[Argentina's] central bank’s reserves remain under pressure. Gross foreign reserves have declined $5.0bn ytd to $38.3bn, compared to a $0.1bn increase over the same period in 2012. ... Reserves could fall by nearly $8.0bn this year. ... Any additional increase in reserves related to the tax amnesty program carried out in 3Q (perhaps $2.0-3.0bn) will likely be temporary and counterbalanced by external debt payments. Overall, we expect more controls to target deteriorating external imbalances, but reserves could still fall to $35.5bn by year-end and by another $5.0bn in 2014.

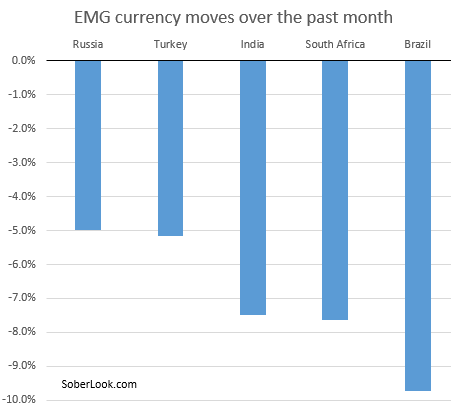

EM bonds have been at the center of the flight from carry and illiquidity. EM local markets lost 1.5% FX-hedged, and almost 4% in USD terms Thursday, the former a record, the latter the worst day since October 2008. EM bond funds continue to see outflows, if more from hard currency than local currency funds. FX weakness is tilting risks toward tighter monetary policy to support the currency is some markets, and this week we penciled in another 50bp of hikes in Brazil. We maintain a short duration stance in EM, with position squaring likely still not done.