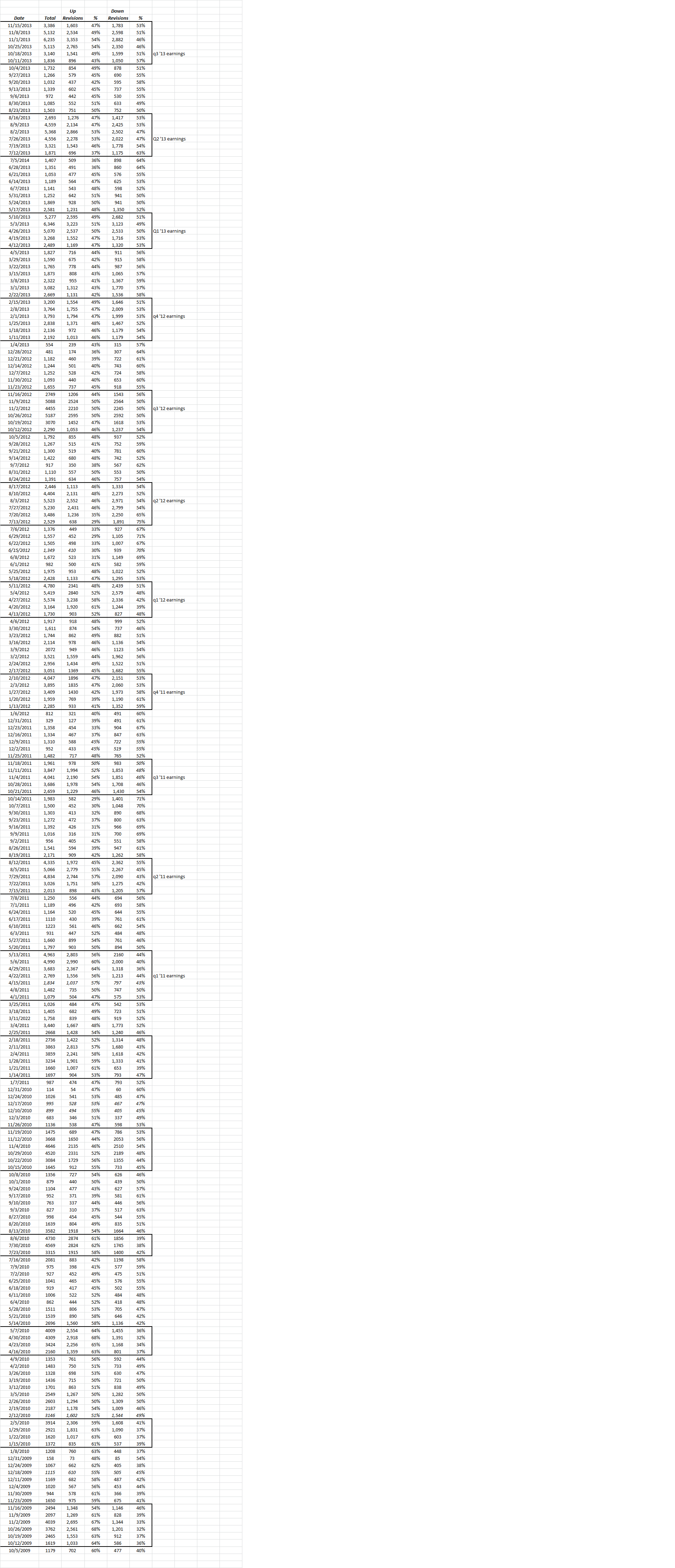

In a perfect example of the navel-gazing we (I) do around S&P 500 earnings data, the very detailed and elaborate Excel spreadsheet reporoduced above, is a history of the S&P 500 Earnings Revisions (by upgrades and downgrades) by week, from late 2009.

Since our Weekly Earnings Update captures percentage changes in the S&P 500 Aggregate and by sector, this Weekly Revision History is a separate report published by ThomsonReuters, that shows the number of upgrades vs. downgrades or “estimate revisions for Fiscal Year 1 period for all companies in the US over the previous 7 days.” The number of companies in this revision data is about 9,000 per ThomsonReuters’ Greg Harrison, and comprises all public companies, so this data is far broader than the S&P 500.

To keep this post short and sweet, we have highlighted or blocked out the peak earnings reporting periods for US public corporations each quarter, and you can see the trends in evidence since the 3rd quarter, 2009:

1.) Despite the “nattering nabobs of negativism” who pick and choose their earnings revisions info, the fact is, during the heart of earnings season which usually comprises the 2nd week of January, April, July and October, through the 2nd week of the following month (or when Wal-Mart reports, whichever is the latter), the percentage of upgrades still exceeds downgrades, although by a smaller percentage than what immediately followed the 2008 Financial Recession;

2.) During the “off-periods” which are the periods outside the primary reporting period, typically the percentage of downgrades exceed upgrades, which is frequently cited by some commentators as reason to be bearish. However to be clear, and as I understand it, an increase in the GE EPS estimate for 2013, by one analyst, is weighted exactly the same as a lowering of the 2013 EPS estimate for an obscure micro-cap company.

3.) While this has been a productivity-driven recovery, including SP 500 earnings, I suspect the next surge in analyst upgrades vs downgrades will occur when revenue growth starts to improve, which has been locked in the low-single digit range for several years;

4.) While it is strictly a personal opinion, this data continues to reinforce the “institutional pessimism” we’ve seen around the stock market. Analysts don’t really lift numbers or boost estimates until they see the earnings data, and even then, given the improvement in quarterly earnings growth we’ve seen from the first day of the quarter through the end of the reporting period, analysts usually get too bearish just in front of earnings, and then lift numbers after seeing results.

5.) According to this spreadsheet, the number of weeks with greater than 50% positive revisions is getting thin, which tells me we need to see better revenue growth;

Barry Ritholz had an interesting graph from McKinsey & Co. on his blog this weekend, which Jeff Miller blogged about in October, 2010. Jeff Miller and I have talked about this at length over the last few years: analysts start out optimistic, then slash earnings growth expectations, typically to their low just as the quarter is about to be reported, and then actual results are usually higher, by 2% – 4%.

This is one reason we track the “forward 4-quarter” S&P 500 estimate of the S&P 500. If the stock market is a discounting mechanism, the forward estimate should explain current stock market movements better than the current quarterly reports (and I sure wish I could prove that statistically).

The bottom line is I thought readers would like to see earnings revision data comprehensively, to draw their own conclusions.

We’ll look at the forward estimate trends shortly.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

A Brief History Of Weekly Earnings Revisions For 9,000 Public Companies

Published 11/17/2013, 11:40 PM

Updated 07/09/2023, 06:31 AM

A Brief History Of Weekly Earnings Revisions For 9,000 Public Companies

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.