The US economy probably continued to grow at a clip of more than 3%* in the third quarter, a Bureau of Economic Analysis report is expected to reveal later today.

Following a weather-related drop of 2.1% in Q1, the economy rebounded quickly in Q2 with output up 4.6%. Still, output was only up 1.2% for the first half of the year and concerns were raised yet again as to whether this was to be 'just another year' of moderate growth.

I think the answer is no. Sure, the full-year growth rate will be depressed due to Q1, but today's report is bound to show another plus 3% growth in Q3 and I expect the same for Q4. In other words, three (expected) consecutive quarterly growth rates above 3% – the US economy is not about to pick up speed... it already has.

With that out of the way, let us dig deeper into the soon-to-be-released Q3 GDP report and the expectations surrounding it. The median estimate of 87 analysts is GDP growth of 3% with a high of 4% (Deutsche Bank) and a low of 2.1%.

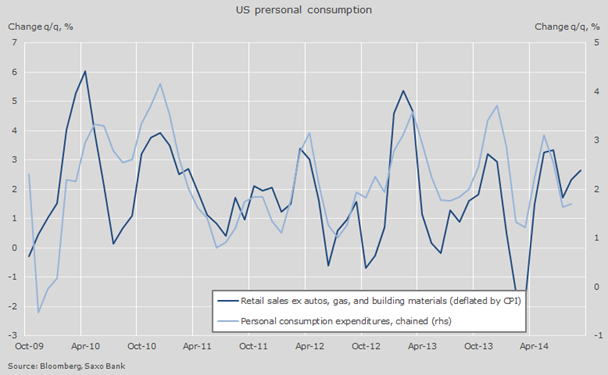

Retail sales struggled in September, falling 0.3% month-on-month, but they nevertheless rose 3.9% for the quarter. Not as impressive as in Q2 (+9.7%), but still a moderate gain in retail sales. Hence expectations for consumer expenditures are lower than in Q2 with consensus looking for growth of 1.9% (2.5% in Q2).

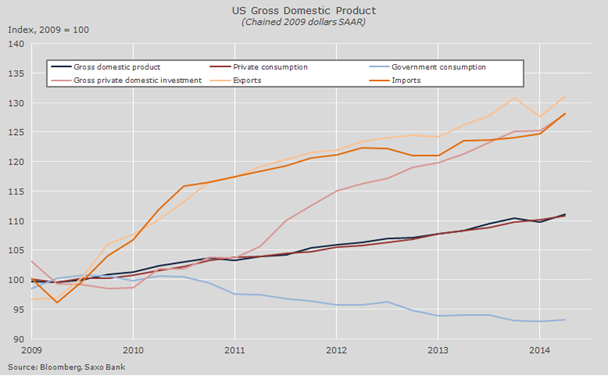

Private consumption growth is thus expected to have moderated in Q3, but other parts of the economy will also have contributed to growth. Investment, both residential and non-residential, did well in Q3 according to available data: housing starts are up 16.6% for the quarter while capital goods shipments climbed 11.1% despite weakness in September.

Private consumption growth may have dropped, but other indicators,such as housing starts, are offsetting this. Photo: Thinkstock.com

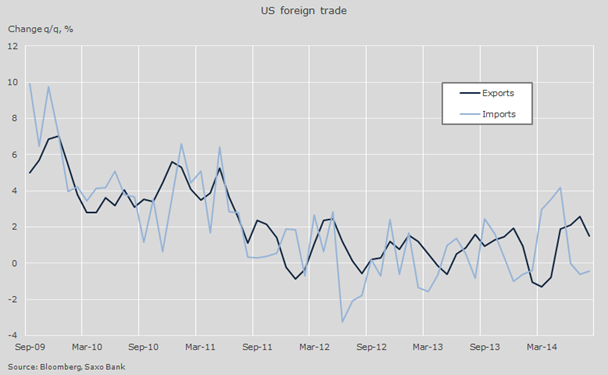

Foreign trade is also expected to have made a positive contribution with (nominal) exports up 8.8% in July-August (September will be an estimate in the GDP report) while imports dropped 0.2%. And this despite the US dollar index gaining close to 8% in Q3.

In addition, the public sector is no longer a drag on the economy, adding to the positive outlook for the US economy. Considering the development in the components mentioned above the consensus forecast of 3% for Q3 GDP growth does not look unreasonable, and I would even say that risk is skewed towards a stronger print. The GDP report will be released at 12:30 GMT.

To subscribe to the Daily Shot letter by e-mail please enter your e-mail address here: Subscribe to the Daily Shot