Yesterday, the Greek bond market managed to make an aggressive about turn after news that a Greek government reshuffle diminished the role of Finance Minister Varoufakis in the Euro/IMF bailout negotiations. Today that trend remains your friend; with Greek bonds continuing their rally as the market interprets Prime Ministers Tsipras move as a softening of Athens negotiating stance. Greece’s action is giving the EUR further support ahead of tomorrows FOMC meeting.

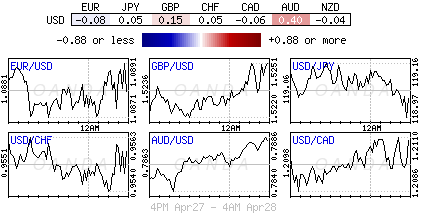

The single unit has managed to print a three-week high (€1.0927) on the belief that a EU/Greek political compromise is but days away. Greece 2-Year yields are down a percentage point to +21%, having hit nearly +30% last week. The inverted yield curve (short rates higher than long rates) continues to suggest a considerable chance of a Greek default, however, signs of relief will hint of the possibility of a solution.

FOMC in the crosshairs

This week’s main event is tomorrow’s FOMC meeting, and the reason why investors are trying desperately not to make any strong moves ahead of the outcome. The problem is that a pre-meet creeping EUR will be making life rather difficult for the EUR bear. They are now much more vulnerable to a EUR short squeeze topside than before.

U.S. policymakers are expected to convey the message that first-quarter data was an aberration, and that they see growth proceeding at a ‘moderate’ pace. With recent retail sales and employment data continuing to show signs of weakness has the USD underperforming and allowing investors to push the timing of the first U.S. rate hike further out the curve.

With the EUR at such elevated levels pre-meeting, fading FED rate hike expectations, supported by a soft patch of U.S. data since the March meet, will risk the squeeze of even more EUR shorts post FOMC. June had been the forerunner for the first-rate hike, but fixed-income dealers are now looking to September or even beyond for the Fed’s rate normalization process to begin. The possibility that the Fed meets dovish expectations, especially with the dollar at current levels against the majors, could easily instigate an elongated EUR short squeeze beyond last months capped highs in the €1.10’s.

The one directional long dollar trade is stretched, coupled with the fact that investors have been more than willing to sell the EUR on rallies, and with no just reward, is making the EUR bear rather nervous. Previously in March, Asian Central Banks had a demand for the USD. With U.S. yields on the back foot, and the possibility of a dovish Fed, these Central Banks will not be in too much of a hurry to want to own dollars. Last month they were the sellers of EUR’s above €1.1000 and were also key in establishing the EUR’s top after the March NFP print.

Most of the dollar longs are against the EUR (+78% vs. +50% in early March). With such a high concentration, a ‘hawkish’ surprise tomorrow could see the market wanting to reestablish dollar longs against the crosses rather than the EUR outright.

Commodity Currencies in the black

The RBA’s Governor Stevens was Australasia’s main focus of attention in the overnight session. Like most commodity and interest rate sensitive currencies, the AUD has been on a tear of late, supported by investors betting that China will take more action to support their economy with stimulus of one kind or another (iron ore is Australia’s biggest export). The AUD is visiting levels that a usually boisterous central banker had issues with (AUD$0.7910). Investors were looking for clues ahead of next week’s RBA meeting. Would a “hot” AUD require another rate cut? Pre-speech, fixed income dealers had priced a +56% possibility of a rate cut by the RBA.

It seems that the Governor did not disappoint, as he expressed concern that the low interest rate environment in Australia makes for a very challenging retirement system. The market seems to have interpreted the remarks as indication that the RBA will likely stand pat next month. Investors will now be waiting for the Fed for directional clues.

Sterling’s feathers cannot be ruffled

The pound is on the verge of braking its seven-week top (£1.5285) and targeting a new handle (£1.5350) despite UK election event risk and worse than expected Q1 GDP data this morning. Sterling is being dragged higher, like all the other majors, by an underperforming USD.

The UK’s Q1 GDP figures show that growth was largely due to the service sector (+0.5%) q/q, with negative contributions from construction (-1.6%) and agriculture (-0.1%). Results like this would suggest that the BoE is expected to maintain its lower-for-longer policy. Governor Carney will not be expected to shift market thinking until there is a material change to inflation risk and wages. GBP positioning will follow the herd for now, at least until investors get a better understanding of Fed thinking.