Tuesday’s another light day for Eurozone news other than the consumer confidence update for Italy. For the US, several reports are scheduled, including new data on housing permits and the S&P/Case-Shiller Home Price Index. In addition, keep in mind that the Bank of England Governor Mark Carney will speak this morning (10:00 GMT). Later, the Conference Board releases its November report on consumer confidence (15:00 GMT).

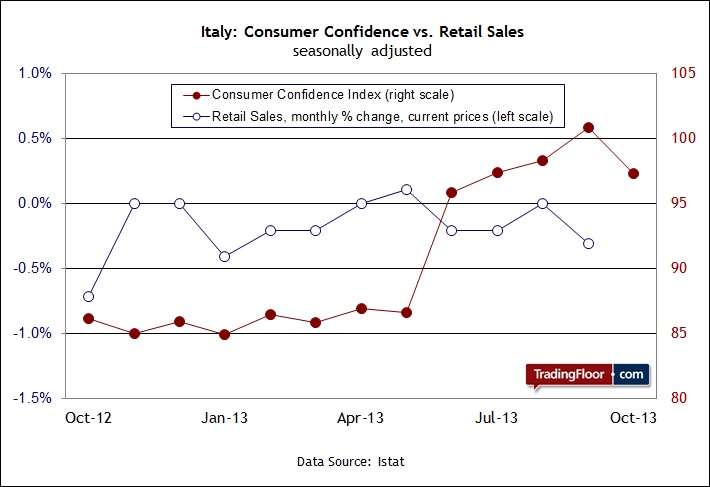

Italy Consumer Confidence (09:00 GMT) With Eurozone economic news close to non-existent today, the market will focus on consumer sentiment in Europe’s third-largest economy for updated guidance on the disinflation/deflation watch. Rationalising the European Central Bank’s surprise cut in interest rates earlier this month, ECB president Mario Draghi explained last week that “we need this buffer away from zero [rate of inflation] to provide a safety margin against deflationary risks at the euro area level. The context of this decision," he continued, "was a gradual but sustained downward drift in inflation that we had observed over several months.”

The update on consumer confidence in Italy — the only major economic number for the Eurozone published today — will surely be analysed in the context of how it influences ECB monetary policy. Meantime, history will never be far from the crowd's thinking.

The shadow of Japan’s dark legacy of letting inflation gradually fade in the 1990s is increasingly weighing on the ECB’s analysis. Draghi has been careful to say that this month's rate cut wasn't triggered by overt deflation risks, but instead as a pre-emptive act to nip the threat in the bud. But numbers speak louder than words, especially in the current climate of heightened anxiety with the outlook for Europe’s weak recovery. The OECD’s latest economic projections see the Eurozone’s recovery limping ahead, but substantial risks remain and so “the ECB should consider further policy measures if deflationary risks become more serious.”

As for Italy's economy, Rabobank advises that it sees no growth generally through the end of the year and the likelihood “the economy will only stagnate in 2014.” If the mood among consumers in Italy falls further in today’s release, the case for arguing that deflationary risks are moving in the wrong direction will strengthen, if only on the margins. Nonetheless, retail spending in Italy slumped the most in last week’s September report since January, according to Istat. A weak number in consumer confidence will only feed the growing concerns that Europe’s recovery is vulnerable.

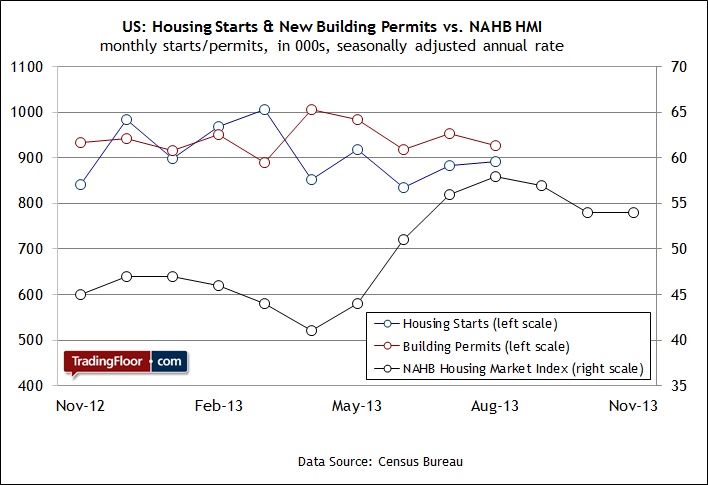

US Housing Permits (13:30 GMT) The Census Bureau today will publish newly-issued home-building permits for September and October, but the update on housing starts data has been rescheduled for December 18, thanks to lingering complications from last month’s government shutdown. The delay of the starts report will be a minor nuisance since permits will tell us quite a lot about the state of housing. Starts and permits generally track each other fairly closely through time, although the numbers have been known to exhibit more divergence in the short run.

The divergence, in fact, has been conspicuous recently, with the annualised number of permits running modestly above the level of starts in each of the five months through August. Some economists think of permits as a rough measure of demand for new housing and so the fact that the consensus forecast anticipates a slight rise in today’s September number for permits implies a marginally favourable tailwind. In any case, we’ll have quite a bit more context for evaluating the housing market with today’s permits data for the past two months. If the crowd is right and permits inch higher, we’ll have reason to think that the housing market overall will hold its ground. True, the mood among home builders has softened a bit in the last several months. But if the permits data at least hold steady, the market will find it easier to assume that the housing recovery, though slightly bruised, is still rolling forward.

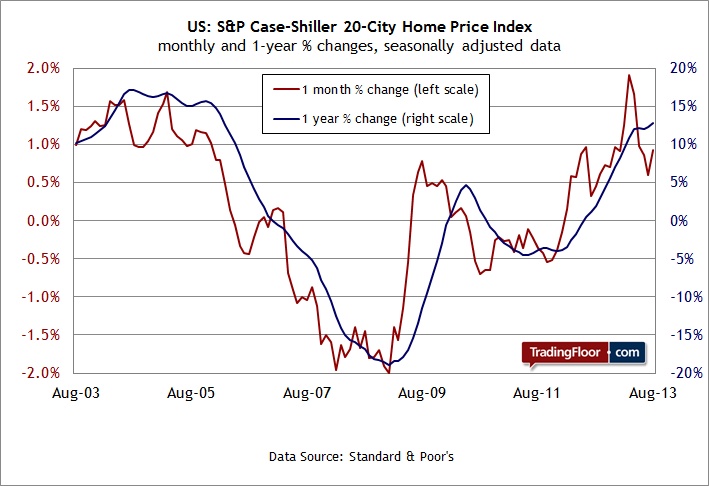

US S&P/CS Home Price Index (14:00 GMT) The Economist warns that “the recovery in housing is looking surprisingly shaky.” The offending signals: the sight of house prices rising with a reversal of fortune for sales. The combination implies trouble ahead, according to some analysts. The optimists say that the numbers only point to a “stalling, rather than a reversal”, according to one expert quoted by The Economist.

The year-over-year change in home prices certainly shows no sign of slowing. In the previous update, prices rose 12.8 percent through August vs. year-earlier levels, based on seasonally-adjusted data. That’s a bit faster than July’s pace and the highest since early 2006, when the last real estate boom was just beginning to falter. But don’t pay too much attention to forecasts. Instead, read today’s September report on the S&P/Case-Shiller Home Price Index (HPI) in context with the housing permits report that arrives 30 minutes earlier. If permits inch up or hold steady, the sight of house prices climbing will look less threatening.

Analysts think that we will, in fact, see another strong report in today’s HPI news. The consensus forecast sees the year-over-year rate running a bit higher, reaching the 13 percent mark. Another round of firm pricing data isn’t a problem if it’s accompanied by an increase in construction and sales. But as yesterday’s October update of the Pending Home Sales Index reminds, demand continues to weaken. Then again, perhaps last month’s retreat was temporarily depressed due to the government shutdown. In any case, the report on housing permits that precedes the HPI data will provide valuable guidance for deciding how to assess the news on prices.

Italy Consumer Confidence (09:00 GMT) With Eurozone economic news close to non-existent today, the market will focus on consumer sentiment in Europe’s third-largest economy for updated guidance on the disinflation/deflation watch. Rationalising the European Central Bank’s surprise cut in interest rates earlier this month, ECB president Mario Draghi explained last week that “we need this buffer away from zero [rate of inflation] to provide a safety margin against deflationary risks at the euro area level. The context of this decision," he continued, "was a gradual but sustained downward drift in inflation that we had observed over several months.”

The update on consumer confidence in Italy — the only major economic number for the Eurozone published today — will surely be analysed in the context of how it influences ECB monetary policy. Meantime, history will never be far from the crowd's thinking.

The shadow of Japan’s dark legacy of letting inflation gradually fade in the 1990s is increasingly weighing on the ECB’s analysis. Draghi has been careful to say that this month's rate cut wasn't triggered by overt deflation risks, but instead as a pre-emptive act to nip the threat in the bud. But numbers speak louder than words, especially in the current climate of heightened anxiety with the outlook for Europe’s weak recovery. The OECD’s latest economic projections see the Eurozone’s recovery limping ahead, but substantial risks remain and so “the ECB should consider further policy measures if deflationary risks become more serious.”

As for Italy's economy, Rabobank advises that it sees no growth generally through the end of the year and the likelihood “the economy will only stagnate in 2014.” If the mood among consumers in Italy falls further in today’s release, the case for arguing that deflationary risks are moving in the wrong direction will strengthen, if only on the margins. Nonetheless, retail spending in Italy slumped the most in last week’s September report since January, according to Istat. A weak number in consumer confidence will only feed the growing concerns that Europe’s recovery is vulnerable.

US Housing Permits (13:30 GMT) The Census Bureau today will publish newly-issued home-building permits for September and October, but the update on housing starts data has been rescheduled for December 18, thanks to lingering complications from last month’s government shutdown. The delay of the starts report will be a minor nuisance since permits will tell us quite a lot about the state of housing. Starts and permits generally track each other fairly closely through time, although the numbers have been known to exhibit more divergence in the short run.

The divergence, in fact, has been conspicuous recently, with the annualised number of permits running modestly above the level of starts in each of the five months through August. Some economists think of permits as a rough measure of demand for new housing and so the fact that the consensus forecast anticipates a slight rise in today’s September number for permits implies a marginally favourable tailwind. In any case, we’ll have quite a bit more context for evaluating the housing market with today’s permits data for the past two months. If the crowd is right and permits inch higher, we’ll have reason to think that the housing market overall will hold its ground. True, the mood among home builders has softened a bit in the last several months. But if the permits data at least hold steady, the market will find it easier to assume that the housing recovery, though slightly bruised, is still rolling forward.

US S&P/CS Home Price Index (14:00 GMT) The Economist warns that “the recovery in housing is looking surprisingly shaky.” The offending signals: the sight of house prices rising with a reversal of fortune for sales. The combination implies trouble ahead, according to some analysts. The optimists say that the numbers only point to a “stalling, rather than a reversal”, according to one expert quoted by The Economist.

The year-over-year change in home prices certainly shows no sign of slowing. In the previous update, prices rose 12.8 percent through August vs. year-earlier levels, based on seasonally-adjusted data. That’s a bit faster than July’s pace and the highest since early 2006, when the last real estate boom was just beginning to falter. But don’t pay too much attention to forecasts. Instead, read today’s September report on the S&P/Case-Shiller Home Price Index (HPI) in context with the housing permits report that arrives 30 minutes earlier. If permits inch up or hold steady, the sight of house prices climbing will look less threatening.

Analysts think that we will, in fact, see another strong report in today’s HPI news. The consensus forecast sees the year-over-year rate running a bit higher, reaching the 13 percent mark. Another round of firm pricing data isn’t a problem if it’s accompanied by an increase in construction and sales. But as yesterday’s October update of the Pending Home Sales Index reminds, demand continues to weaken. Then again, perhaps last month’s retreat was temporarily depressed due to the government shutdown. In any case, the report on housing permits that precedes the HPI data will provide valuable guidance for deciding how to assess the news on prices.