Since Facebook’s launch in 2004, the company has grown into a social media behemoth as it is estimated that 20% of the globe’s population is on Facebook. The company is once again in focus today though, as FB stock reported earnings for the most recent quarter after the market closed on Tuesday.

Once again, Facebook Inc (NASDAQ:FB) did not disappoint as FB beat the Zacks Consensus estimate of 32 cents a share, posting EPS of 33 cents a share (final, actual, before non-recurring items). FB also beat on revenue by $80 million, reporting $3.20 billion total revenue as opposed to the $3.12 billion estimate. However, many investors and analysts sold off the stock after-hours thanks to worries about costs, pushing shares of FB down 10% in late Tuesday trading, and near a price of $73.35/share.

Still, for the bulls out there, it is important to key in on the revenue growth as this remains a strong point for FB. Take a look at the layout below for how FB’s revenues have been faring:

Other Key Stats

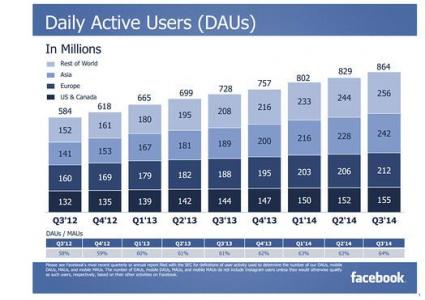

Facebook currently maintains a staggering 864 million daily average users (DAUs) around the globe. DAUs increased to 864 million from 829 million in Q2, and 728 million from Q3 2013. Daily Active users (DAU’s) are considered by many investors and growth metrics to be the single most valuable measure of FB’s growth and success.

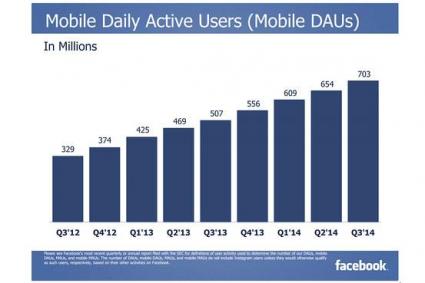

Many investors and traders are alarmed by the very high forward P/E ratio of 61.10, which is in a completely different world when compared to the industry’s average of 2.20. Despite these worries, FB’s Q3 profit almost doubled year over year from 2013, thanks to solid advertising growth, specifically on mobile gadgets. The percentage of advertising dollars from mobile devices rose to 66% in Q3, up by about 62% from Q2, and 49% Q3 2013, while revenues also rose 59%, to $3.20 billion.

FB is overall a winner, and the stock is up by 60% over the past year, and comes out on top when compared to other social media platform stocks like Twitter Inc (NYSE:TWTR) and LinkedIn Corporation (NYSE:LNKD)., while it has also outperformed the S&P 500 as well. All this solidifies FB’s growth and that the social media platform still has a lot of steam to keep the growth and expansionary locomotive moving forward. Below is a chart comparing the S&P 500 Index with FB, TWTR, and LNKD:

There is no doubt that FB’s reign as king is still in the beginning stages. It is nominated to be the next Google by some, but FB faces stiff competition from giant e-commerce retailer, Amazon.com Inc (NASDAQ:AMZN), also another nominee to be the next Google.

In order to broaden the company and its footprint, Facebook’s Mark Zuckerberg has been making key acquisitions like WhatsApp for $22 billion earlier this year. Zuckerberg did not relent, as he went on to offer the startup owners of Snapchat Inc., the mobile app for brief message and photos, a hefty sum of around $3 billion, however, Zuckerberg’s offer was turned down.

The recent conference call was also the first time FB disclosed WhatsApp’s financial performance, which has been disappointing. According to a filing with the SEC on Tuesday, WhatsApp lost $232.5 million in the first half of 2014, considerably higher than the company’s $58.8 million loss in the first half of 2013. Zuckerberg has stated that he does not intend to rush monetizing WhatsApp by allowing advertisements on the messaging application.

Outlook

Thanks in part to the acquisitions and its longer-term focus, many traders and investors argue that FB is also a great growth stock, as it holds the potential to skyrocket, especially after seeing how the social media king crushed estimates. FB saw EPS soar from last year’s figures, and many think that for a stock like FB, the sky is the limit if they can properly monetize their recent acquisitions and expand their user base.

FB has been looking very positive from its Q3 conference call after the closing bell, despite how the stock has been crashing on the company’s announcement that it would be ramping up spending, and how costs may also soar in 2015. The following is a table comparing essential Q2 financials with those of Q3:

Bottom Line

Everyone is excited to see where FB is going to move from this point, as there is no doubt that FB remains a better stock for investors to put their money in, when compared to TWTR or LNKD. Despite LNKD’s huge potential, I would still be very cautious when the company conducts its conference call, as they have missed in the past 3 quarters, and surprised negatively. I would say FB is the clear winner and any smart investor could take the recent slump as an excellent opportunity to buy in.

However, slowly dollar-cost averaging in might be advisable now, as the stock could be shaky on the cost worries, though the company does look to overcome this in the long term. A quick glance at the following growth metric charts will display how FB could be a solid investment now (stats from Facebook):