Economic reports are taking on increasing import as Europe’s economic trend weakens and the crowd becomes fearful that the US may be susceptible to the deceleration that’s swirling about the globe.

In the search for fresh numbers to evaluate the risk, today’s revised data on Eurozone inflation will be a key event. For the US, the main numbers to watch for Thursday are initial jobless claims and the September release for industrial activity.

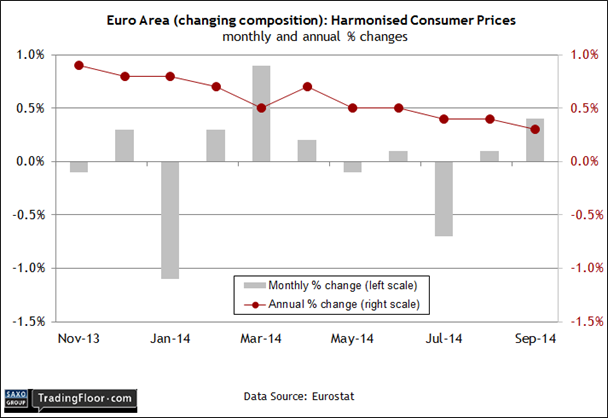

Deflation comes knocking … the Eurozone's CPI figure for September may be lower than

the forecast 0.3%. Photo: Thinkstock EU: Consumer Price Inflation (09:00 GMT) The annual rate of Eurozone consumer inflation for September is expected to be 0.3% in today’s revision, according to Econoday.com – unchanged from the flash estimate issued at last month’s close.

Stability is a good thing at this stage, but it’s clear that deflation is knocking on the door. What are the chances that today’s number will surprise the crowd with a lower-than-expected reading vs. the consensus forecast? Unfortunately, the odds are higher than zero, and perhaps substantially so.

Earlier this week we learned that industrial production fell more than expected in September, leaving output lower by a sizeable 1.9% on a year-on-year basis. The red ink is all the more troubling because the latest slide was fuelled by a sharp decrease in capital goods, which retreated nearly 4% last month compared with a year ago.

These are numbers that you’d expect to see in a recession, and so today’s update on inflation may end up inching lower vs. the initial estimate for September.

A new round of disappointing economic data will probably put more strain on the already challenged politics surrounding monetary policy. With ongoing deterioration in the macro trend, the case continues to strengthen for doing more via the European Central Bank. There’s also a renewed push for additional fiscal stimulus, particularly in Germany, which seems to be slipping into recession as well.

“We need a grand bargain in which national governments understand that monetary policy can only be successful when accompanied by structural reform and responsible fiscal policy,” advised Marcel Fratzscher, head of the German Institute for Economic Research.

There’s still a fair amount of doubt as to whether Europe will receive the policy that’s appropriate for an economy that’s slipped over to the dark side ... again. Perhaps a lower-than-expected reading on inflation today will be convince the austerians that it's time for a change.

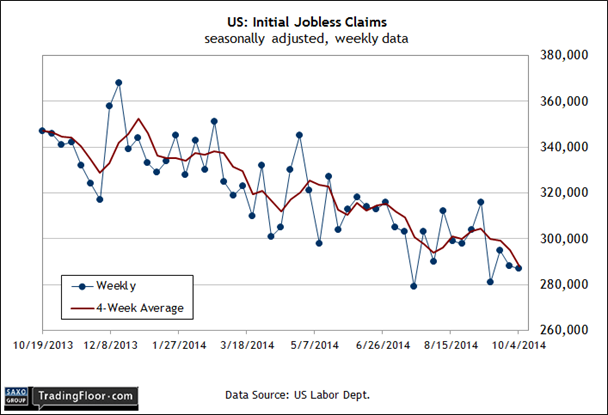

US: Initial Jobless Claims (12:30 GMT) Today’s report on new filings for unemployment benefits will be closely read at a time when fears of macro trouble are on the rise. Although the US economy continues to look resilient next to Europe and Japan, the ongoing slide in the stock market reflects a growing sense that risk is on the rise.

Economists expect that today’s update will show a slight rise in claims to 290,000 (seasonally adjusted) vs. 287,000 in the previous release. That’s effectively no change for such a volatile series. Hugging the 290,000 mark, after all, is a sign that claims are still near the recently established 14-year low (279,000 as of mid-July 2014).

New data that shows the labour market isn’t succumbing to the forces of contraction, which are weighing on Europe is a crucial issue at the moment. Last month’s payrolls report was encouraging, reflecting the strongest net increase in US jobs since June. But confidence is waning for assuming that October will follow suit.

We are, it seems, at a point of rising anxiety in the markets related to fears that the tide may be turning, even for the US. As a result, a bit of hard data that offers some upbeat news for the labour market would be welcome change. By contrast, a deeply disappointing release on this front will stoke a new wave of bearish sentiment.

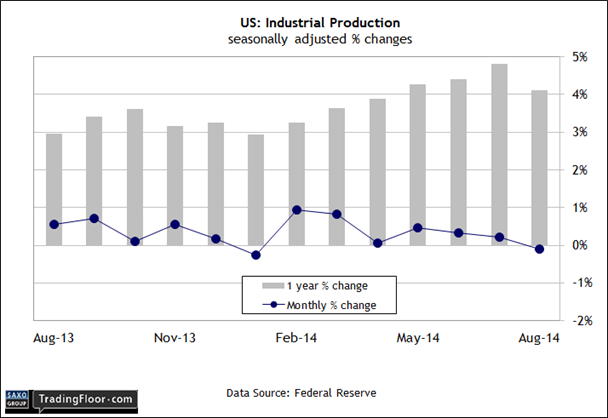

US: Industrial Production (13:15 GMT) Yesterday’s disappointing update on retail sales for September raises the stakes for today’s industrial production release. The crowd’s looking for a decent gain – 0.4% for the monthly comparison. A healthy rebound after the previous month’s 0.1% dip would certainly help minimise the nagging suspicion that the US may be vulnerable to the slowdown (or worse) that’s showing up around the world these days.

Adding to concerns is the sight of producer prices in the US posting declines for the first time in more than a year. Yesterday’s monthly update from the Labor Department showed that inflationary pressure, still mild by historical standards, may again be decelerating. If so, that would be a troubling shift amid the current round of soft data from elsewhere in the world.

But economists are looking for a robust report on industrial production today – news that would help boost confidence that the US economy will continue to expand at a moderate pace. Otherwise, it’s going to be easier to see the US falling prey to the gravitational forces weighing on Europe.