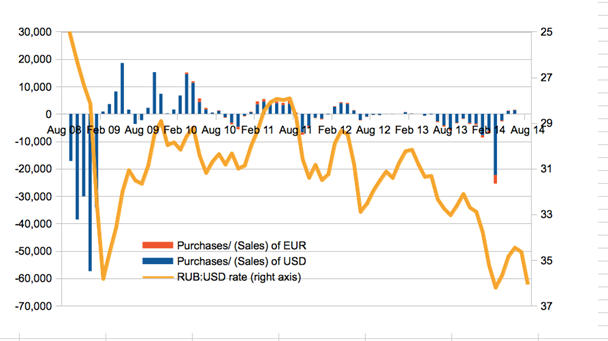

The Central Bank of Russia seems to be going against the grain. If, politically, the screws have been tightened to breaking point, monetary policy appears to be a beacon of economic free will. As the Ukrainian crisis takes another turn for the worse, the central bank, unperturbed, stays away from currency interventions. Official statistics show that the central bank was entirely absent from the currency market both in July and August.

Central bank interventions in currency market Source: www.cbr.ru

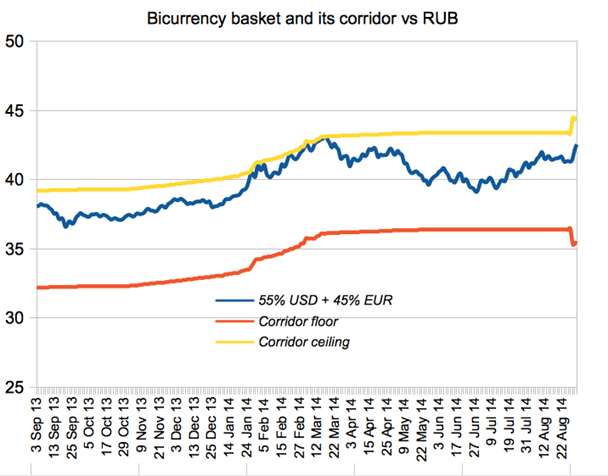

The bank even relaxed its ruble exchange policy in mid-August. It widened the ruble corridor within which the currency can now trade without any support from the central bank. The size of potential interventions, when the ruble moves outside the corridor, was cut by almost two-thirds to $350 million.

The bank has not just rolled back the size of potential support for the ruble back to pre-crisis March levels, it has made it easier to change the ceiling of the corridor. The central bank would only need to spend US$350 mn (vs US$1.5 billion in March to mid-June and US$1bn in mid-June to mid-August) before the ceiling is pushed up by five kopecks.

The current bi-currency corridor is set between 35.4 and 44.4. The ruble might be ready to test the ceiling, with the rate at 42.5 on September 2.

Ruble exchange rate against the bi-currency basket and the central bank corridor

Source: www.cbr.ru

The bank even relaxed its ruble exchange policy in mid-August. It widened the ruble corridor within which the currency can now trade without any support from the central bank. The size of potential interventions, when the ruble moves outside the corridor, was cut by almost two-thirds to $350 million.

The bank has not just rolled back the size of potential support for the ruble back to pre-crisis March levels, it has made it easier to change the ceiling of the corridor. The central bank would only need to spend US$350 mn (vs US$1.5 billion in March to mid-June and US$1bn in mid-June to mid-August) before the ceiling is pushed up by five kopecks.

The current bi-currency corridor is set between 35.4 and 44.4. The ruble might be ready to test the ceiling, with the rate at 42.5 on September 2.

Ruble exchange rate against the bi-currency basket and the central bank corridor

Source: www.cbr.ru

A riddle wrapped in a mystery inside an enigma

Undeterred by political calamities, the central bank keeps steering the ruble towards a free float from next year. It also seems determined to use its interest rates as a tool of inflationary targeting rather than as a prop for the faltering economy, whether the rest of the government likes it or not.

The policy might seem the remaining ray of sanity among the gathering gloom. But the reality might be that the current monetary policy suits the political narrative. Why keep the ruble any stronger, which would effectively subsidise massive capital flight? It is clear that a weaker ruble devalues the assets of many foreign investors and messes up their cash flows. But aren't they queuing for the exit anyway? The hope is that other investors will come, willing to take or ignore the political risk, but those investors are unlikely to veer too far away from export-oriented extraction industries or projects with a quick return.

The ruble in freefall/free float will save currency reserves, which could then be used for worthier causes. The weaker ruble – short term – is also good for the budget, exporters, local producers and the like.

Such a policy will, inevitably, stoke inflation, which, in turn, will eat away most devaluation gains. It is unlikely that the central bank would insist on high real interest rates if the economy remains weak. Cheap money would only lead to more inflation. The combination of a weak ruble and high inflation would deter investments, especially in industries which rely on imported equipment or assembly parts. It would essentially keep the Russian economy in its current commodity-dependent state.

And now for something completely different

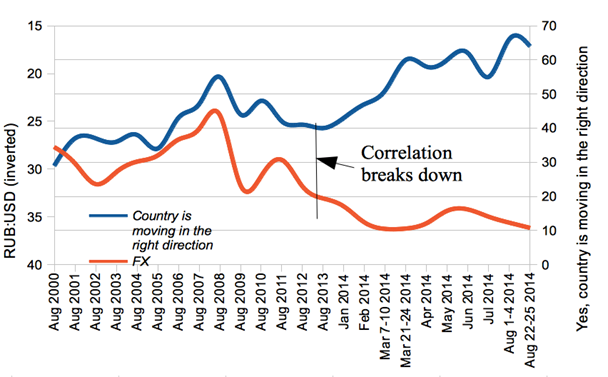

It is not all doom and gloom. You can have some fun with the exchange rate statistics. Why not compare the exchange rate with the popular vote on the state of the country? Since August 2000, the independent polling agency Levada has been asking people "Is the country moving in the right direction?". There is a good visible correlation between “yes" answers and the ruble/dollar exchange rate. A stronger currency means more satisfaction with the state of the country. It does make some intuitive sense.

It is interesting that the correlation broke down completely around a year ago. Russians seem increasingly satisfied with the country's chosen direction, while the currency implies a completely different picture. The last time the ruble was anywhere as weak (August 2009 and August 2013), there was only around 40% support for where the country was going. Either the correlation has now broken down after 13 years or there is something very wrong with the answers and the reported level of the popular support.

Correlation between popularity of country's path and RUB:USD exchange rate

Source: www.cbr.ru

A riddle wrapped in a mystery inside an enigma

Undeterred by political calamities, the central bank keeps steering the ruble towards a free float from next year. It also seems determined to use its interest rates as a tool of inflationary targeting rather than as a prop for the faltering economy, whether the rest of the government likes it or not.

The policy might seem the remaining ray of sanity among the gathering gloom. But the reality might be that the current monetary policy suits the political narrative. Why keep the ruble any stronger, which would effectively subsidise massive capital flight? It is clear that a weaker ruble devalues the assets of many foreign investors and messes up their cash flows. But aren't they queuing for the exit anyway? The hope is that other investors will come, willing to take or ignore the political risk, but those investors are unlikely to veer too far away from export-oriented extraction industries or projects with a quick return.

The ruble in freefall/free float will save currency reserves, which could then be used for worthier causes. The weaker ruble – short term – is also good for the budget, exporters, local producers and the like.

Such a policy will, inevitably, stoke inflation, which, in turn, will eat away most devaluation gains. It is unlikely that the central bank would insist on high real interest rates if the economy remains weak. Cheap money would only lead to more inflation. The combination of a weak ruble and high inflation would deter investments, especially in industries which rely on imported equipment or assembly parts. It would essentially keep the Russian economy in its current commodity-dependent state.

And now for something completely different

It is not all doom and gloom. You can have some fun with the exchange rate statistics. Why not compare the exchange rate with the popular vote on the state of the country? Since August 2000, the independent polling agency Levada has been asking people "Is the country moving in the right direction?". There is a good visible correlation between “yes" answers and the ruble/dollar exchange rate. A stronger currency means more satisfaction with the state of the country. It does make some intuitive sense.

It is interesting that the correlation broke down completely around a year ago. Russians seem increasingly satisfied with the country's chosen direction, while the currency implies a completely different picture. The last time the ruble was anywhere as weak (August 2009 and August 2013), there was only around 40% support for where the country was going. Either the correlation has now broken down after 13 years or there is something very wrong with the answers and the reported level of the popular support.

Correlation between popularity of country's path and RUB:USD exchange rate