Today’s macro calendar is busy. Investors will be focusing on the flash estimate of the Eurozone’s August inflation figure, as the European Central Bank’s policy-setting governing council prepare to meet and hold a press conference on Thursday, September 4.

The European morning brings plenty of interesting data from the two big crisis countries: Spain and Italy. Spain’s current account, business confidence and retail sales, and Italy’s unemployment, inflation and gross domestic product are published today. Yesterday morning, Spain reported surprisingly strong GDP and economic sentiment readings, and its export-led recovery seems to be going well, with domestic spending increasing. Italy has been lagging and unable to get on the growth track. In fact, in real GDP terms, Italy is back to levels last seen in 2000. Politically, Spain has been approaching Germany and Brussels, while France and Italy seem to have drifted in the opposite direction. With key European Union top jobs being doled out, perhaps Spain’s tactic is to be a model of austerity, while simultaneously running huge deficits. The EU and Germany need a positive example, and with Spain playing that role, perhaps its deficits will be overlooked for a while. Interestingly, German chancellor Angela Merkel declared on Monday that her government backs the Spaniard Luis de Guindos to head the all-important euro group.

The latest escalation of the Ukrainian crisis has led to emergency meetings being planned for over the weekend, where further sanctions against Russia will be discussed. A need for a rapid response is clear, but it is uncertain if Europe has the resolve to tighten the screws enough to make a difference. I don’t think the Kremlin would have escalated unless they thought it would bring them a better deal.

US data is always of interest, and after yesterday’s nice upward revision to second-quarter GDP (see Stephen Pope's comments on TradingFloor), signs of further strength and inflationary pressure could come from the personal income and spending data. The University of Michigan consumer sentiment data should receive less attention, as plenty of other sentiment indices have already been published for the same data period.

Germany July Retail Sales (06:00 GMT)

German retail sales are expected to post a monthly gain of 0.1% in July, after a 1.3% increase in June. The expected change from the previous year is 1.5%, up from 0.4% in June. Germany has mostly resisted monetary easing in Europe. This partly follows from the fear of debt mutualisation through the ECB’s unconventional monetary policies and antipathy toward inflation. Germany also worries that should monetary policy be eased, the crisis countries will have less incentive to implement reforms. At the point where everyone is suffering, that argument should be thrown out the door, but there is a tendency that Germany only gives in when its own direct interests are in jeopardy. Thus, Europe’s best hope is terrible retail sales in Germany. The GfK consumer survey, which reported earlier this week was surprisingly negative, but that should not yet show in July's retail sales. Here is a short article discussing how Germany’s situation dominates economic policy in Europe.

Eurozone August Flash Consumer Price Index (09:00 GMT).

The inflation rate is expected to have continued to fall in August to 0.3%, down from 0.4% in July, and way below the ECB’s 2% target. Core inflation, which excludes volatile food and energy prices, is expected to remain unchanged at 0.8%. While the difference between the core and the headline reading is notable, and suggests that one key reason for the low headline reading is the currently low energy prices, which, according to at least ECB president Mario Draghi, is also good for the economy as it lowers costs, the low core inflation is all the evidence we need to say the ECB is way below its target.

The ECB’s main tools in its fight against the low inflation are the Targeted Long Term Refinancing Operation, or cheap loans to banks, which will be available to the markets from September 18, and the Asset-Backed Securities program, which is in the works and will take a considerable amount of time before it is available. It has been speculated, and Draghi has hinted, that there are additional measures that could be used if the inflation outlook does not improve – but the effectiveness of a US-style quantitative easing program in Europe would be difficult to implement for political and practical reasons.

Still, investors do not expect next week’s policy-setting meeting to come up with anything but further promises to act if the TLTRO fails to have the desired effect. With the Ukrainian crisis remaining a big threat to the outlook and break-even inflation rates suggesting markets do not see inflation picking up in the short-to-medium term, perhaps the best one could hope for is a stabilisation of the inflation rate to current levels.

One thing to watch are comments over the recent fall of the euro – EURUSD is now at 1.32, while it visited 1.40 in the beginning of May. Lower values of the euro should help lift the inflation rate, but some estimates that have been thrown around suggest that the recent fall would only add about 0.1% to the annual inflation rate.

The July unemployment rate will be released at the same time, but as it is not a policy target of the central bank, it should get less attention. Still, it has been trending down for several months now, and it would be nice to see the gradual decline continuing.

The European morning brings plenty of interesting data from the two big crisis countries: Spain and Italy. Spain’s current account, business confidence and retail sales, and Italy’s unemployment, inflation and gross domestic product are published today. Yesterday morning, Spain reported surprisingly strong GDP and economic sentiment readings, and its export-led recovery seems to be going well, with domestic spending increasing. Italy has been lagging and unable to get on the growth track. In fact, in real GDP terms, Italy is back to levels last seen in 2000. Politically, Spain has been approaching Germany and Brussels, while France and Italy seem to have drifted in the opposite direction. With key European Union top jobs being doled out, perhaps Spain’s tactic is to be a model of austerity, while simultaneously running huge deficits. The EU and Germany need a positive example, and with Spain playing that role, perhaps its deficits will be overlooked for a while. Interestingly, German chancellor Angela Merkel declared on Monday that her government backs the Spaniard Luis de Guindos to head the all-important euro group.

The latest escalation of the Ukrainian crisis has led to emergency meetings being planned for over the weekend, where further sanctions against Russia will be discussed. A need for a rapid response is clear, but it is uncertain if Europe has the resolve to tighten the screws enough to make a difference. I don’t think the Kremlin would have escalated unless they thought it would bring them a better deal.

US data is always of interest, and after yesterday’s nice upward revision to second-quarter GDP (see Stephen Pope's comments on TradingFloor), signs of further strength and inflationary pressure could come from the personal income and spending data. The University of Michigan consumer sentiment data should receive less attention, as plenty of other sentiment indices have already been published for the same data period.

Germany July Retail Sales (06:00 GMT)

German retail sales are expected to post a monthly gain of 0.1% in July, after a 1.3% increase in June. The expected change from the previous year is 1.5%, up from 0.4% in June. Germany has mostly resisted monetary easing in Europe. This partly follows from the fear of debt mutualisation through the ECB’s unconventional monetary policies and antipathy toward inflation. Germany also worries that should monetary policy be eased, the crisis countries will have less incentive to implement reforms. At the point where everyone is suffering, that argument should be thrown out the door, but there is a tendency that Germany only gives in when its own direct interests are in jeopardy. Thus, Europe’s best hope is terrible retail sales in Germany. The GfK consumer survey, which reported earlier this week was surprisingly negative, but that should not yet show in July's retail sales. Here is a short article discussing how Germany’s situation dominates economic policy in Europe.

Eurozone August Flash Consumer Price Index (09:00 GMT).

The inflation rate is expected to have continued to fall in August to 0.3%, down from 0.4% in July, and way below the ECB’s 2% target. Core inflation, which excludes volatile food and energy prices, is expected to remain unchanged at 0.8%. While the difference between the core and the headline reading is notable, and suggests that one key reason for the low headline reading is the currently low energy prices, which, according to at least ECB president Mario Draghi, is also good for the economy as it lowers costs, the low core inflation is all the evidence we need to say the ECB is way below its target.

The ECB’s main tools in its fight against the low inflation are the Targeted Long Term Refinancing Operation, or cheap loans to banks, which will be available to the markets from September 18, and the Asset-Backed Securities program, which is in the works and will take a considerable amount of time before it is available. It has been speculated, and Draghi has hinted, that there are additional measures that could be used if the inflation outlook does not improve – but the effectiveness of a US-style quantitative easing program in Europe would be difficult to implement for political and practical reasons.

Still, investors do not expect next week’s policy-setting meeting to come up with anything but further promises to act if the TLTRO fails to have the desired effect. With the Ukrainian crisis remaining a big threat to the outlook and break-even inflation rates suggesting markets do not see inflation picking up in the short-to-medium term, perhaps the best one could hope for is a stabilisation of the inflation rate to current levels.

One thing to watch are comments over the recent fall of the euro – EURUSD is now at 1.32, while it visited 1.40 in the beginning of May. Lower values of the euro should help lift the inflation rate, but some estimates that have been thrown around suggest that the recent fall would only add about 0.1% to the annual inflation rate.

The July unemployment rate will be released at the same time, but as it is not a policy target of the central bank, it should get less attention. Still, it has been trending down for several months now, and it would be nice to see the gradual decline continuing.

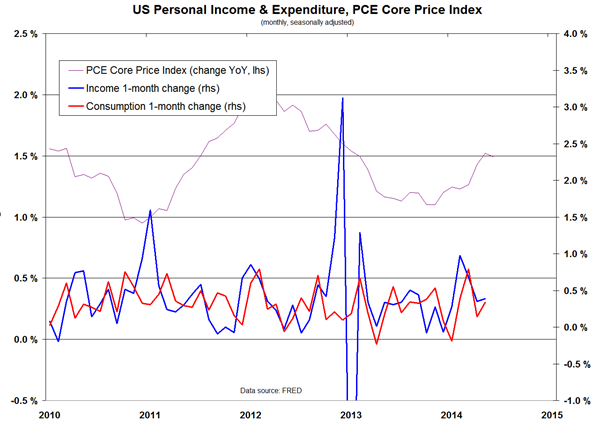

US July Personal income, spending, PCE core (12:30 GMT)

Personal income is expected to have increased by 0.3% and spending by 0.1%. All eyes will be on the Personal Consumption Expenditures price index, which is deemed by the Federal Reserve Bank to be the most reliable inflation gauge. The headline and core PCE indices are expected to both come in at around 1.5%, showing little sign of accelerating inflation.