The U.S. Dollar strengthened against most majors and reached an almost one-year high versus the Euro subsequent to a line-up of economic reports denoting that the American economy has rebounded. Analysts agree that August was a phenomenal month for the greenback; and even though it sustained small advances over the past few days, it managed to hold on to its gains. On Friday, the greenback rallied versus the majority of its counterparts despite some soft data on Personal Spending. Official reports showed that Personal Income dipped to 0.2 percent, and Personal Spending, slumped -0.1 percent, denoting that it's the first time it falls in half a year. The good news is that Manufacturing activities in the Chicago area improved, and Consumer Confidence rose even more than previously indicated. Trading experts say that the strength of the U.S. Dollar comes from the fact that investors find the greenback to be a better choice than other assets at this time. The question in everyone's mind is when the Federal Reserve will raise the costs of borrowing money. The Fed indicated that it will wind down stimulus in October, but did not provide a clear cut time-line for raising the cash rate. In the coming days, the U.S. will issue key fundamentals, including the Beige Book and Manufacturing ISM.

Gold Prices traded up and down after dropping on Thursday, when the U.S. announced that its economy grew more than previously announced. The shiny metal slumped as demand for safe havens ebbed in the market, but it's predicted to rally again as situations in several areas of the world seem to be heating up. Futures for delivery in December traded at $1,288.20 a troy ounce on the Comex Division of the New York Mercantile Exchange. Contracts concluded the month of August trading 0.51 percent lower. Appetite for risk assets could decline now that the Ukraine has asked the E.U. for assistance with a situation that has escalated. According to the Ukrainian President, Petro Poroshenko, Russia has continued to invade bringing in convoys of trucks and tanks.

And while five central banks are scheduled to meet this week, the focus will be on the European Central Bank. Sources predict that any announcement by the European monetary authorities could prompt higher volatility than the much anticipated Non-Farm Payroll reports due out this Friday. With consumer prices dipping further, economists expect the ECB will have to issue more measures to fight low levels of inflation. The central bank will also have to come up with the answer to the huge drop in German Retail Sales, the hike in Unemployment throughout the region and the deterioration in Confidence among entrepreneurs and consumers. The experts believe that the problem is not the tough sanctions imposed against Russia, but the strict fiscal policies in effect. The British Pound rallied against the Euro but slipped against the U.S. Dollar. Sources anticipate the Sterling could rebound this week as further positive economic data is set to be released.

The Yen plummeted against the Forex majors subsequent to a number of lackluster economic announcements. For starters, the rate of joblessness went up; household spending plunged more than anticipated, consumer prices slowed more than forecast, retail sales fell, and housing starts dropped along with industrial output. Signs that the Japanese economy faces major challenges may prompt the Bank of Japan to expand stimulus.

The Australian Dollar continued to trade high, remaining as the Reserve Bank stated, "overvalued." Experts in currency trading suggest that the Aussie could decline against the greenback, especially as investments in the mining sector are expected to drop. New Zealand's Dollar registered big declines in August versus its U.S. peer even though the economy of this small South Pacific nation posted an expansion of 3.1 percent in the initial quarter of the year.

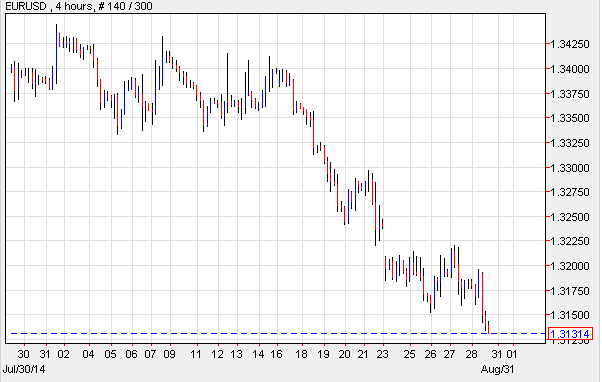

EUR/USD- Euro Slips For The Seventh Week

The EUR/USD continued to trade downwards for a seventh week. This occurred after official reports out of the Euro region showed that consumer prices only went up 0.3 percent this past month, after posting a hike of 0.4 percent in July. In addition, yearly energy inflation slumped from -1.0 to -2.0 percent. Many analysts say that Mario Draghi, the President of the European Central Bank may advocate for leaving monetary policy unchanged at this time; though most economists predict that policy makers won't stand still in light of the recent bounty of negative economic fundamentals. Sources say that the bank may simply reduce the outlook for gross domestic product, or they may announce that they will purchase more assets. The latter option could have a major impact on the EUR/USD, while the former choice could leave the EUR/USD at the current low. Some experts have suggested that the ECB could decide to cut the deposit rate by 10 basis points which would comprise further easing, but others say the bank may not do so until later in September. One thing is for sure; the majority of market participants will be monitoring the outcome of the ECB's meeting scheduled for August 4th.

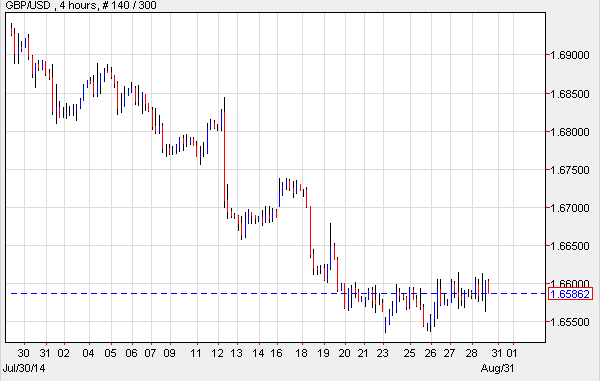

GBP/USD- Pound Could Rally

The GBP/USD rallied after data out of the U.K. showed that the CBI Trends Index went up, while there was another hike in Home Prices. And while the economy of the U.K. has offered signs of improvement, and it's poised to progress better than that of other G-7 nations, economists say that a slack remains in several sectors. Business optimism is said to be at the highest level since 1973 and investments are also on the track for recovery. But exports have gone down, a factor that could affect gross domestic product releases. In addition, inflation is forecast to drift sideways and perhaps conclude the year at 1.6 percent. This week, the Bank of England is scheduled to meet. The markets don't expect a surprise announcement, and this may prompt the GBP/USD to show only slight fluctuations. Should the reports due out in the days ahead prove to be positive, the Sterling may advance versus the greenback.

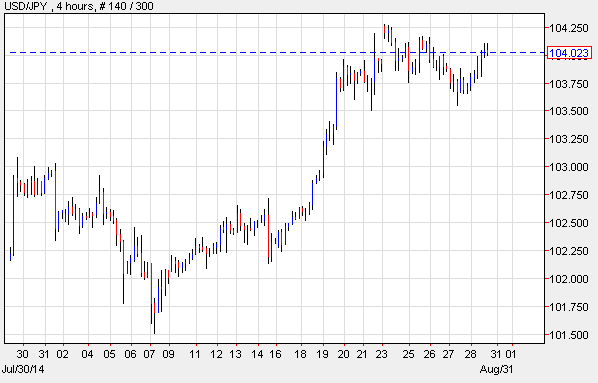

USD/JPY- Japan Issues String Of Poor Data Reports

The USD/JPY advanced, supported by solid data out of the U.S. and as a result of poor macroeconomic fundamentals out of Japan. The later ones indicated that the rate of unemployment has risen in Japan, housing starts have declined dramatically, and activities in the industrial sector have shown a major slowdown. The monetary authorities hoped to see improvements in the third quarter, but at this time, they'll be forced to reassess their stance, given that the economy is still struggling to recover. Consumer spending has continued to decline, months after the shock of the sales tax increase has ebbed. Industrial Output only went up 0.2 percent in July, while economists expected it to gain 1 percent. This week, the Bank of Japan's monetary authorities will meet; but no changes are predicted at this time. Finance Minister, Taro Aso intimated that the effects of April's tax hike is slowly easing but will need to be monitored closely. On Friday, Economy Minister, Akira Amari stated that there's no need to be less than optimistic about consumer spending.

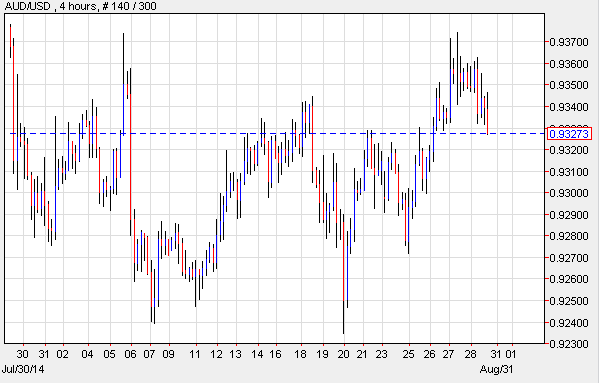

AUD/USD- Aussie Above Desired Range

The AUD/USD traded mixed but continue to fluctuate near levels which the central bank calls "too high." Economists anticipate that the nation's economy will expand depending on how well iron ore prices and exports fare in the months ahead. Recent releases showed that exports to China have gone up, and inflation prospects have improved. However, there's still producer price deflation brought on by industrial overcapacity. This, economists say, will ease, and inflation will slowly advance towards the 3 percent target by the conclusion of 2015.

Today's Outlook

Today's economic calendar shows that all U.S. markets are closed in observance of Labor Day. The Euro region will report on German GDP, French Manufacturing PMI, and the region's Manufacturing PMI. The U.K. will issue BoE Consumer Credit, Manufacturing PMI, Mortgage Lending and M4 Money Supply. And Australia will publish Building approvals as well as Current Account.