later.

A Favorite REIT

Now, let’s do the same math on one of my favorite REITs -- Realty Income (O).

I chose Realty Income for a very specific set of reasons. First, in 2003, its dividend yield -- at 3.5% -- was close enough to the 10-year Treasury yield to make these two viable competitors for the would-be income investor’s portfolio. Secondly, as a low-risk, triple-net retail REIT, Realty Income is a prime example of a stock that has come to be viewed as a “bond substitute” by income investors.

How Did Realty Income Stack Up?

The math here is a little more detailed, but I’ll do my best to keep it simple. A million-dollar portfolio invested in Realty Income at the beginning of 2003 would have bought you 29,516 shares paying $1.17 per share in annualized dividends. That works out to $34,534 in income in the first year -- or about $5,500 less than the 10-year Treasury.

But this is where it gets fun. Unlike the bond, Realty Income actually raised its payout every year. By 2013, those 29,516 shares were paying out $2.18 per share in annual dividends. That works out to $64,345 in annual income -- or $24,345 more than the interest from the bond.

In 2013, Realty Income sported a dividend yield of 4.8%, which isn’t shabby. But your yield based on your purchase price would have been a much more impressive 6.45%. And remember, we haven’t said a word about capital gains; we’re focusing purely on the cash payout, which is ultimately what pays your bills in retirement.

Two Blue Chips

Stepping away from REITs, let’s take a look at two widely-held blue chips that have more or less tracked the market over the past ten years -- Johnson & Johnson (JNJ) and Wal-Mart (WMT). I included both of these names for one critical reason -- both paid comparably low dividends back in 2003. Yet despite paying a modest yield at the time, both had been serial dividend raisers for a long time -- and still are. Their stock prices have had wild swings over the years, but their dividends have been a source of rock-solid stability.

In 2003, Johnson & Johnson and Wal-Mart yielded 1.5% and 0.65% in dividends, respectively. A million dollars invested in each would have paid out $15,296 and $6,538. That stacks up pretty poorly in comparison to the $40,000 you could have received in bond interest by investing in Treasuries.

Fast Forward Ten Years

Those original million-dollar investments in Johnson & Johnson and Wal-Mart would be paying you $49,244 and $34,144, respectively. Wal-Mart’s total cash payout is still a little lower than the payout from the Treasury note, though it rose by more than a factor of five -- and will likely keep rising at a blistering pace for the foreseeable future. And again, this says nothing about capital gains -- or about the reinvestment of dividends, which would have boosted the number of shares you owned and thus your ultimate payout.

Lessons Learned?

Dividend growth matters far more than current yield. When building an income portfolio, accept a lower payout today in the interest of generating a far bigger payout tomorrow. As in so many other areas of investing, delayed gratification has its rewards.

I’ll leave you with one final point on inflation and taxes. The first is obvious. Prices rise over time, and the only way you can avoid getting progressively poorer in retirement is to have an income stream that at least keeps pace with inflation.

Finally, depending on how you are invested (IRA vs. taxable account), taxes will play a role in your “take home” income. If investing in a taxable account, you will pay 15-20% on your dividend income, depending on your income bracket and whether the dividends are “qualified.” Bond interest is taxed as ordinary income, meaning you could be paying a substantially higher rate, depending on your tax bracket.

Disclosures: Sizemore Capital is long O, WMT, and JNJ.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Forget Yield, Dividend Growth Matters Most

Published 07/23/2013, 02:23 PM

Updated 07/09/2023, 06:31 AM

Forget Yield, Dividend Growth Matters Most

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.