- Shanghai Composite tumbles on decreasing volume

- Continued fall in Indian inflation may prompt rate cut

- Brazil struggling with elevated debt levels

Once again we begin with China where the Shanghai Composite is down 5.2% over the past two days.

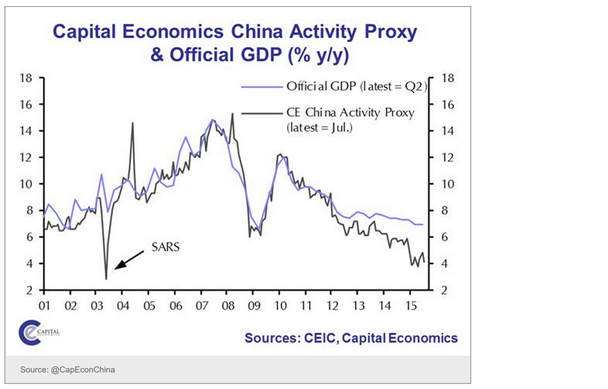

The public has lost interest in the market and trading volumes are declining. China's securities industry did amazingly well last spring, but now we are seeing those gains reversed. Here is an example:

This decline in financial activity is bound to shave a few basis points off the GDP growth figures. Growth estimates vary considerably across the various research groups, but the 7% figure seems to be the thing of the past. There is, however, no evidence of a "hard landing" for now.

Turning to India, the country's wholesale and consumer inflation data now provide plenty of room for the RBI to cut rates. Reserve Bank of India governor Raghuram Rajan may wait for the Federal Reserve to get the liftoff started before implementing the next cut in order to avoid too much pressure on the rupee.

Continuing with the BRIC theme, Russia's corporate credit has tightened dramatically. Aggregate bond and loan issuance is at lows we haven't seen in over a decade.

In Brazil, Petrobras debt is under considerable pressure after the S&P's downgrade. Here is the yield chart on the 2021 5.375% USD bonds.

The nation will struggle with elevated debt levels as the real weakness pushes the domestic value of dollar-denominated liabilities to new highs.

Brazil's sovereign CDS spread is now wider than Russia's.

Turning to Food for Thought, it seems the public wants Joe Biden in this presidential race...

Disclosure: Originally published at Saxo Bank TradingFloor.com