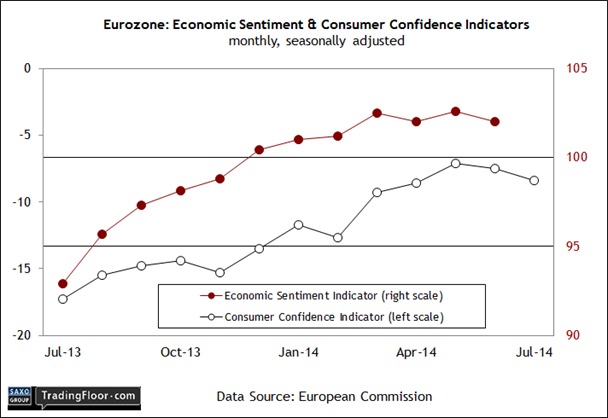

- Russian sanctions will have detrimental affect on EU growth

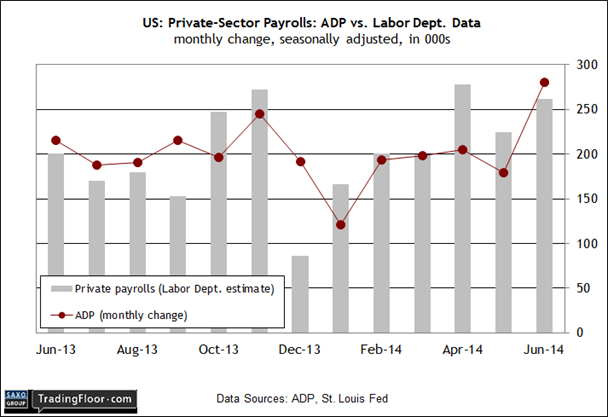

- Positive US employment expected to continue

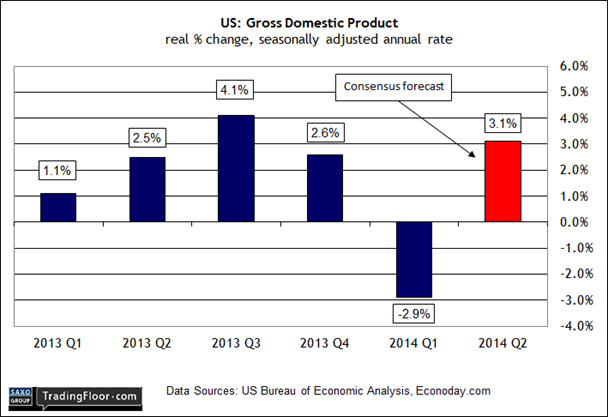

- 3 per cent US GDP growth 'will be sustainable'

A brighter profile can be found in last week’s Flash Eurozone PMI Composite Output Index, which climbed to a three-month high for this month's initial reading. “Many companies reported that business had picked up again in July after an unusually high number of holidays and a knock-on effect of mild winter weather had depressed activity in prior months,” Markit Economics advised.

The question now is whether the optimism via the PMI release is subject to revision if Europe moves ahead with tougher sanctions?

US: ADP Employment Report (12:15 GMT) The market will be eager to see today’s estimate of private-sector payrolls from ADP. The economy has been creating jobs at a moderately faster pace in recent months and so today’s ADP release will be widely read as a clue for anticipating Friday’s official employment data from the government.

As for the ADP numbers, the June report was unexpectedly strong, with non-farm private payrolls growing by 281,000. That’s the biggest monthly advance since November 2012. As it turned out, the subsequently released June figures from the Labor Department were encouraging as well, with private payrolls rising 262,000 last month, or just below the best monthly comparisons we’ve seen in the last two years.

The consensus forecast sees today’s ADP estimate delivering another healthy advance, although the projected 235,000 increase is well below the previous 281,000 gain. Nonetheless, it would be surprising to see today’s report deliver something less than encouraging results. Indeed, last week’s news that jobless claims dropped to an eight-year low for the week through July 19 suggests that payrolls will continue to expand at a relatively accelerated pace for the near term.

US: GDP (12:30 GMT) The crowd’s expecting a substantial rebound in today’s initial estimate of second-quarter GDP report from the Bureau of Economic Analysis. That’s also my expectation via my econometric modelling. But let’s be clear: a big disappointment would weigh heavily on sentiment.

The consensus forecast anticipates a 3.1 percent increase in today’s “advance” estimate of GDP for the second quarter. If you’re wondering what could derail the upbeat outlook, consider the latest numbers for real personal consumption expenditures (RPCE), which dominate the GDP figures. In April and May, RPCE declined (the June data for RPCE will be published on Friday). The back-to-back run of red ink will weigh on today’s GDP estimate. Should we worry? No, according to the consensus forecast. The prevailing wisdom is that today’s revised numbers will compare favourably with previous estimates.

“Pretty much across the board, components will look better,” said Jim O'Sullivan, chief US economist at High Frequency Economics. “I do think we can sustain a 3 percent [GDP] growth number for the next couple of quarters.”