Since the middle of last week, emerging market and higher yielding / higher beta currencies have been under renewed pressure. The pure possibility - although still rather remote - of the Federal Reserve potentially tapering its asset purchases already from December this year is enough to spook emerging markets. While the Mexican peso has not been spared any pain in this process, it has - in relative terms to peer currencies - suffered less than during other bouts of risk aversion this year.

Banxico less dovish than anticipated

The last time we analysed Mexican economic fundamentals, emerging markets were in a rather bizarre limbo situation. They were negatively affected by the extended US government shutdown, which fuelled general uncertainty and nervousness. The overall perception was that this shutdown would effectively force the Fed to delay any planned tapering action well into 2014. This was perceived as a major relief factor for capital inflow-dependent emerging market currencies, especially those that are exposed to current account deficits. (For details, see EM Focus: Mexican peso rises as taper delay looks likely.)

Since my aforementioned post, the Banco de Mexico (Banxico) has trimmed Mexican benchmark policy rates by 25 basis points, bringing the official target rates down to 3.5 percent. While this rate decision was broadly in line with consensus, what came as a surprise to markets was the fairly unambiguous indication Banxico made concerning the easing cycle having come to an end, for the time being. Underpinning this was an accompanying statement concerning lower downside risks to growth estimates - a statement that was also somewhat more positive than after the past few meetings.

Reform drive still intact

Concerning actual growth, annualised GDP expansion in the third quarter of this year was still somewhat anaemic at 1 percent. This expansionary number, however, followed contractionary second quarter growth data. At the same time, reform efforts continue in Mexico with the recent passing of income tax changes being just one example. Attention is now focused on energy sector reforms and overall efforts to implement such reforms continue to boost the long-term growth potential of this EM.

Bearing the above-mentioned factors in mind, we revisit the technical outlook for USDMXN, with focus on both sides of the market, plus key triggers and confirmation levels ahead of this Friday's release of the all-important US October non-farm payrolls and employment data.

USDMXN consolidates above the 13.00 handle

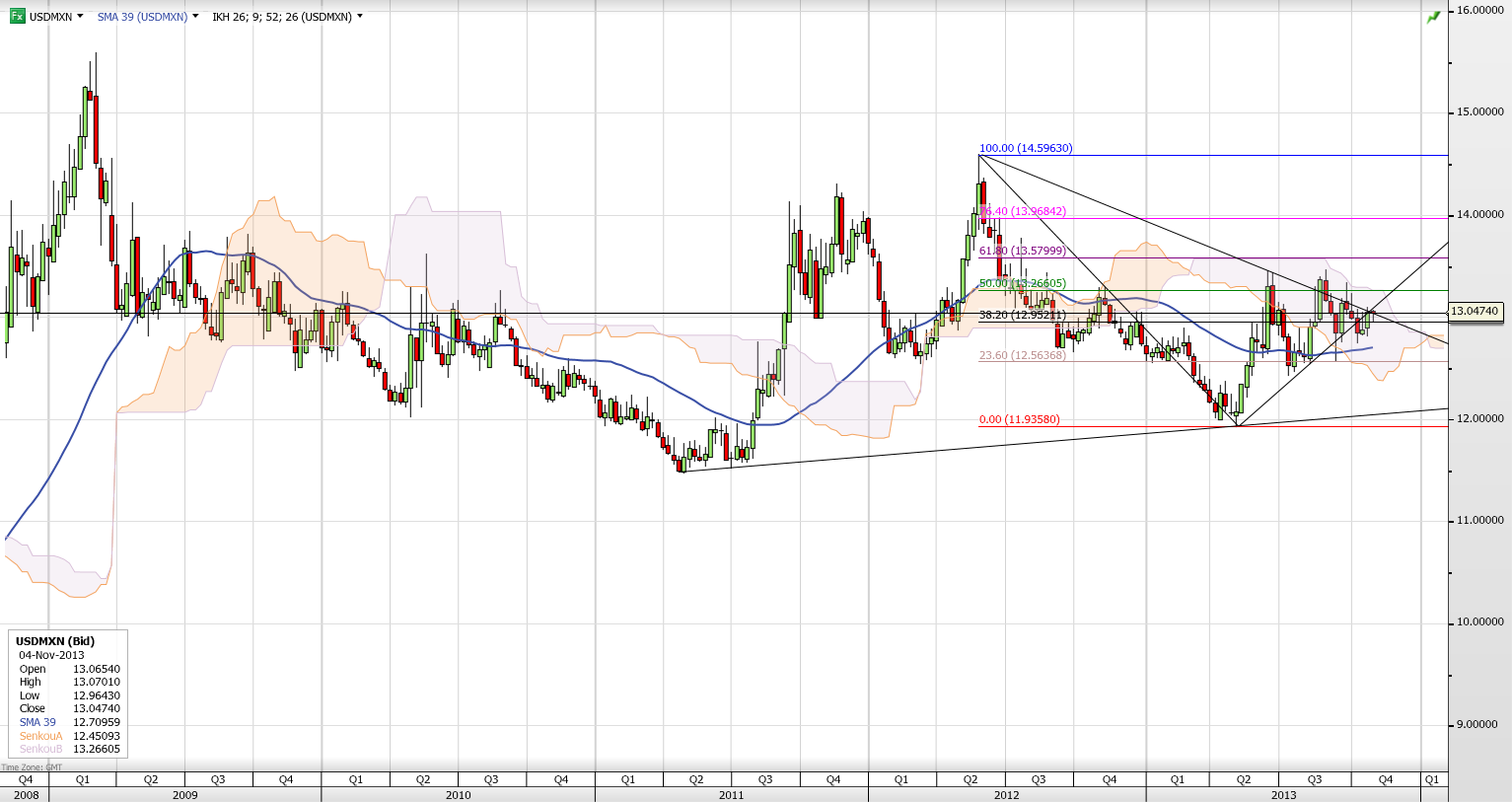

Since our last update, USDMXN has seen relatively tight trading ranges, with daily trading action consolidating above the 13.00 mark, and the general picture settling into a somewhat neutral stance. While USDMXN has managed to stage a critical weekly close below trend-line support from the May 2013 lows, price action has seen the currency pair climb back to the said trend line, which now acts as a short-term resistance level, currently sitting around the 13.10 area. The past few days' of trading have also seen USDMXN stage an up-move above both the 55- and 100-day moving averages.

USDMXN on a daily scale - trading consolidates in the 12.80 - 13.10 area

A move back towards the 12.7480 level would support a more neutral picture. For the downside in USDMXN to re-emerge oncemore in a more meaningful fashion, however, USDMXN would need to see a close on a weekly scale below the 12.5820 support level. This would quickly pave the way towards the 12.5636 mark, which is the 23.60 percent retracement level in the 14.5963 - 11.9358 wave. This in turn would bring into view the July lows at 12.4306.

On the upside, a daily close above the 13.3455 level would bring 13.4655 in sight, which marks both the September highs and acts as a double-top formation on the daily charts. A close above the latter level, in turn, would pave the way towards the 61.80 retracement level on the above wave, sitting at the 13.5800 level.

USDMXN on a weekly scale - price action turns neutral around the trend line

Banxico less dovish than anticipated

The last time we analysed Mexican economic fundamentals, emerging markets were in a rather bizarre limbo situation. They were negatively affected by the extended US government shutdown, which fuelled general uncertainty and nervousness. The overall perception was that this shutdown would effectively force the Fed to delay any planned tapering action well into 2014. This was perceived as a major relief factor for capital inflow-dependent emerging market currencies, especially those that are exposed to current account deficits. (For details, see EM Focus: Mexican peso rises as taper delay looks likely.)

Since my aforementioned post, the Banco de Mexico (Banxico) has trimmed Mexican benchmark policy rates by 25 basis points, bringing the official target rates down to 3.5 percent. While this rate decision was broadly in line with consensus, what came as a surprise to markets was the fairly unambiguous indication Banxico made concerning the easing cycle having come to an end, for the time being. Underpinning this was an accompanying statement concerning lower downside risks to growth estimates - a statement that was also somewhat more positive than after the past few meetings.

Reform drive still intact

Concerning actual growth, annualised GDP expansion in the third quarter of this year was still somewhat anaemic at 1 percent. This expansionary number, however, followed contractionary second quarter growth data. At the same time, reform efforts continue in Mexico with the recent passing of income tax changes being just one example. Attention is now focused on energy sector reforms and overall efforts to implement such reforms continue to boost the long-term growth potential of this EM.

Bearing the above-mentioned factors in mind, we revisit the technical outlook for USDMXN, with focus on both sides of the market, plus key triggers and confirmation levels ahead of this Friday's release of the all-important US October non-farm payrolls and employment data.

USDMXN consolidates above the 13.00 handle

Since our last update, USDMXN has seen relatively tight trading ranges, with daily trading action consolidating above the 13.00 mark, and the general picture settling into a somewhat neutral stance. While USDMXN has managed to stage a critical weekly close below trend-line support from the May 2013 lows, price action has seen the currency pair climb back to the said trend line, which now acts as a short-term resistance level, currently sitting around the 13.10 area. The past few days' of trading have also seen USDMXN stage an up-move above both the 55- and 100-day moving averages.

USDMXN on a daily scale - trading consolidates in the 12.80 - 13.10 area

A move back towards the 12.7480 level would support a more neutral picture. For the downside in USDMXN to re-emerge oncemore in a more meaningful fashion, however, USDMXN would need to see a close on a weekly scale below the 12.5820 support level. This would quickly pave the way towards the 12.5636 mark, which is the 23.60 percent retracement level in the 14.5963 - 11.9358 wave. This in turn would bring into view the July lows at 12.4306.

On the upside, a daily close above the 13.3455 level would bring 13.4655 in sight, which marks both the September highs and acts as a double-top formation on the daily charts. A close above the latter level, in turn, would pave the way towards the 61.80 retracement level on the above wave, sitting at the 13.5800 level.

USDMXN on a weekly scale - price action turns neutral around the trend line